Worldwide Air Quality Sensor ICs Market — Strategic Imperatives for 2026

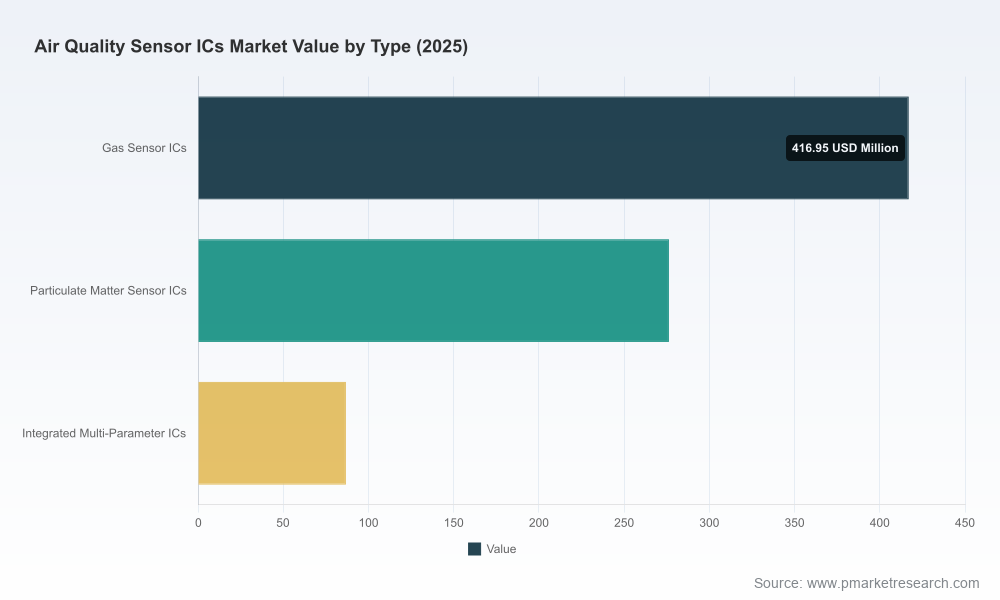

The global market for air quality sensor integrated circuits (ICs) stands at a pivotal inflection point. After expanding from a mid-single‑hundred million-dollar industry in 2020 to an estimated USD 780.0 Million in 2025, the sector is forecast to accelerate through the coming decade — reaching an expected USD 868.92 Million in 2026 and, under our base forecast, approximately USD 1,569.03 Million by 2032. That trajectory implies a compounded annual growth rate of roughly 10.51% across the 2026–2032 horizon. For executives setting product roadmaps, capital allocation, and supply‑chain strategies in 2026, these macro dynamics are not abstract trends: they are the market signals that should shape near‑term investment, partner selection, and competitive positioning.

Worldwide Air Quality Sensor ICs Market

Why this report matters for enterprise decisions in 2026

- Translate growth into profitable action: Understand where higher ASPs, volume expansion, and feature‑led differentiation will combine to produce meaningful margin expansion versus mere revenue growth.

- Prioritize investments under supply stress: The report maps material and geopolitical exposures (critical minerals, MEMS fabs, specialty gases) so procurement leaders can sequence diversification and stock strategies.

- De‑risk product plans with regulatory foresight: New tariffs, import controls, and emerging IAQ standards are modeled into realistic scenarios for 2026 program approval cycles.

- Shape M&A and partnership playbooks: Our competitiveness and concentration analysis highlights where bolt‑on acquisitions, licensing deals, or co‑development agreements deliver the fastest market access.

What the report delivers — practical, operational intelligence

- Transparent market model: A bottoms‑up revenue forecast by device class and end application with driver‑level sensitivity (unit volumes, ASP trajectories, sensor fusion share). The model is delivered in an editable workbook so you can re‑baseline to your internal assumptions.

- Technology deep dives: Comparative techno‑economic profiles for MEMS, MOX, NDIR, photoacoustic, laser‑based PM and emerging integrated multi‑parameter IC architectures — highlighting cost curves, power profiles, size tradeoffs, and algorithm requirements.

- Supply‑chain heatmaps: Tiered supplier lists, concentration risk scores, and alternative sourcing routes for wafers, packaging, and specialty substrates — with suggested lead‑time hedging tactics for 2026 procurement cycles.

- Regulatory & policy scenarios: Quantified impact matrices for tariff regimes, export controls, and environmental compliance costs under multiple geopolitical stress cases.

- Commercial playbooks: Channel and OEM engagement strategies, pricing elasticity benchmarks, product bundle constructs (hardware + firmware + cloud analytics), and go‑to‑market sequencing by customer type.

- Vendor scorecards & competitive benchmarks: Independent scoring across technology readiness, manufacturability, certification status, roadmap clarity, and partner openness to co‑development.

- Actionable M&A diagnostic: Quick‑screen acquisition targets, accretion/dilution sensitivity, and integration playbooks focused on sensor IP, calibration labs, and software stacks.

Competitive landscape — who is shaping 2026 product choices

The air quality sensor IC market exhibits measurable concentration: the top three suppliers account for a meaningful share of industry revenues, and the top five consolidate a majority position. That market structure creates both stability — through established supply agreements with large OEMs — and opportunity for challengers that can undercut on power, size, or integration. Below we synthesize competitive positioning and the near‑term moves that will influence 2026 procurement and partnership decisions.

Worldwide Air Quality Sensor ICs Market

- Sensirion AG (Stäfa, Switzerland) — Strengths: CMOSens® ecosystem, strong multi‑parameter platforms, and deep algorithm/IP assets. Recent launches (December 2025 SEN65 and SEN63C) reinforce the company’s lead in integrated indoor‑air solutions. Strategic implication: Sensirion remains the go‑to for integrators seeking off‑the‑shelf multi‑parameter accuracy, but premium positioning requires partners to accept higher ASPs or commit to co‑development.

- ScioSense B.V. (Eindhoven, Netherlands) — Strengths: MOX expertise and automotive‑grade variants enable strong traction in cabin monitoring and embedded consumer use cases. Strategic implication: Companies targeting automotive OEM programs or ruggedized consumer wearables should evaluate ScioSense for its robustness and firmware‑based compensation capabilities.

- Bosch Sensortec GmbH (Reutlingen, Germany) — Strengths: MEMS integration, AI‑assisted sensing, and rapid miniaturization. Bosch’s 2025/2026 introductions (BME690 and the fanless BMV080) signal a focused push into ultra‑compact, low‑power IoT form factors. Strategic implication: Expect Bosch to be favored where design‑in size and power are gating requirements; partnerships should prioritize joint optimization of sensor + system stacks.

- Renesas Electronics Corporation (Tokyo, Japan) — Strengths: Firmware‑configurable modules and strong systems integration pedigree. Renesas’ ZMOD family simplifies signal conditioning and accelerates time‑to‑market. Strategic implication: For OEMs with constrained firmware resources, Renesas offers an attractive turnkey option, albeit with less architectural flexibility for deep customization.

- Infineon Technologies AG (Neubiberg, Germany) — Strengths: Photoacoustic spectroscopy (XENSIV PAS) for high‑accuracy CO2 sensing in smart‑building applications. Infineon’s 2024 and continuing product cadence positions it as the accuracy leader for HVAC and compliance‑sensitive installations. Strategic implication: Where regulatory compliance or occupant health metrics are contractual obligations, Infineon’s platform is often the safer technical choice.

- Amphenol Advanced Sensors & Amphenol SGX (USA / UK) — Strengths: Broad portfolio across NDIR, MOX, and PM sensors and deep channel reach into HVAC and building automation. Strategic implication: Amphenol’s portfolio breadth and assembly capabilities favor large OEMs and integrators requiring multi‑supplier convenience and consolidated logistics.

- Cubic Sensor and Instrument Co., Ltd. (Wuhan, China) — Strengths: Integrated module manufacturing combining PM, CO2, VOC and environmental sensing with cost competitiveness. Strategic implication: Strong contender for high‑volume deployments where BOM cost is first order and regional supply continuity is critical.

Industry headwinds, regulatory shocks, and 2026 risk management

- Tariff and trade policy volatility: Recent policy actions — including new tariffs on certain advanced computing chips — can increase upstream semiconductor costs and recalibrate sourcing economics for sensor ICs. The report models realistic margin impacts and recommends procurement hedges and tariff mitigation strategies.

- Critical minerals & material restrictions: Export controls and restrictions on rare earths and other inputs have raised the risk of localized shortages and price spikes. We quantify substitute options, recycling potential, and strategic inventory thresholds to maintain production continuity in 2026.

- Environmental compliance costs: Upstream semiconductor fabs generate VOCs, NOx, SOx and particulate emissions that are increasingly regulated. Our analysis captures likely capex and opex implications for suppliers and the pass‑through to sensor IC pricing.

- Concentration & supplier lock‑in: With the market’s top suppliers holding a significant share of revenues, buyers should plan parallel qualification tracks and second‑source strategies to avoid single‑supplier exposure for critical programs.

Actionable strategic recommendations for 2026

- Implement dual‑sourcing for critical ICs and qualify a functional second supplier within the calendar year to reduce single‑point risks.

- Invest in sensor fusion and edge analytics to differentiate on value beyond raw sensor accuracy — software will increasingly command a share of product economics.

- Lock multi‑year supply contracts for specialty substrates and critical passives; use options and indexed pricing to hedge against commodity shocks driven by geopolitics.

- Pursue modular certification pathways (e.g., building codes, automotive qualification) early in the development cycle to compress time‑to‑market and reduce rework costs.

- Consider targeted M&A for calibration labs, firmware teams, or small‑scale fabs to internalize capabilities that materially shorten product lead times.

- Stress‑test pricing and demand under tariffs and export restriction scenarios using our scenario models before finalizing 2026 budgets.

How PW Consulting’s Worldwide Air Quality Sensor ICs Market report enables execution

Our report is structured to move clients from insight to action. Beyond an independent market forecast and vendor scorecards, subscribers receive the editable revenue model, a supplier risk heatmap recalibrated for their bill of materials, a scenario simulation workbook for tariff and material‑constraint contingencies, and a playbook for commercial negotiations with incumbent sensor suppliers. We also offer tailored workshops and a fast‑track consulting engagement to translate report findings into procurement contracts, product roadmaps, or M&A target screens within 60 days.

Worldwide Air Quality Sensor ICs Market

For companies making 2026 strategic bets — from launching new consumer IAQ devices to committing to automotive cabin sensing programs or scaling smart‑city deployments — this report provides the quantitative backbone and tactical playbooks necessary to convert market growth into durable competitive advantage. To review our full segment breakouts, vendor scorecards, and the complete model, visit the report page for subscriber access and validation datasets.

For detailed analysis of this topic, please visit the official page:Worldwide Air Quality Sensor ICs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com