Revealed: Acoustic Insulation Systems Transforming Industrial Noise Control

Other |

2026-05-05 09:54:36

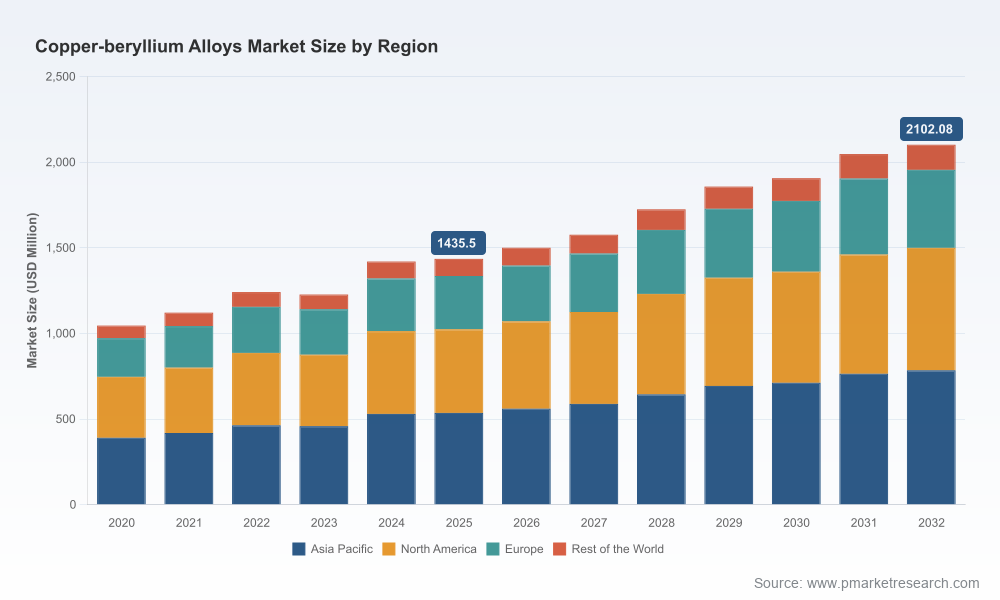

PW Consulting’s new market brief on the Worldwide Copper‑Beryllium Alloys Market provides a concise, decision‑focused preview of the intelligence senior executives and strategy teams need as they enter 2026 planning cycles. The global market reached approximately USD 1,435.5 Million in 2025 and, under our base forecast, expands to roughly USD 2,102.1 Million by 2032 — reflecting a compound annual growth rate (CAGR) of 5.6% for the 2026–2032 period. This release is intentionally framed as an executive “trailer”: it surfaces the strategic implications, risk vectors, and playbook recommendations that matter most, while directing readers to the full report for granular segment and regional tables, unit‑level modeling, and downloadable data feeds.

Worldwide Copper-beryllium Alloys Market

Immediate relevance to procurement and sourcing strategies: With demand growth outpacing mature base‑metal segments, procurement teams must rethink supplier footprints before contract renewals in 2026.

Worldwide Copper-beryllium Alloys Market

Capex and capacity planning for manufacturers: Producers and component integrators require short‑term visibility into material availability and regulatory headwinds to schedule capital projects and maintenance outages.

Worldwide Copper-beryllium Alloys Market

Mergers, partnerships and corporate development: The market’s concentration and specialized upstream supply position make M&A and JV activity a top lever for securing feedstock and technology access.

Regulatory compliance and workforce safety: Tightening exposure limits and hazardous substance listings mean compliance programs must be operationalized alongside commercial initiatives — not after the fact.

After a period of uneven growth during 2020–2025, the copper‑beryllium alloys market enters a structurally favorable phase driven by continued strengthening demand across high‑value applications and constrained upstream beryllium supply. Our modeling shows the market rising from USD 1,435.5 Million in 2025 to approximately USD 2,102.1 Million in 2032, a 5.6% CAGR for 2026–2032. The forecast incorporates scenario stress tests covering supply shocks, regulatory tightening, and substitution adoption curves. The market remains concentrated: the three largest producers account for a dominant share of global capacity, with the top five firms encompassing a substantial majority—an important factor for buyers and investors assessing bargaining power, pricing dynamics, and the feasibility of supplier diversification strategies.

Upstream supply constraints: Beryllium mine production is limited in scale, with only a handful of primary producers globally. The scarcity profile of raw beryllium and the geography of production create tangible supply‑chain risk that ripples through alloy availability and lead times.

Export controls and trade policy: Recent policy moves — including the addition of beryllium metal to certain export control lists — have already introduced friction into global flows and require early engagement by procurement and trade compliance teams.

Occupational and chemical regulation: Longstanding occupational exposure limits and classification of beryllium compounds as high‑concern substances under modern chemical regimes impose compliance costs and can restrict use in certain jurisdictions without authorization pathways.

The market is dominated by a small number of specialized, vertically integrated players that combine metallurgy expertise with application‑specific alloy portfolios. Three names that consistently anchor supplier shortlists for global OEMs and integrators are:

Materion Corporation — Mayfield Heights, Ohio, USA (https://www.materion.com). A global leader in copper‑beryllium alloys and engineered ToughMet products, Materion supplies aerospace, electronics and oil & gas customers with high‑performance grades and extensive metallurgical support capabilities.

NGK Metals Corporation — Reading, Pennsylvania, USA (https://www.ngkmetals.com). Specialist producer of precision strip, wire and rod forms for connectors, springs and precision components; recognized for process control and component‑level engineering partnerships.

Ulba Metallurgical Plant JSC — Ust‑Kamenogorsk, Kazakhstan (https://ulba.kz). Significant producer of beryllium‑bearing alloys and semi‑finished products, with export flows into electronics and defense supply chains globally.

These incumbents benefit from technical know‑how and regulatory experience that create high barriers for new entrants. For buyers, this translates into limited near‑term options to pursue pure spot‑market savings without accepting elevated execution risk. For investors and consolidators, the oligopolistic structure amplifies the strategic value of acquiring capability rather than capacity alone.

The full PW Consulting report is structured to translate market intelligence into executable programs. Key deliverables include:

Macro and micro forecasts with downloadable scenario files (three base scenarios + stress cases).

Supplier mapping and supplier‑risk scoring covering technology capability, capacity, regulatory posture and geopolitical exposure.

Application‑level demand archetypes and adoption curves for high‑value end markets (telecom and electronics, automotive electrification, aerospace/defense, and energy).

Practical compliance checklists and a gap‑closure playbook for OSHA/EU/China export control implications.

Unit economics and price‑build models for major product forms (strip/foil, rod/bar, wire, tube/others) to support margin recovery initiatives and contract negotiations.

M&A target shortlists and integration playbooks focused on technology accretive targets, recycling and circularity assets, and non‑beryllium substitute technology providers.

Operational decarbonization pathways where alloy producers can reduce Scope 1/2 exposure and align with customer sustainability requirements.

Prioritize supply diversification now: Build a tiered sourcing strategy that blends primary producers, qualified secondary processors, and certified recyclers. Begin qualifying second‑source suppliers under parallel development tracks to shorten switch timelines.

Operationalize regulatory resilience: Invest in audit‑grade exposure monitoring and vendor compliance documentation. Where authorization regimes exist, engage early with regulators and counsel to de‑risk project timelines.

Shortlist alloy alternatives and substitution strategies: For non‑mission‑critical uses, accelerate validation of low‑beryllium or beryllium‑free alloys to create optionality and reduce long‑term dependence.

Embed cost‑to‑serve and price‑build models into commercial negotiations: Use supplier cost transparency tools and joint cost‑reduction programs to contain input price volatility without eroding supply resilience.

Consider targeted M&A or partnerships: Acquiring specialty processors, recycling capabilities or minority stakes in raw‑material sources can be more value‑accretive than greenfield capacity investments.

Elevate workforce safety and community engagement: Strong occupational‑health programs are not just compliance items — they are commercial differentiators when bidding for aerospace and defense contracts.

To assist corporate planners, our model includes at least three central scenarios: a baseline that assumes steady regulatory enforcement and moderate trade disruptions; a constrained‑supply scenario driven by export controls and a production shortfall; and a substitution/technology shift scenario that accelerates uptake of beryllium‑free alternatives in targeted applications. Each scenario provides decision triggers and tactical checklists to inform procurement cadence, inventory strategy, and capital planning.

Supplement annual budgeting with rolling 12‑ to 24‑month supplier risk reviews that use the report’s supplier‑risk scoring outputs.

Convert forecast variances into procurement clauses: force majeure language, price‑adjustment mechanisms linked to raw‑material indices, and explicit compliance warranties.

Benchmark strategic initiatives: use our concentration and scenario outputs to prioritize whether to allocate scarce R&D and M&A capital to securing feedstock, expanding downstream capabilities, or pursuing substitution technologies.

PW Consulting’s preview is designed to equip executive teams with the judgmental framing and playbooks required for robust 2026 planning. It deliberately omits granular region‑by‑region and application‑level tables in this summary so that technical and commercial teams download the underlying datasets and models where they can be integrated directly into ERP, S&OP, and M&A diligence processes.

For access to the full report — including downloadable scenario spreadsheets, supplier lists, regional demand matrices, and product‑form unit economics — please visit PW Consulting’s research portal. The comprehensive dataset and configurable models are provided under license to enable direct integration into corporate planning systems and diligence workstreams.

Pw Consulting’s Worldwide Copper‑Beryllium Alloys Market report is the actionable starting point for procurement, manufacturing, strategy and investor teams preparing to make pivotal choices in 2026. Contact our industry team to schedule a data walkthrough and workshop tailored to your company’s role in the value chain.

For detailed analysis of this topic, please visit the official page:Worldwide Copper-beryllium Alloys Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com