Worldwide Zeolite Adsorbents Market — Strategic Insights for 2026 Decision Makers

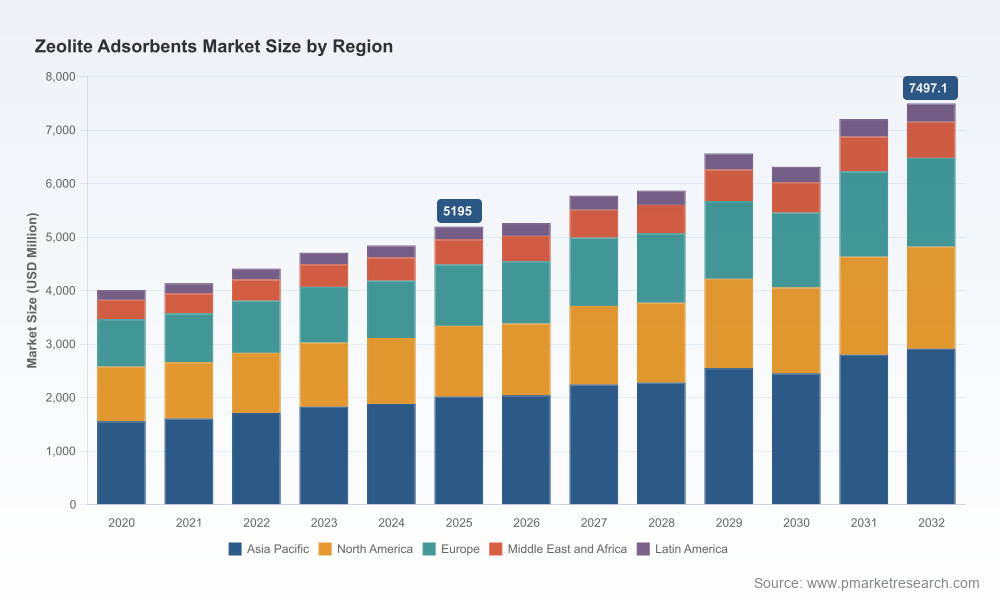

PW Consulting’s latest market study on Worldwide Zeolite Adsorbents provides a focused, decision-grade briefing for executives preparing capital, sourcing, R&D, and M&A moves in 2026. The global market for zeolite adsorbents has demonstrated steady expansion through the 2020–2025 base period and is set to continue growing over our 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 5.38%. From an estimated market size of roughly USD 4.01 billion in 2020, the industry expanded to about USD 5.20 billion in 2025 and is projected to approach USD 7.50 billion by 2032. This trajectory, combined with observable shifts in regulation, feedstock dynamics, and technology partnerships, creates a narrow window for strategic positioning — but also substantial information asymmetry that favors well-prepared players.

Worldwide Zeolite Adsorbents Market

Why this report matters for 2026 strategy

- It translates macro growth into boardroom actions: linking regulatory drivers, feedstock dynamics, and competitive moves to specific go/no‑go thresholds for capacity investments.

- It turns supply‑chain noise into procurement playbooks: quantifies exposure to aluminosilicate feedstock volatility, rare‑earth additives, and energy intensity in synthesis processes to support hedging and supplier diversification.

- It converts technology signals into commercial pathways: maps zeolite chemistries (e.g., Zeolite A, Zeolite X, Zeolite Y, ZSM‑5 and specialty formulations) to near‑term addressable industrial applications and product premiumization opportunities.

- It supports M&A and partnership diligence with a concentration lens: with top‑tier consolidation metrics indicating a moderately concentrated market structure (CR3 ≈ 34.6%; CR5 ≈ 48.2%), the report identifies pockets where scale, specialty chemistry, or regional access deliver outsized value.

Report contents — practical, usable deliverables

- Market sizing and seven‑year forecasts (2026–2032) with scenario variants tied to regulatory tightening and energy costs.

- Commercial segmentation frameworks by product type, end‑use application, and region — designed for rapid integration into internal sales and product roadmaps (note: this release intentionally omits the deep segmented tables; access the full dossier for granular splits and unit economics).

- Raw‑material and energy cost models with stress testing for aluminosilicate feedstock and selected rare‑earth additives, including sensitivity analyses and supplier concentration heatmaps.

- Regulatory impact playbook: quantified implications of emission standards, VOC capture mandates, CO2 separation targets, and detergent phosphate bans on near‑term demand patterns.

- Competitive due diligence packages for leading suppliers, including capability matrices, technology maturity assessments, and commercial threat/opportunity scoring.

- 50+ primary interviews and plant‑level capacity checks, feeding an executable set of procurement and capacity‑siting recommendations.

- M&A and partnership scouting list with valuation multipliers and integration risk checklists for bolt‑on vs. transformational deals.

Competitive landscape — what to watch in 2026

The market remains characterized by a mix of global integrated players and large regional producers. Leading firms include Honeywell UOP, BASF SE, Tosoh Corporation, Arkema (CECA), Clariant, W. R. Grace, Zeochem, Zeolyst, and sizeable Chinese and Russian producers. Our analysis of recent corporate moves and capability builds surfaces three strategic patterns:

Worldwide Zeolite Adsorbents Market

- Consolidation and capability acquisition: Strategic deals are strengthening end‑to‑end catalyst and adsorbent portfolios. Notably, Honeywell’s acquisition activity in 2025 expanded its catalyst and zeolite technologies, signaling intensified competition at the technology‑scale interface.

- Scale + specialty duality: Large incumbents continue to invest in pilot and solids processing capabilities (e.g., recent facility openings and pilot centers), while mid‑tier and regional players focus on cost optimization and tailored formulations for local markets.

- Sustainability as a differentiation axis: Partnerships that pair zeolite expertise with renewable fuels and bio‑refining routes (e.g., scale‑up collaborations for bio‑fuels conversion) are rapidly shifting the premium landscape for advanced zeolite chemistries.

For deal teams, the market concentration metrics point to a balance: top players control meaningful shares but there is room for value creation through targeted specialty offerings, regional capacity, and technology‑led differentiation. The full report includes benchmarking dossiers for each key supplier and an acquisition candidate shortlist with indicative valuation bands and synergies.

Worldwide Zeolite Adsorbents Market

Industry dynamics shaping near‑term demand

- Regulatory tightening: Stricter industrial emissions directives and air quality standards in major jurisdictions are materially increasing demand for adsorbents used in VOC capture, emission control, and CO2 separation. These regulations create predictable demand corridors for certain high‑performance products.

- Shift in consumer product chemistry: Detergent phosphate bans in multiple markets are accelerating adoption of synthetic zeolite A as a builder substitute — creating a stable, if geographically uneven, base demand.

- Raw‑material and input volatility: Synthetic zeolite manufacture depends on high‑purity aluminosilicate feedstocks and energy‑intensive synthesis routes. In addition, supply‑chain pressures on rare‑earth additives used in specific catalysts have introduced cost and availability risk that can change product economics rapidly.

- Price signals and regional dynamics: Toward late 2025, regional pricing showed divergence — with softness in certain Asian feed markets as detergent and construction demand moderated, and relative price stability in North America. These signals are early indicators of where excess capacity or underinvestment risks may emerge.

Implications for corporate strategy in 2026

Executives should translate these macro and competitive signals into three prioritized programs this year:

- Supply‑chain resilience program (Immediate — 3 months): Map exposure to critical feedstocks and rare‑earth additives, implement multi‑sourcing or toll synthesis options, and lock short‑term contracts where economically justified. The report supplies a supplier‑risk scoring template and a procurement hedging model calibrated to market volatility scenarios.

- Portfolio and pricing optimization (Near term — 3–12 months): Rebalance product portfolios toward higher‑margin, regulation‑driven solutions (e.g., emission control adsorbents, CO2 capture applications) while maintaining base volumes tied to detergents and industrial drying. The full dossier includes a margin ladder and product cannibalization matrices essential for commercial planning.

- Capex, M&A, and partnership roadmap (Medium term — 6–18 months): Use targeted investments to secure regional capacity or specialty formulations. Consider bolt‑on acquisitions to close capability gaps (e.g., pilot‑scale synthesis, solids processing expertise) and partnerships to access adjacent end markets such as sustainable fuels conversion. Our transaction playbook ranks opportunity archetypes by IRR uplift and integration complexity.

Risk factors and monitoring framework

Key upside and downside scenarios for 2026–2032 center on regulation, feedstock/energy costs, and technology substitution. The most material risks to monitor are:

- Rapid regulatory shifts that either accelerate uptake (e.g., stricter VOC/CO2 mandates) or change market access rules for certain adsorbents.

- Feedstock supply shocks—especially if aluminosilicate inputs or rare‑earth additives face export controls or mine‑level disruptions.

- Emerging competing materials or separation technologies that could displace incumbent zeolite use in specific applications.

To manage these risks, the report provides a dynamic monitoring dashboard and a set of early‑warning indicators linked to price, capacity utilization, regulatory announcements, and patent filings.

How to use this intelligence — next steps for executives

- For strategy teams: integrate the report’s forecasting scenarios into capital allocation and product roadmap reviews scheduled for 2H 2026.

- For procurement: adopt the procurement playbook and implement the supplier‑risk scoring template during Q1 supplier negotiations.

- For corporate development: use the M&A shortlist and valuation multipliers to screen targets and begin confidential outreach where appropriate.

- For R&D and product management: prioritize formulations and pilot projects that align with regulatory‑driven demand pockets and premium segments highlighted in our technology‑market fit matrices.

PW Consulting’s Worldwide Zeolite Adsorbents Market report is deliberately structured as an operational toolkit for 2026 — offering boardroom‑ready scenarios, transaction playbooks, and procurement models while reserving the granular regional and application splits for report subscribers. If your team is preparing to commit capital, restructure supply chains, or pursue strategic partnerships this year, the full report contains the segmented demand curves, plant‑level capacity checks, supplier scorecards, and unit‑cost models required to execute with confidence.

To request the full report or to arrange a briefing with our lead analysts and industry practice leaders, please visit the PW Consulting publications page or contact our market strategy practice. PW Consulting will host a members‑only webinar reviewing the detailed segmentation and the three risk‑adjusted scenarios in Q1 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Zeolite Adsorbents Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com