Next-Generation Single-Site Metallocene Catalysts vs. Traditional Multi-Site Commodity Chemical Accelerators

Other |

2026-06-18 10:56:48

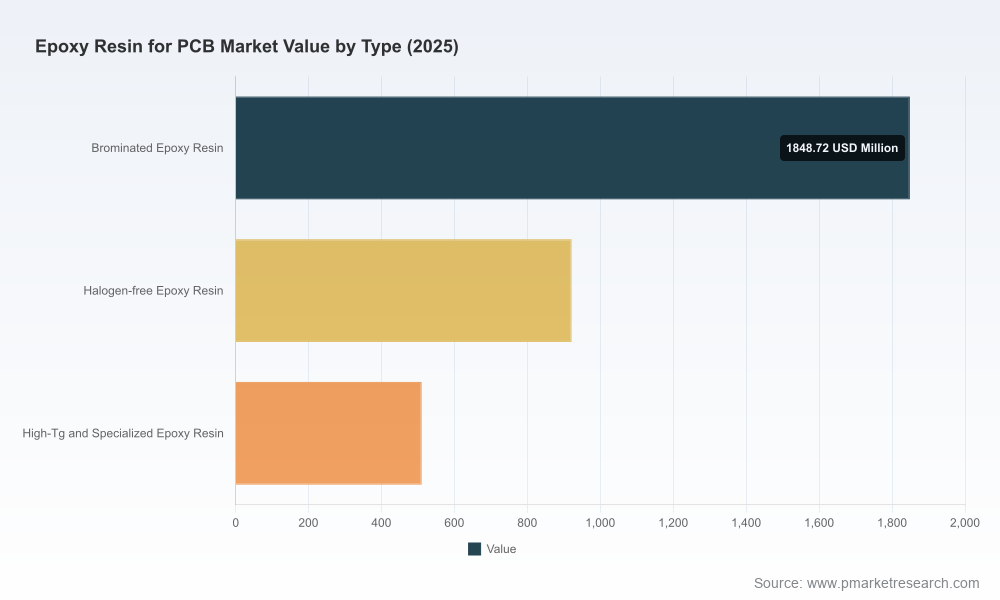

PW Consulting's new market study on Worldwide Epoxy Resin for PCB (base year 2025) frames a near‑term and medium‑term roadmap for suppliers, PCB fabricators, OEMs and investors preparing for the 2026 decision cycle. The global market demonstrated steady expansion over the historical period (2020–2025), rising from approximately USD 2,450.5 Million in 2020 to USD 3,280.5 Million in 2025. Our forward model projects continued growth across 2026–2032, with overall revenues reaching an estimated USD 4,896.83 Million by 2032 under a central forecast that implies a 5.88% CAGR for the forecast window (2026–2032).

Worldwide Epoxy Resin for PCB Market

The epoxy resin segment that supports printed circuit board (PCB) substrates sits at the intersection of several high‑velocity trends: continued miniaturization and high‑frequency performance requirements in communications and computing, electrification and advanced driver assistance systems (ADAS) in automotive, and ongoing geopolitically driven changes to trade flows and localized supply. Those forces are layered on top of a market that is moderately concentrated (CR3 ~42.5%; CR5 ~61.8%), meaning strategic moves by a handful of incumbents can shift pricing, availability and technology adoption curves quickly.

Worldwide Epoxy Resin for PCB Market

For 2026 decisions, these dynamics translate into three imperatives: (1) understand how cost and capacity shocks propagate through the PCB value chain; (2) adapt product portfolios to rising performance thresholds (thermal, Tg, low dielectric loss and halogen‑free mandates); and (3) build commercial and operational resilience to trade policy interventions and raw material cyclicality.

Worldwide Epoxy Resin for PCB Market

Policy and trade: 2025–2026 witnessed multiple trade remedies on epoxy imports across major markets; these developments materially affect sourcing economics and regional supply allocation for 2026 procurement cycles and beyond.

Capacity and competition: Large‑scale capacity projects announced and commissioned in 2024–2025 are reshaping unit cost curves in certain production hubs; some players have announced further expansions into electronic‑grade streams, increasing competitive pressure on margins for commodity grades while accelerating specialization at the high end.

Pricing signals: Feedstock and resin price movements have been uneven—in late 2025 certain key feedstocks softened, while select electronic‑materials suppliers implemented material price increases in early 2026 citing upstream cost pressures—creating transient arbitrage opportunities but also cost passthrough risks.

The market comprises vertically integrated chemical producers, specialized electronic‑grade resin manufacturers and regional players scaling capacity. Leading incumbents distinguish themselves along three axes: technical breadth (high‑Tg, low‑Dk/Df, halogen‑free systems), upstream integration (resin monomer and feedstock control), and route‑to‑market with key laminate/CCL and PCB fabricator customers.

Vertically integrated leaders leverage feedstock integration to offer stable, electronic‑grade formulations and FR‑4 platforms designed for multilayer PCBs.

Specialists emphasize differentiated chemistries for high‑frequency and automotive radar applications, and fast‑track development of halogen‑free and low‑loss resins to meet OEM specifications.

Regional champions are expanding capacity and investing in cost‑efficient liquid resin lines aimed at high‑volume electronics segments, compressing margins on commodity grades while widening availability.

PW Consulting’s report contains focused company profiles and capability mapping for the major players, highlighting where product strengths map to end‑market needs and where scale or integration confer strategic advantage. In the preview above we deliberately summarize competitive positioning without disclosing proprietary benchmarking or segment shares reserved for the full report.

This study is structured for decision use in 2026. Highlights include:

Demand model and topline forecast (2026–2032) with scenario sensitivity to end‑market adoption rates and trade shocks.

Supply‑side maps including global capacity location, lead times, typical technology routes and unit‑cost drivers for commodity and specialty resin classes.

Raw material cost pass‑through analysis and a price‑elasticity matrix linking feedstock swings to resin unit economics and PCB laminate pricing.

Regulatory and trade impact playbook: how antidumping, countervailing duties and regional safeguards reallocate supply and affect landed cost across buyer archetypes.

Competitive benchmarking and capability heatmaps (R&D, vertical integration, specialty grades, geographic presence) to inform M&A and partnership prioritization.

Commercial playbooks for procurement (strategic sourcing levers, hedging approaches, inventory strategies) and go‑to‑market for upstream suppliers targeting PCB fabricators.

Technology and product roadmaps outlining where to deploy R&D budgets to meet high‑frequency, automotive, and server/compute substrate requirements.

Note: the full report contains granular segment tables, regional allocation and application‑level metrics necessary for transaction diligence and contract modeling. The preview intentionally withholds those tables to preserve the proprietary value of the dataset.

For executive teams preparing budgets, sourcing strategies and R&D allocations in 2026, we recommend a set of prioritized actions grounded in our market model and risk analysis:

Rebalance portfolios toward higher‑value specialty grades (high‑Tg, halogen‑free, low‑loss) where technical entry barriers and certification cycles create defensible margins.

De‑risk raw material exposure through selective hedging, dual‑sourcing and conditional long‑term supply agreements that embed indexation and volume flexes.

Accelerate qualification programs with tier‑1 PCB fabricators in regions where trade remedies are increasing localization; early qualification reduces time‑to‑revenue when procurement sourcing shifts locally.

Evaluate opportunistic M&A in mid‑2026 to acquire capacity or technology that accelerates entry into automotive and high‑frequency applications—use diligence checklists that stress customer qualification pipelines and backlog convertibility.

Design flexible capex plans: prioritize brownfield expansions and modular capacity over large greenfield investments to mitigate demand volatility and trade policy risk.

Implement a price‑architecture review tying product pricing to verified performance attributes (Tg, Dk/Df, flame retardancy), reducing the likelihood of commoditization by competing on technical value rather than purely on price.

Systematize regulatory monitoring and scenario playbooks that include duty pass‑through clauses and routing alternatives to preserve margin when antidumping measures are applied.

We present three correlated scenarios to guide capital allocation and commercial timing in 2026:

Base Case (central): Demand growth aligns with our forecast (5.88% CAGR for 2026–2032), with periodic capacity additions smoothing price cycles and allowing for predictable margin management.

Upside Case: Faster adoption in high‑frequency communications and EV/ADAS spurs accelerated specialty resin uptake. Triggers: accelerated OEM design wins, sustained downstream inventory rebuilds and limited new commodity resin commissioning.

Downside Case: Trade interventions and near‑term demand slowdown combine to depress volumes and compress prices. Triggers: broader antidumping measures, abrupt downstream destocking or sustained feedstock price weakness that undercuts producer economics.

Each scenario includes a set of tactical playbooks in the full report (timing to contract renegotiation, capex staging, inventory thresholds, and M&A activation signals) so leaders can convert strategic intent into operational plans within the 2026 planning window.

PW Consulting offers a modular support suite for companies acting on the report’s insights: tailored demand and pricing models, supplier due diligence, M&A target screening calibrated to PCB qualifications, sourcing negotiation playbooks, and joint R&D partnership roadmaps. Clients also receive an interactive data package and scenario simulator so finance and commercial teams can stress test P&L and balance sheet outcomes under different market paths.

This preview is designed to surface the strategic choices and operational priorities executives must address in 2026. For procurement directors, product leaders and corporate development teams that require transaction‑grade data, the full report contains the complete dataset, detailed segmentation, regional flows, and downloadable modeling workbooks.

To explore licensing options for the dataset, request briefings on competitor profiles, or commission a custom scenario run for your business case, please visit the PW Consulting report page and download the executive datasheet. The full report and supporting models provide the granular inputs necessary to convert the strategic plays outlined here into defensible, actionable decisions.

For detailed analysis of this topic, please visit the official page:Worldwide Epoxy Resin for PCB Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com