Hydraulic Fracturing Well Testing Services Market Size, Share, Driving Trends, and Industry Forecast by 2032

Other |

2026-07-13 10:52:52

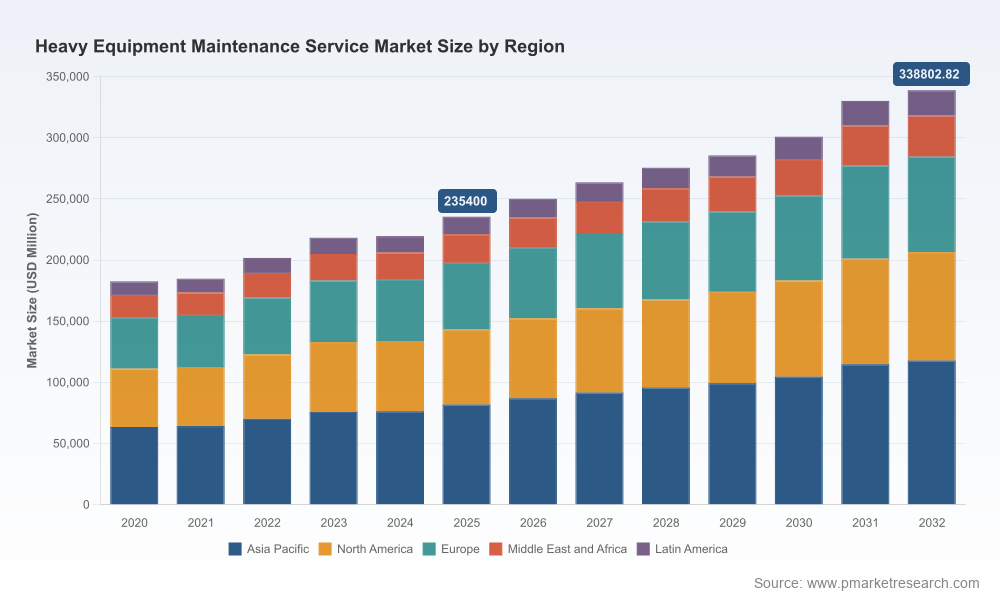

PW Consulting’s new market study, “Worldwide Heavy Equipment Maintenance Service Market (Base Year: 2025) — Strategic Outlook 2026–2032,” delivers the evidence-based perspective executives need to translate macro momentum into executable 12–36 month strategies. The global services market for heavy equipment maintenance is estimated at USD 235,400 Million in 2025 and is projected to expand at a 5.34% CAGR through our forecast window, with the market trajectory continuing into 2032. This briefing explains why that trajectory matters for capital allocation, service network design, and digital transformation priorities in 2026 — while preserving the detailed, proprietary segment and regional tables that are available in the full report.

Worldwide Heavy Equipment Maintenance Service Market

Translating growth into margin: A mid-single-digit CAGR masks heterogeneity across service types, customer cohorts, and geographies. Boards and commercial leadership must move beyond headline growth to understand how maintenance portfolios and aftermarket offerings produce differentiated margin streams for OEMs, dealers, and independent service providers. Our report quantifies those dynamics and maps them to near-term investment levers.

Worldwide Heavy Equipment Maintenance Service Market

Operational resilience in tighter labor markets: Technician shortages and wage inflation are no longer local tactics issues — they are strategic constraints. With median technician wages rising more than 14% year-over-year to USD 36.50 per hour in 2025 and many shops reporting understaffing, service capacity planning and skills pipelines are now material enterprise risks. The study prescribes workforce and outsourcing scenarios calibrated to preserve uptime while containing service cost inflation.

Worldwide Heavy Equipment Maintenance Service Market

Regulatory and compliance timing: OSHA updates effective in recent cycles increase the compliance load for digital documentation, operator certification, and safety record-keeping. Compliance investments will change total cost of ownership calculations for many heavy-equipment fleets; our scenario analyses show when and where those investments pay back.

Concise market sizing and probabilistic forecasts: We provide an audited baseline for 2020–2025, and a segmented forecast for 2026–2032, including alternative scenarios that model macroeconomic sensitivity, commodity cycles, and capital spending patterns.

Decision-ready frameworks: Cost-to-serve, service-mix optimization, and aftermarket parts economics models that can be used immediately to stress-test P&L and service margin targets at the enterprise and business-unit level.

Service network playbooks: Options for hybrid dealer/OEM service networks, franchise models, and strategic partnerships with independent service providers — including risk matrices for outsourced repairs versus in-house capabilities.

Digital and telematics monetization blueprints: End-to-end guidance on integrating OEM telematics, third-party maintenance platforms, and software-as-a-service that improves predictive maintenance capture rates without compromising data governance.

Workforce strategy and talent economics: Recruitment, retention, and apprenticeship models tailored for high-cost regions and growth markets, plus sensitivity analysis on labor-rate inflation and technician shortages.

Regulatory and safety compliance templates: Minimum viable digital documentation and certification pathways that reduce audit risk and support scaled service delivery.

Vendor intelligence and M&A leads: Profiles of strategic and disruptive players across OEMs, parts remanufacturers, and software vendors — with a focus on capability gaps and partnership opportunities.

Prioritize capital by risk-adjusted uptime ROI: Use the report’s ROI templates to prioritize investments in preventive and predictive capabilities where uptime dollars exceed replacement costs.

Right-size service footprints: Apply our network optimization tools to determine where direct service centers, authorized dealer investments, or third‑party partnerships deliver the best cost-to-serve.

Make workforce investments strategic: Use the labor economics scenarios to design targeted apprenticeship programs, automation deployments, and remote-diagnostic capabilities that compress service cycle times and reduce dependence on scarce technicians.

Negotiate smarter with software and telematics vendors: Leverage the comparative vendor analysis and integration playbooks to structure contracts that protect proprietary data, enable predictive analytics, and share upside with fleet customers.

The heavy equipment maintenance ecosystem remains fragmented: the aggregate market shows robust scale but relatively modest top‑tier concentration. Leading OEMs and large independents are expanding capability sets to capture higher-value aftermarket flows while software vendors enable new service delivery models.

Caterpillar Inc. — a full-spectrum incumbent — continues to combine dealer-supported preventive programs, parts distribution, telematics-enabled diagnostics, and rebuild programs to protect customer uptime across construction and mining fleets.

Komatsu Ltd. — leveraging its dealer network and KOMTRAX telematics — is pushing preventive-care bundles and remote monitoring as retention levers in mature and growth markets alike.

Volvo Construction Equipment — through ActiveCare uptime services — exemplifies an OEM strategy that links telematics insights to bundled service SLAs and genuine parts ecosystems.

John Deere (Deere & Company) — with Connected Support — is integrating diagnostics, parts logistics, and dealer interventions to serve mixed fleets where construction and agriculture overlap.

Liebherr, Hitachi Construction Machinery, SANY, and XCMG — each maintains broad service networks and emphasize spare-parts availability and component overhaul capabilities, adapting local service models to regional fleet economics.

DEUTZ Corporation — through recent strategic acquisitions — is extending its engine- and heavy-repair footprint in the Americas, signaling consolidation opportunities in component-level servicing.

HCSS and Fleetio — representative software players — are catalyzing productivity improvements via maintenance management, telematics integration, and analytics; manufacturers and large rental fleets are increasingly integrating these platforms into operations.

Recent M&A and network moves underscore near-term dynamics. Notably, DEUTZ pursued bolt-on acquisitions to broaden heavy‑repair capabilities in the Americas, and other service network expansions announced in late 2025 and early 2026 reflect intensified competition for serviceable hours and parts share. These transactions, and their integration challenges, are profiled in company-level case studies in the full report.

Labor economics are the primary immediate constraint. Technician wages and shop labor rates increased materially in 2025 — with median wages rising and many shops increasing hourly rates — while technician supply remains constrained, particularly among younger cohorts. These shifts drive higher per‑repair labor cost and make remote diagnostics, standardized repair kits, and modular component replacements more attractive.

Regulatory changes around digital documentation and operator certification raise the cost of noncompliance and create a first-mover advantage for firms that standardize digital maintenance records and operator training processes.

Telematics and predictive analytics are reaching a maturity inflection point: successful pilots are being operationalized, but monetization varies by service model. The report quantifies common pitfalls in data ownership and OEM-versus-fleet commercialization strategies.

Parts lifecycle management and remanufacturing are emerging margin sanctuaries. Firms that can reduce lead times and stabilize parts pricing will secure higher aftermarket margins even as equipment lifecycles elongate in some segments.

This announcement is a strategic preview designed to surface the structural insights that matter to senior teams. We have deliberately withheld granular regional and service-type breakdowns from this release — including detailed percentage splits and line-item revenue by region and service type — to preserve the report’s proprietary value. The full report contains the specific segmentation tables, regional forecasts, and service-level economics that operational teams will need to execute plans in 2026.

Lock in short-cycle uptime wins: Invest in targeted predictive maintenance pilots where telemetry data density and parts availability are high; convert pilots to paid SLAs within 9–12 months.

Hedge labor exposure: Combine selective automation, modular repair strategies, and strategic partnerships with third-party providers to mitigate technician shortages while preserving service levels.

Prioritize M&A selectively: Seek acquisitions or alliances that fill service capability gaps (component repair, mobile service fleets, software integration) rather than broad geographic expansion that is costly to integrate.

PW Consulting’s full “Worldwide Heavy Equipment Maintenance Service Market” report contains the comprehensive data tables, regional and service-type segmentation, company profiles, and actionable implementation playbooks referenced here. For executives preparing budgets, revising dealer agreements, or scoping acquisition targets in 2026, the report provides the granular inputs required to make defensible decisions. Visit our report page to access the complete dataset, model files, and bespoke advisory options.

For detailed analysis of this topic, please visit the official page:Worldwide Heavy Equipment Maintenance Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com