Worldwide Automotive Body Comfort System Market — Strategic Insights for 2026 Decision-Makers

Executive Snapshot

PW Consulting’s latest report on the Worldwide Automotive Body Comfort System Market delivers an authoritative, actionable roadmap for executives making portfolio, sourcing, and M&A decisions in 2026. Built on a base year of 2025 and a forecast spanning 2026–2032, the study quantifies an industry that expanded from roughly USD 71,240.5 Million in 2020 to USD 100,260.0 Million in 2025 and is projected to reach approximately USD 162,190.2 Million by 2032, reflecting a compound annual growth rate (CAGR) of 7.11% across the forecast horizon. All financials are denominated in USD Million.

Worldwide Automotive Body Comfort System Market

Why this report matters for 2026 strategy

- It reframes comfort systems from component line-items to strategic experience platforms that drive vehicle differentiation, customer retention, and recurring-service opportunities.

- It bridges hardware, software, and sustainability considerations—providing a cross-functional lens that CFOs, product heads, and procurement teams can use to prioritize investments quickly.

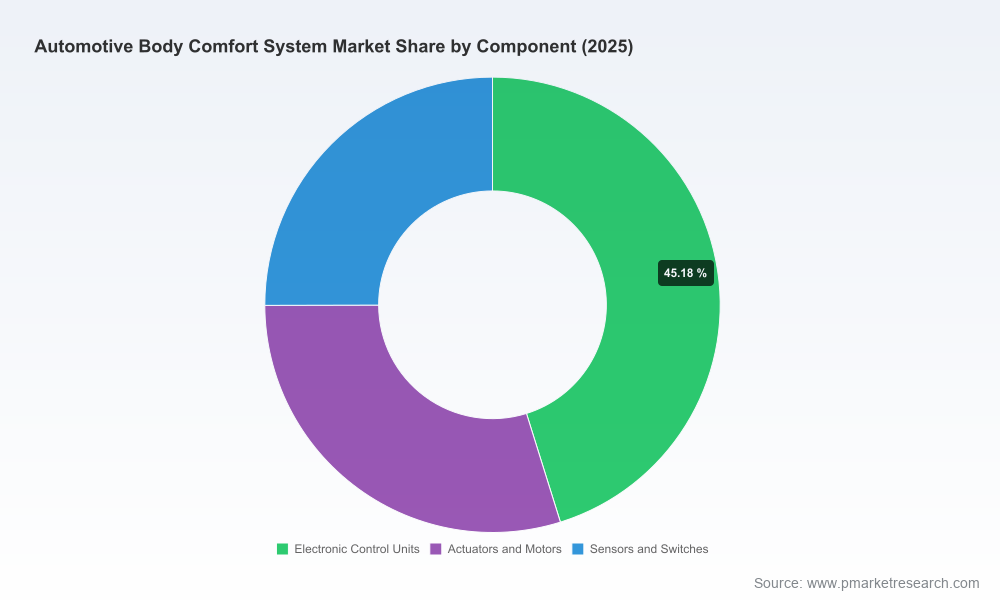

- It surfaces competitive positions measured both by market concentration (CR3 ~31.4%; CR5 ~46.8%) and by capability clusters—guiding partnership and M&A hypotheses where scale matters but nimble specialization pays.

Market dynamics and the 2026 decision context

The body comfort systems space is being reshaped by three converging forces: vehicle-level electrification and thermal management needs; software-defined personalization; and regulatory plus materials-driven sustainability targets. These dynamics mean that comfort sub-systems—traditionally engineered as electro-mechanical assemblies—are evolving into networked, software-rich modules that interoperate with HVAC, driver monitoring, and vehicle energy management systems.

Worldwide Automotive Body Comfort System Market

Key technical and regulatory inflection points that will influence 2026 priorities include:

Worldwide Automotive Body Comfort System Market

- Regulatory integration: New safety and monitoring mandates (e.g., EU driver/occupant monitoring requirements) are accelerating the need to embed occupant sensing within body and comfort electronics architectures rather than as bolt-ons.

- Communications and low-power architectures: Adoption of next-generation CAN FD SIC transceivers compliant with the latest ISO edition is enabling lower-power standby modes and new comfort functions without significant energy penalties—critical for EVs.

- Sustainability and materials: OEM targets for recycled and renewable plastics in interiors—formalized in several OEM sustainability plans from 2025 onward—require rethinking supplier selection, qualification cycles, and component-design-for-recycled-materials programs.

Core growth drivers through 2032

- EV proliferation and cabin electrification: As vehicle architectures move away from mechanical HVAC load sources and toward localized thermal management, demand for advanced seat and localized comfort systems accelerates.

- Premiumization and personalization: Consumers increasingly expect multi-zone thermal comfort, active ventilation, massage, and personalized climate zones—pushing suppliers to add sensors, actuators, and software layers.

- OEM differentiation: Interior comfort systems are fast becoming a primary tactile and emotional differentiator in the showroom and in digital marketing—driving OEMs to integrate comfort features earlier in platform design cycles.

What’s inside the PW Consulting study (practical, decision-ready content)

The report is designed for executives who must translate market signals into operational moves. Key deliverables include:

- Comprehensive market sizing and long-form forecast (2026–2032) by component, architecture, and application—presented with scenario sensitivity to energy and materials shocks.

- Go-to-market playbooks for Tier-1 suppliers, component specialists, and OEMs that prioritize modularity, software monetization, and aftersales strategies.

- Supplier strategic scorecards and capability maps covering electronics, actuators, sensors, thermal modules, and embedded software—differentiating scale-players from best-in-class specialists.

- Detailed technology roadmaps showing likely timing for mass adoption of occupant sensing arrays, ECUs with multi-domain integration, and low-power CAN FD implementations.

- Commercial diligence templates, valuation priors, and M&A screening filters for acquirers targeting inorganic growth in comfort subsystems.

- Supply-chain resilience and raw-materials analysis with mitigation options—covering polymer substitution, recycling qualification timelines, and secondary-market sourcing strategies.

- Tested scenario planning: high-adoption, baseline, and constrained-growth cases tied to macro variables (EV penetration, raw-material constraints, regulatory changes).

Competitive landscape — strategic implications for 2026

The competitive topology is a hybrid of global systems integrators and focused specialists. The market concentration metrics (CR3 ≈ 31.4%, CR5 ≈ 46.8%) indicate meaningful scale advantage for the top players but leave ample room for differentiated, regional, or technology-led challengers. Notable participant archetypes and strategic takeaways:

- Gentherm (United States): A leader in thermal-seat solutions. Strength lies in deep thermal IP and system-level integration; strategy recommendation: pursue software and sensing partnerships to turn thermal modules into customer-facing features that can be updated OTA.

- Lear Corporation (United States): Offers full seating systems with integrated comfort modules. Strength lies in system integration and OEM relationships; strategy recommendation: product modularization and a platform licensing approach for mid-volume OEMs will defend margin pressure from low-cost regional suppliers.

- Adient plc (Ireland): Emphasizes ergonomics and modular architectures. With recent product innovations focused on occupant safety and comfort, Adient is well positioned to marry safety electronics with comfort features—consider prioritizing Tier‑1 OEM collaborations that bundle safety and comfort offerings.

- FORVIA (Faurecia) and Magna International: Large interior suppliers with full-system capabilities. Their global footprint supports scale and cross-sell; recommended move: concentrate R&D on integrated cabin climate subsystems that reduce part count and optimize vehicle energy budgets.

- Continental and Robert Bosch: Strong in body and comfort electronics and sensors. They are natural owners of the control‑logics layer—opportunities exist for licensing software stacks to smaller seat manufacturers whilst protecting OEM-facing system contracts.

- Denso, Valeo, Toyota Boshoku, Kongsberg Automotive, Alfmeier Präzision: Each brings targeted competencies—from HVAC and climate control to precision actuators. For these players, the strategic imperative is to lock in materials-flows and to co-develop qualification programs for recycled materials to remain integrated into OEM supply chains.

Recent industry signals support these strategic priorities: Adient’s August 2025 product innovation emphasized ergonomics and integrated occupant safety; broader supplier studies (e.g., BCG’s March 2026 Global Automotive Supplier Study) underline the growing importance of interior and comfort systems as OEM differentiation vectors.

Risks and tailwinds

- Risks: Materials supply disruptions and recycled-material qualification timelines; semiconductor and power‑electronics sourcing constraints; and potential regulatory fragmentation across major markets that could raise compliance costs.

- Tailwinds: Strong OEM appetite for interior differentiation; energy-efficient architectures in EVs enabling new comfort features; and sustainability mandates stimulating innovation in material substitution and circular-design practices.

Actionable 2026 playbook — six moves for market leaders and challengers

- Re-prioritize R&D margins to ‘software plus sensing’ — fund embedded software, occupant models, and OTA frameworks to convert one‑time hardware sales into recurring software-enabled value.

- Adopt modular architecture standards — accelerate platformization so comfort modules can be validated once and scaled across multiple vehicle programs, reducing qualification lead time.

- Secure materials & circularity pathways — lock long-term offtakes for recycled polymers, and co-invest in accelerated qualification with tier‑down OEMs to avoid late-stage redesigns.

- Pursue bolt-on and capability-driven M&A — target unique sensor or MCU assets that close gaps in system-level offerings; use our M&A filters to prioritize targets that shorten time-to-market by 12–18 months.

- Strengthen software economics — implement feature-tiering strategies and subscription pilots where permitted, focusing on personalization and wellness services linked to seat and climate subsystems.

- Invest in joint validation with OEMs — propose shared testbeds around safety-comfort integration (driver monitoring + occupant climate) to accelerate homologation and deepen OEM lock-in.

How PW Consulting can help you act

This report is intentionally strategic and action-oriented: it provides the datasets, supplier matrices, scenario tools, and commercial playbooks that permit rapid, evidence-based decision-making in 2026. To preserve competitive value for subscribers, we have intentionally withheld the detailed regional and application-level numeric splits in this release—those granular tables and downloadable models are available on the report landing page and via our subscription service.

If your priorities for 2026 include portfolio rationalization, targeted M&A, or a rapid pivot to software-enabled comfort monetization, PW Consulting’s data, model access, and bespoke advisory services are designed to convert the opportunities described here into executable programs.

Next steps

- Download the executive package or request an in-depth briefing to review the supplier scorecards, detailed forecast workbook, and scenario models.

- Engage our advisory team for a tailored strategy session—covering target-screening for acquisitions, cost-to-serve simulations, or validation roadmap development for recycled-material integration.

PW Consulting — providing the market clarity and operational templates executives need to make confident, timely decisions in the evolving automotive body comfort systems landscape.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Body Comfort System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com