Automotive Over-The-Air (OTA) Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-03-22 07:14:44

As organizations prepare capital plans and product roadmaps for 2026, high resolution mass spectrometry (HRMS) is no longer a niche analytical tool — it is a strategic enabler across clinical diagnostics, proteomics, environmental monitoring, and biopharma characterization. PW Consulting’s new Worldwide High Resolution Mass Spectrometry System Market report (base year 2025) synthesizes seven years of historical trends and a seven-year forecast (2026–2032) to give senior executives, procurement leads, and investors the pragmatic intelligence they need to move from reactive buying to proactive capability-building.

Worldwide High Resolution Mass Spectrometry System Market

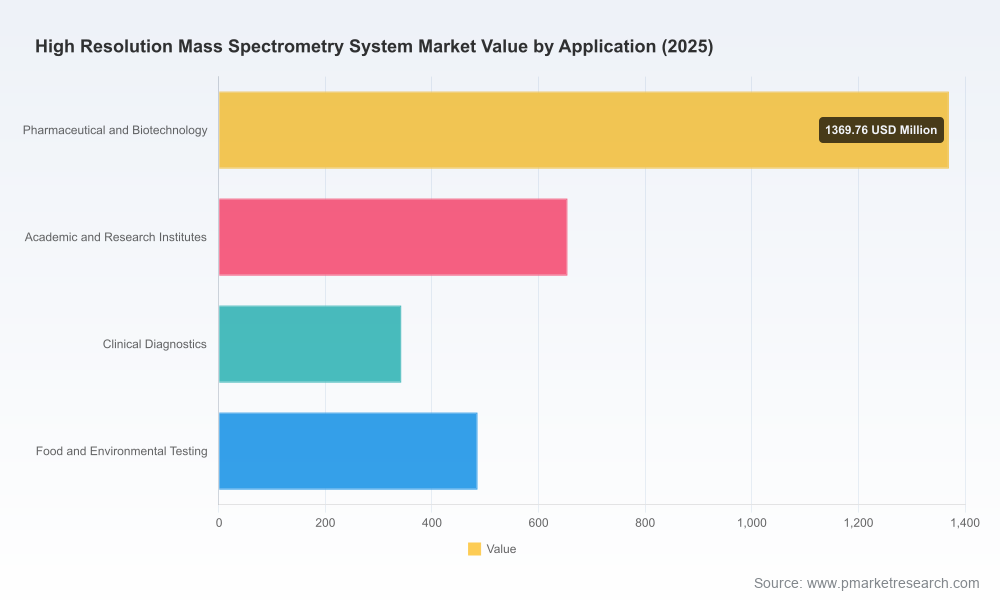

The HRMS market has demonstrated healthy expansion through the first half of the decade: total industry revenues rose from USD 1,935.2 Million in 2020 to USD 2,851.32 Million in 2025. Our modelling — grounded in equipment shipments, installed-base replacement cycles, service revenue flows, and regulatory-driven demand — projects continued growth in 2026 and beyond, with the market forecast to exceed USD 3,163.87 Million in 2026 and to approach USD 4,924.80 Million by 2032, reflecting a compound annual growth rate (CAGR) of 8.12% across the forecast period.

Worldwide High Resolution Mass Spectrometry System Market

Regulatory harmonization and reimbursement clarity are converging to accelerate clinical adoption. The FDA’s Quality Management System Regulation (QMSR) revision to 21 CFR Part 820, effective February 2, 2026, aligns device quality requirements with international standards — lowering regulatory friction for manufacturers integrating HRMS hardware into clinical workflows.

Worldwide High Resolution Mass Spectrometry System Market

Clinical platforms are maturing. Recent regulatory and product milestones (notably expanded CE-mark IVD menus and new automated mass spec platforms) are creating templates for standardized lab deployment, accelerating conversion of research-class instruments into routine clinical assets.

Environmental and public-health mandates are expanding the non-clinical addressable market. New monitoring rules requiring sub-ppq/ppb detection thresholds elevate HRMS from “nice to have” to “mission critical” for many contract and public laboratories.

Executives planning CapEx, partnerships, or M&A in 2026 should prioritize three interdependent initiatives:

Capability-first procurement: Shift evaluation criteria from headline instrument specs to operational metrics — throughput per square meter, consumables intensity, service SLAs, and laboratory workflow integration. Instruments with lower life-cycle cost and predictable service economics will outcompete higher-specification entrants when budgets tighten.

Regulatory-anchored productization: For vendors and OEM partners, embedding QMSR-aligned documentation and IVD-ready workflows into product deliveries will materially shorten sales cycles into hospital systems and clinical networks.

Platform partnerships: Biopharma and clinical labs should accelerate ecosystem plays (sample prep, LIMS, AI-assisted data interpretation). Interoperable stacks reduce time-to-result and create higher switching costs, which is a defensible commercial advantage in a market exhibiting meaningful concentration among leading vendors.

The vendor field is bifurcating around two value propositions: ultra-high-performance platforms for discovery and proteomics, and cost-optimized, automated systems for clinical and routine testing. Market concentration metrics indicate a market where a small group of global vendors captures a majority of revenues, with the top three and five players representing significant shares — a dynamic that influences pricing, service models, and channel strategies.

Thermo Fisher Scientific: Continued investment in next-generation Orbitrap platforms reinforces Thermo Fisher’s leadership in high-accuracy workflows for precision medicine and proteomics. Recent introductions emphasize speed and sensitivity improvements that matter in large-scale proteomic and multi-omics projects.

Bruker Corporation: Product advances focused on ion mobility and functional proteoform sequencing strengthen Bruker’s position in spatial biology and deep-proteome applications — segments where differentiation is driven by instrument architecture and software pipelines.

SCIEX (Danaher): New QTOF platforms and high-throughput triple quadrupole lines position SCIEX to serve large clinical labs and contract testing organizations where sample throughput and robustness trump maximum resolving power.

Waters, Agilent, Shimadzu, JEOL, PerkinElmer and others: Each incumbent is executing a hybrid strategy — balancing instruments for discovery with variants tailored for routine lab automation. Market access strategies vary by channel strength, service footprint, and vertical partnerships.

Roche: As an adjacent diagnostics OEM, Roche’s expansion of its cobas Mass Spec automated platform into a broader IVD menu demonstrates how in vitro diagnostic positioning can reframe market expectations for laboratory automation and reimbursement pathways.

Product launches at ASMS 2025 — including Thermo Fisher’s Orbitrap Astral Zoom and Excedion Pro, Bruker’s timsUltra AIP and timsOmni, Waters’ Xevo TQ Absolute XR, and SCIEX’s ZenoTOF 8600 — accelerated the technological arms race around throughput, sensitivity, and operational efficiency.

Regulatory approval events, notably Roche’s December 2025 CE Mark expansion for mass spec-based IVD assays, are lowering institutional barriers to adoption and creating new routinization pathways for mass spec in clinical workflows.

Public funding priorities — such as an increase in NIH structural-biology and proteomics funding — have directly influenced procurement cycles, particularly within academic and translational research centers.

Two policy vectors will be particularly consequential in 2026:

Device quality and clinical readiness: The FDA’s QMSR update (effective February 2026) raises the floor for quality systems expected of vendors supplying instruments that contribute to clinical decision-making. Buyers should demand QMSR-aligned documentation as routine in RFPs and audit trails.

Environmental monitoring mandates: Rules requiring lower detection limits for emerging contaminants impose technical requirements that make HRMS a compliance necessity for many labs. This creates sustained base demand for instruments and analytical services beyond clinical and research spending cycles.

Our report is designed as an executive-grade playbook, not a catalog of static figures. Key actionable components include:

Investment decision frameworks that translate instrument performance and total cost of ownership into financial and operational scenarios tailored to hospitals, CROs, public labs, and industrial QC teams.

Vendor battle-cards covering product roadmaps, service models, channel reach, and certifiable quality systems — enabling procurement teams to create defensible supplier shortlists.

Regulatory impact matrices tying global rule changes to procurement risk and time-to-deployment, including mitigation playbooks for clinical labs and OEM partners.

Use-case-driven ROI templates for priority applications (clinical TDM workflows, PFAS/environmental monitoring, proteomics platforms), allowing finance teams to model payback under conservative and aggressive adoption scenarios.

M&A and partnership heatmaps identifying white spaces where bolt-on acquisitions or co-development agreements can accelerate access to end markets or enable bundled service offerings.

The report synthesizes primary interviews with laboratory directors, OEM product leaders, and regulatory experts, plus quantitative analysis of shipment trends, installed-base replacement cycles, consumables and service pricing, and public funding flows. Forecasts blend bottom-up unit economics with top-down adoption curves and are stress-tested against regulatory and macroeconomic scenarios to reveal upside and downside trajectories for 2026 planning.

Procurement managers: Use the vendor battle-cards and ROI templates to convert technical specs into board-level CapEx justifications and to design multi-vendor proof-of-concept timelines that preserve interoperability options.

R&D and Translational Heads: Prioritize investments in platforms that accelerate downstream clinical translation; align instrument choices with grant and reimbursement timelines to maximize utilization.

Investors and corporate development teams: Use our M&A heatmaps and concentration metrics to identify consolidation targets and service models that can be scaled through existing customer bases.

2026 represents a transition year where regulatory clarity, product maturation, and expanding non-clinical mandates will together convert latent demand into concrete procurement and partnership activity. Organizations that treat HRMS decisions as multidimensional — balancing instrument capability with lifecycle economics, compliance readiness, and platform interoperability — will capture disproportionate value. PW Consulting’s report gives decision-makers the scenario-tested insights and operational playbooks necessary to turn market momentum into durable competitive advantage.

This preview highlights the strategic framing and principal conclusions of our Worldwide High Resolution Mass Spectrometry System Market report. For detailed segment tables, vendor scorecards, pricing matrices, and the full set of model assumptions that underpin our forecasts, please visit the report landing page to access the complete study and supporting data packages.

For detailed analysis of this topic, please visit the official page:Worldwide High Resolution Mass Spectrometry System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com