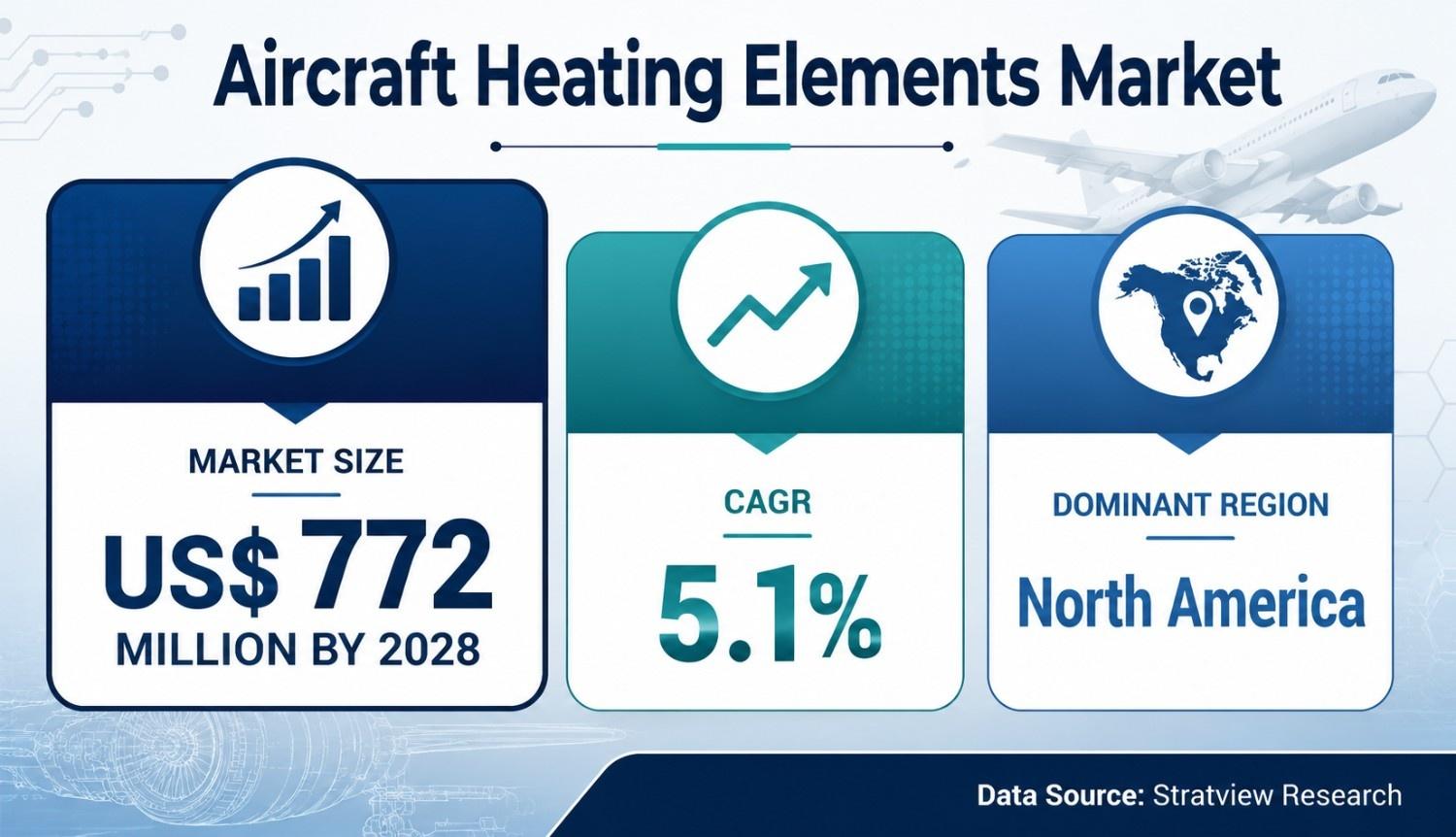

Aircraft Heating Elements Market Growth to Reach US$ 772 Million by 2028 as Applications Expand

Other |

2026-06-14 10:07:46

PW Consulting today releases an executive preview from its forthcoming Worldwide Monochlorobenzene (MCB) Market report, timed to support strategic planning for 2026. As an essential chlorinated intermediate across pesticides, dyes, pharmaceuticals and specialty chemistries, monochlorobenzene occupies a small but strategically significant corner of the chemical landscape. Our analysis synthesizes historic behavior (2020–2025), a market baseline for 2025, and a forward-looking forecast through 2032 to equip corporate leadership with the high-level insights required to shape resilient growth strategies.

Worldwide Monochlorobenzene Market

A steady growth trajectory: The Worldwide MCB market is modeled with a compound annual growth rate (CAGR) of 3.8% across PW Consulting’s forecast horizon. That steady expansion underpins many downstream value chains and informs medium-term capacity planning, pricing strategies and feedstock contracts.

Worldwide Monochlorobenzene Market

Manageable scale, outsized strategic impact: While MCB’s overall market size is modest compared with base petrochemicals, its role as an intermediate for higher-value specialty products amplifies its relevance for margins, product positioning and regulatory exposure.

Worldwide Monochlorobenzene Market

Concentration dynamics that matter: Market concentration at the top tier is material enough to shape global pricing and supply continuity. PW Consulting’s concentration metrics point to a market where the leading three and five producers exert meaningful influence — a structural feature that should inform procurement and partnership decisions.

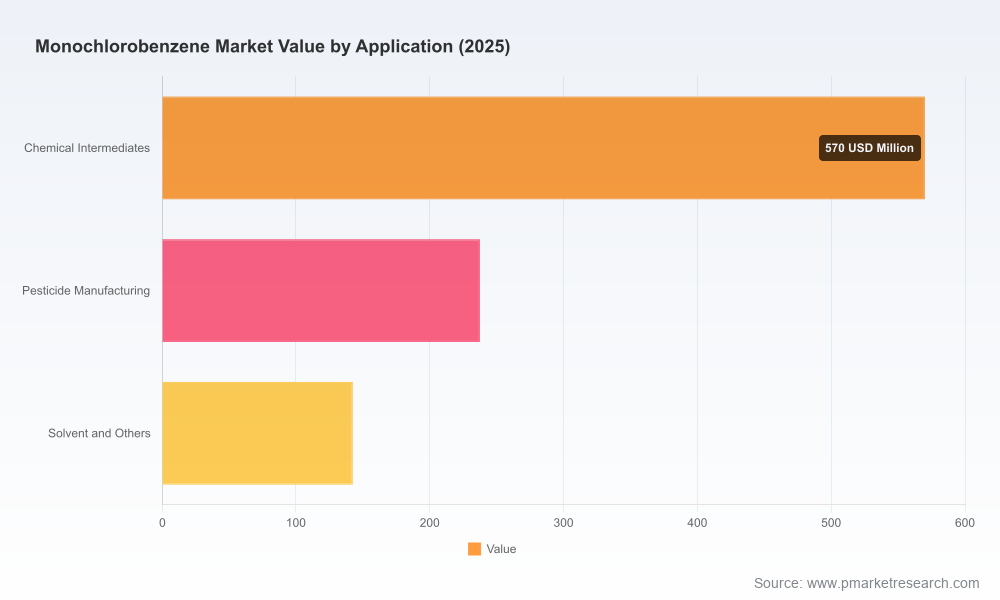

PW Consulting establishes 2025 as the base year in our analysis and models the market through 2032. The baseline market size for 2025 provides a practical starting point for budgeting, scenario analysis and capacity debates inside chemical companies. Against that baseline, the market grows at a mid-single-digit CAGR to 2032 under PW Consulting’s central scenario, reflecting a combination of steady demand from chemical intermediates and the gradual reshaping of industrial solvent use driven by regulatory change and end-market dynamics.

Key takeaways for 2026 planning: investments or contract renewals should be evaluated against a market that is growing but sensitive to feedstock swings and regulatory calibrations. Capex timing, grade mix optimization and margin protection strategies (pricing pass-through and hedging mechanisms) are central levers.

Market sizing and forecast (2020–2032): An audited baseline and probabilistic projections that support portfolio stress-testing and investment case sensitivity.

Supply-side intelligence: Capacity maps, technology routes, and a production-cost benchmarking toolkit that allow procurement and operations leaders to assess competitor cost positions and identify arbitrage opportunities.

Demand-side segmentation and use-case judgment: Graded demand analysis (industrial, pharmaceutical and reagent grades), and demand elasticity scenarios keyed to downstream end-markets.

Price and feedstock dynamics: A structured view of benzene and chlorine feedstock exposure, price transmission mechanisms, and practical guidance for hedging and contract design.

Regulatory and compliance matrix: An assessment of key regulatory levers — including recent North American policy updates affecting solvent reactivity and industrial solvent reviews — and their implications for product certification, emissions control investments and reformulation risk.

Competitive benchmarking and strategic options: Detailed company profiles, capability maps and a playbook for market entry, JV selection, and M&A prioritization.

Risk register and mitigation playbook: Scenario-driven risk assessment covering feedstock volatility, regulatory shocks, and demand displacement from substitution or green-chemistry shifts.

The MCB ecosystem blends global specialty players with regionally focused chemical producers. PW Consulting’s competitive analysis synthesizes public filings, plant-level intelligence and primary interviews to characterize strategic positioning across the value chain.

Aarti Industries Limited (India) — A regional heavyweight with integrated downstream links into dyes, pigments and agrochemical intermediates. The company’s strategy emphasizes backward integration and domestic market leadership, while selectively pursuing export channels for higher-grade streams.

ChemieOrganic Chemicals India Pvt. Ltd. (India) — A focused chlorobenzene manufacturer that competes on cost and responsiveness to regional industrial buyers. Its position demonstrates how agile, mid-sized producers can secure niche positions by offering tailored grades and logistics advantages.

LANXESS AG (Germany) — A global specialty-chemicals player with differentiated high-purity offerings for biocides and agrochemicals. LANXESS typifies the segment of the market where product purity and regulatory compliance command premium positioning.

Key Chinese producers — Several large state-owned and private players operate significant chlorobenzene capacity and exert pronounced influence on global trade flows. Their strategies vary from cost-led export models to domestic supply prioritization tied to integrated downstream manufacturing hubs.

Japanese and North American incumbents — Specialist producers and integrated chemical companies in Japan and the United States maintain positions in high-purity grades and technical services, serving demanding pharmaceutical and specialty-chemical markets.

Smaller exporters and reagent-grade suppliers — A cohort of producers from South and Southeast Asia competes on flexible production and niche reagent-grade offerings, often serving analytical and laboratory markets.

Rather than disclosing confidential market shares, the report benchmarks cost curves, purity capabilities and logistical footprints — enabling buyers and investors to identify partners and to stress-test potential supply disruptions.

Feedstock sensitivity: Benzene remains the primary upstream feedstock for MCB manufacture. PW Consulting’s monitoring shows notable regional variation in benzene availability and cost, which materially affects regional competitiveness and trade flows. Producers and buyers should prioritize feedstock risk mapping as contracts come up for renewal.

Price momentum and volatility: Chlorobenzene pricing has trended upward in recent months, reflecting tighter upstream markets and periodic logistical constraints. Buyers should design price-mechanism clauses that allow for transparent cost pass-through while protecting margins on long-term offtake commitments.

Regulatory reshaping in North America: Recent regulatory actions have revised solvent emission standards and placed certain solvent uses under closer review. This regulatory tightening will accelerate reformulation and substitution pressures in some end markets and may require capital investment in emissions controls or product stewardship programs.

Demand composition: Demand for different product grades remains the prime determinant of margin. Pharmaceutical and specialty-grade demand underpins premium pockets, while technical grades support scale — companies should continually reassess their grade portfolios and the cost-to-serve for each grade.

Prioritize feedstock resilience: Secure diversified benzene supply via staggered contracts, and evaluate tolling or co-location options with integrated benzene producers to reduce exposure to regional price swings.

Grade portfolio optimization: Reassess grade mix annually against downstream price realizations and regulatory trajectories. Incremental investment in purification capacity can unlock access to higher-margin pharmaceutical and specialty segments.

Regulatory-forward product stewardship: Implement a regulatory monitoring dashboard that flags solvent policy developments and translates them into cost and product-impact scenarios. Early engagement with regulators and customers on reformulation timelines mitigates stranded-inventory risk.

Commercial-playbook adjustments: For buyers, short-term spot cover combined with medium-term take-or-pay commitments can balance price certainty with flexibility. For producers, a two-tiered sales strategy — core long-term contracts plus opportunistic spot sales — preserves utilization and captures upside.

M&A and partnership filters: Target opportunities that add either feedstock security, access to premium-grade capabilities, or logistics advantages. Joint ventures that secure downstream offtake are especially compelling in a market where concentration at the top shapes negotiating leverage.

Feedstock price shocks — mitigated via hedging, contractual flexibility and supplier diversification.

Regulatory surprises — mitigated via proactive compliance investments and scenario planning tied to solvent use and emissions.

Demand displacement through substitution or green-chemistry alternatives — mitigated via R&D partnerships and faster product innovation cycles.

Concentration-induced supply interruptions — mitigated via strategic buffer inventories and multi-sourcing for critical grades.

PW Consulting’s full report is structured to be directly operational for 2026 decision-making. Procurement teams will find the supplier risk matrix and contract language templates immediately actionable. Business development and corporate strategy functions will benefit from scenario-based demand forecasts and the competitive playbooks for M&A screening. Plant operations and engineering teams will gain from the cost-benchmarking and capex prioritization frameworks. Together these elements create a single integrated reference to support investment memos, board briefings and tender negotiations.

Our preview intentionally showcases the depth and practical orientation of the analysis while reserving the granular breakouts and proprietary modeling inputs for the full report. Executives seeking to convert these strategic imperatives into executable plans should consult the complete study for the detailed segment-level data, capacity maps, and supplier-specific intelligence that underpin PW Consulting’s recommendations.

For 2026 planning cycles, PW Consulting recommends three immediate actions: (1) run a rapid sensitivity analysis of your MCB exposure using the report’s benchmark scenarios; (2) convene a cross-functional working group to align procurement, regulatory affairs and commercial teams on feedstock and compliance strategies; and (3) schedule a briefing with PW Consulting to review the granular data and bespoke scenario modeling that underpin our projections.

Contact PW Consulting to access the full Worldwide Monochlorobenzene Market report and the supporting models, or to arrange a tailored briefing for executive teams and board-level stakeholders. The full dataset, company-level assessments and playbooks are available through our official distribution channels.

For detailed analysis of this topic, please visit the official page:Worldwide Monochlorobenzene Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com