Tall Oil Fatty Acid Market Report 2034: Key Drivers, Global Size, and Future Outlook

Other |

2026-06-10 11:49:26

As companies position for the next wave of performance and resilience, PW Consulting’s latest Worldwide Thiochemicals Market report outlines the commercial stakes and strategic options for 2026 and beyond. The thiochemicals market has demonstrated steady growth since 2020, expanding from an estimated USD 2.61 billion in 2020 to approximately USD 3.26 billion in 2025. Our forecast anticipates continued expansion at a compound annual growth rate (CAGR) of 4.51% across the 2026–2032 horizon, with the market approaching roughly USD 4.44 billion by 2032. These headline numbers mask a complex interplay of raw-material volatility, shifting end-market dynamics, and consolidation trends that will determine winners and laggards in the coming 18–36 months.

Worldwide Thiochemicals Market

Timing of investment and capacity decisions: With EBITDA margins sensitive to feedstock swings, organizations considering debottlenecking, brownfield expansions, or greenfield entry need an evidence-based view of volumes, demand elasticity, and cost pass-through dynamics. Our market model translates the aggregate CAGR into scenario-linked capacity utilization profiles to help prioritize capital allocation.

Worldwide Thiochemicals Market

Procurement and supply-chain risk management: Thiochemical producers are uniquely exposed to elemental sulfur and sulfur-derivative price volatility. Recent market signals show meaningful swings in sulfur availability and cost—factors that can represent a material portion of cash cost for certain mercaptan production routes. Our report quantifies the sensitivity of product margins to sulfur price bands and models hedging and vertical integration outcomes.

Worldwide Thiochemicals Market

M&A and partnership targeting: Moderate concentration among incumbent producers creates opportunity windows for strategic acquisitions and offtake agreements. We provide a prioritized list of acquisition targets, capability gaps versus market needs, and a playbook for value-accretive combinations that preserve supply security while unlocking technical synergies.

Sustainability and regulatory compliance: Buyers and regulators are increasing scrutiny on sulfur-handling, emissions from H2S-based processes, and lifecycle footprints. The report maps regulatory trends and provides practical compliance and decarbonization pathways that protect market access while delivering cost-competitive production profiles.

The thiochemicals value chain is anchored to elemental sulfur and derived sulfur streams. Industry practice converts elemental sulfur into intermediates such as H2S and methyl mercaptan, which are then routed into a variety of specialty and commodity-grade thiochemicals. Consequently, sulfur market dynamics are a primary driver of cost and availability. Notably, recent industry intelligence flagged sharp sulfur spot price volatility and projected contract-price uplifts in early 2026—developments that ripple through producer cash costs, margin structures, and the economics of new capacity.

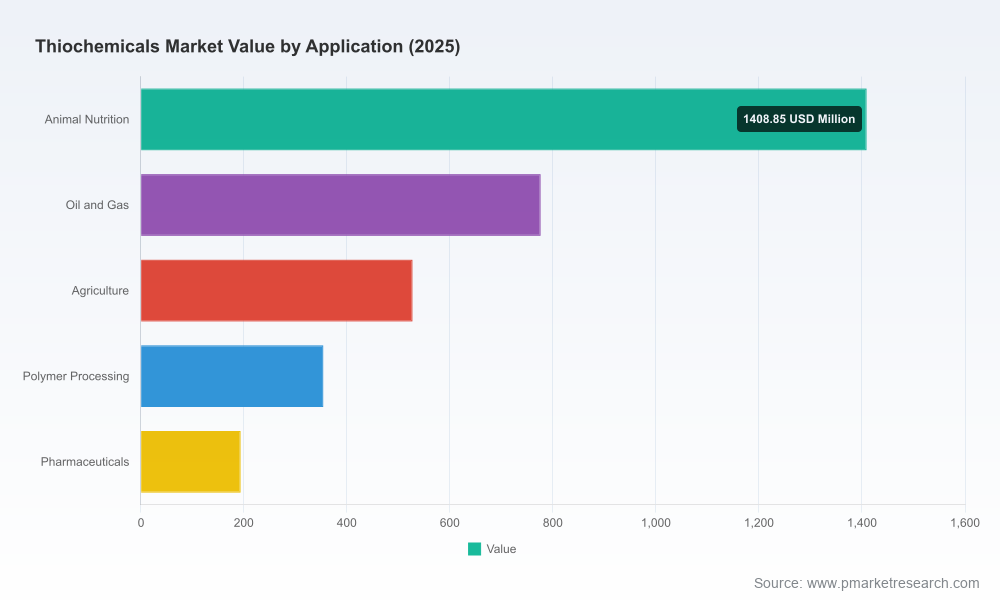

Demand drivers are equally multifaceted. Long-established end markets such as petrochemical refining and animal nutrition continue to absorb substantial volumes, while adjacent growth pockets—including certain polymer processing applications and specialty agrochemical intermediates—are becoming more relevant to mid-cycle strategic planning. The combined effect is a market that is neither purely cyclical nor purely secular; instead, firms must navigate overlapping horizon risks and near-term shocks.

The competitive field blends multinational platform players with regional specialists and specialty-house vendors. PW Consulting’s proprietary ranking shows a market that is meaningfully concentrated among top global producers while still offering niches where smaller, technically focused firms capture premium segments.

Arkema (France) — A global leader in organosulfur chemistry with multi-continent manufacturing footprints and an integrated portfolio spanning gas odorants, lubricant additives and specialty mercaptans. Arkema’s recent disclosures underscore capacity optimization and sustainability commitments; the firm has been active in incremental capacity moves to meet refining and industrial demand.

Chevron Phillips Chemical Company LLC (United States) — A major producer with vertically integrated capabilities that serve refinery and specialty markets. Their asset base and technology capabilities position them to exploit scale economies as feedstock conditions normalize.

Specialty and regional players (Europe, Japan, China) — Firms such as BRUNO BOCK, Daicel, Toray Fine Chemicals, and a cohort of Chinese producers provide differentiated products for cosmetics, fine chemicals, and agricultural intermediates. Their technical expertise and proximity to specific demand clusters afford higher margin opportunities, albeit at smaller absolute scale.

Laboratory and high-purity suppliers — Companies like Merck KGaA sustain the high-value tail of the market providing ultra-pure reagents and small-batch specialty thiochemicals for pharma and life sciences, a segment with different risk-reward metrics than commodity-supply chains.

Overall, market concentration metrics indicate a non-fragmented landscape where the top tier controls a significant share of global supply. This structure creates predictable bargaining power for larger producers but also leaves openings for nimble specialty houses that can defend premium niches through quality, service, and regulatory compliance.

Hedge and diversify sulfur sourcing: Given sulfur’s outsized impact on cash cost, firms should adopt multi-pronged procurement strategies—long-term contracts, tolling arrangements, and selective vertical integration—tailored to product-value chains where sulfur input is most material.

Prioritize modular, de-risked capacity moves: Debottlenecking and small-scale modular expansions often deliver better risk-adjusted returns than large greenfield projects in a market with moderate but steady growth. We provide a roadmap that links incremental investment tranches to scenario-based demand triggers.

Accelerate sustainability roadmaps that matter to buyers: Practical interventions—fugitive emission controls, sulfur recovery optimization, and transparent lifecycle data—are increasingly table stakes with global OEMs and large formulators. Early movers capture procurement preference and can command premium pricing in regulated markets.

Value chain partnerships over pure-play capacity bets: Co-development agreements with downstream formulators and strategic offtake partnerships mitigate demand risk and accelerate commercialization of higher-margin specialties.

Integrated market model: Forecasting at product and aggregate levels with scenario toggles for sulfur-price shocks, feedstock disruptions, and demand up/downside cases—designed for CFOs and strategy teams to stress test investment and pricing strategies.

Procurement and cost-sensitivity playbook: Quantified input-cost elasticities, sourcing strategies, and a toolkit for implementing hedges, tolling agreements, and feedstock diversification approaches.

Competitive intelligence dossiers: Executive profiles, capability matrices, and likely strategic trajectories for major players—useful for M&A screening, JV selection, and supplier rationalization.

Regulatory and sustainability tracker: A calendar of regulatory milestones, emissions/handling best practices, and CAPEX implications for compliance and low-carbon transition options.

Commercial playbooks: Go-to-market strategies for new entrants and incumbents—including contract structures, pricing levers, and channel strategies tailored to different end-market archetypes.

To illustrate the report’s decision utility: we model a scenario where sulfur contract prices rise materially in a single quarter. Under that stress-case the math favors firms with integrated sulfur handling or long-term offtake arrangements, and penalizes those operating on spot procurement for sulfur-sensitive intermediates. The model quantifies the EBITDA impact, payback period for securing long-term feedstock contracts, and the threshold at which tolling or upstream integration becomes the rational strategic response.

Run a 90-day procurement and capex stress-test using our scenario templates to identify immediate vulnerability points and quick-win mitigation actions (inventory strategies, short-term offtake, selective hedging).

Initiate a targeted M&A screening based on our deal-readiness matrix if strategic scale or feedstock security is required to meet your 2028–2032 ambitions.

Deploy a sustainability gap analysis aligned to your largest customers’ procurement policies; prioritize initiatives that deliver both regulatory compliance and commercial differentiation.

For 2026, decisions in the thiochemicals space will turn less on single-year demand forecasts and more on integrated choices about feedstock security, targeted capacity investment, and differentiated product positioning. PW Consulting’s Worldwide Thiochemicals Market report provides the quantitative backbone and executable frameworks that senior leaders need to make those choices with confidence. Our “trailer” approach here highlights the strategic contours and key risks—while the full report delivers the proprietary datasets, model access, and granular playbooks needed to operationalize an advantaged strategy.

Executives seeking the complete market model, company dossiers, and tailored scenario analysis should consult the full report on PW Consulting’s site. The detailed segmentation, supplier maps, and our actionable annexes are available only in the full publication to preserve the competitive integrity of the insights and to support bespoke advisory engagements.

For detailed analysis of this topic, please visit the official page:Worldwide Thiochemicals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com