Why Choose BodyTite Liposuction in Dubai for Your Body

Health |

2026-06-08 05:59:36

PW Consulting’s latest market research on the Worldwide Bandage Contact Lenses market provides a focused, action-oriented view for corporate leaders, investors, and clinical program directors preparing strategy for 2026 and beyond. The study synthesizes historical market performance, a robust forecast through 2032, a regulatory and reimbursement playbook, and an actionable competitive analysis — all organized to support real-world commercial and clinical choices while reserving detailed, proprietary segment tables for subscribers.

Worldwide Bandage Contact Lenses Market

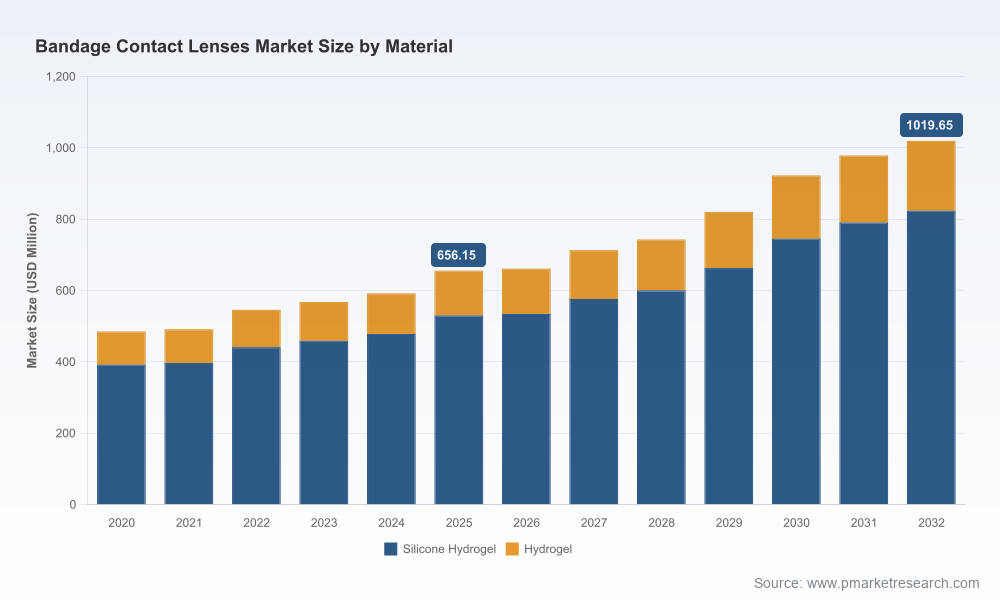

Acceleration into therapeutic wear: After steady expansion between 2020 and 2025, the market reached an estimated total of USD 656.15 Million in 2025, and is projected to continue on a compound annual growth rate (CAGR) of 6.5% through the 2026–2032 forecast window. The trajectory reflects rising adoption of silicone hydrogel technologies, broader therapeutic indications, and improving reimbursement pathways — trends that will shape go-to-market choices in 2026.

Worldwide Bandage Contact Lenses Market

Consolidation yet opportunity: Market concentration is meaningful — the top three players account for more than sixty percent of the market (CR3 ≈ 62.4%), and the top five capture roughly four-fifths (CR5 ≈ 78.5%). For incumbents, this confirms the defensive value of product differentiation and post-market clinical programs; for challengers, it signals the importance of focused niche plays (veterinary, first-aid, or regional OEM supply) and creative partnership models.

Worldwide Bandage Contact Lenses Market

Regulatory and reimbursement inflection points: Bandage contact lenses are regulated as Class II medical devices in the U.S., requiring 510(k) clearance for therapeutic claims. Parallel developments in coding and payer policy — including the practical application of fitting codes (e.g., CPT 92071) and separate supply reporting methods — are reducing friction for clinical adoption, but also raise documentation and evidence hurdles that commercial teams must address now.

Five strategic playbooks designed for distinct buyer types: incumbent device manufacturers, new entrants, contract manufacturers, specialty distributors, and ophthalmic clinical teams. Each playbook maps specific KPIs, investment thresholds, and near-term execution steps for 12–24 month horizons.

Regulatory roadmap and submission templates: A distilled 510(k) readiness checklist, recommended clinical endpoints for therapeutic labeling, and a comparative table of recent clearances that showcases precedent-setting predicate claims and supporting evidence strategies.

Reimbursement operational guide: Practical coding flows, payer submission templates, and audit-risk mitigation steps tied to the most common claim pathways for therapeutic lens fitting and supply.

Commercial model scenarios: Three go-to-market archetypes (premium-differentiated, low-cost OEM, and channel-aggregator) with revenue sensitivity to pricing, utilization, and payer mix. Each scenario includes break-even timelines and recommended pilot geographies.

Supply chain and manufacturing playbook: Sourcing priorities for high-Dk/t silicone hydrogels, cost-to-serve models for high-diameter specialty lenses, and contract-manufacturing qualification criteria to preserve regulatory traceability.

Investor diligence appendix: Quick-reference scorecards for M&A or minority-investment targets, including red flags for clinical evidence, quality systems, and commercial scalability.

The competitive structure blends large, vertically integrated incumbents with a set of focused specialists and regional manufacturers. Leading global eye-care companies maintain therapeutic-labeled silicone hydrogel portfolios and strong clinical distribution networks; specialist firms focus on material innovation, veterinary applications, or price-competitive supply to hospital channels. Recent regulatory clearances by new entrants demonstrate that product innovation and well-constructed regulatory strategies can secure market entry.

Global incumbents: Established vision-care firms have two structural advantages — recognized therapeutic predicates that ease regulatory pathways, and deep clinical relationships that accelerate adoption in surgical and emergency settings. Their strategic playbook will likely emphasize label expansion, bundled post-op programs with surgeons, and scale-driven manufacturing optimization.

Specialists and regional players: Companies concentrating on material science, veterinary lenses, or first-aid products create adjacent opportunities. These firms can win on niche clinical value, faster product iteration cycles, and targeted reimbursement education campaigns aimed at specialty clinics.

New regulatory entrants: Recent 510(k) clearances during 2025 have fortified competitive pressure. These events highlight that with a focused evidence package and alignment to predicate devices, new silicone hydrogel constructs can obtain clearance and enter therapeutic channels. Expect incremental pricing pressure and selective substitution in hospital formularies as these products become available.

Regulatory approvals in late 2025 expanded the set of available silicone hydrogel therapeutic lenses, increasing supplier options for hospitals and eye clinics.

Product catalog refreshes from niche manufacturers have broadened veterinary and first-aid offerings, creating cross-sell opportunities for distributors servicing mixed veterinary and ophthalmic practices.

Payer practice updates and clearer coding guidance for therapeutic contact lens fittings are lowering commercial friction, but they also necessitate improved claims documentation and outcome reporting from manufacturers and clinics.

Prioritize label and evidence strategy. Companies targeting therapeutic claims should finalize targeted clinical endpoints, ensure alignment with recent 510(k) precedents, and design pragmatic post-market surveillance that feeds commercial storytelling. For 2026, an adaptive evidence plan — combining targeted clinical cohorts with real-world registry data — will accelerate payer acceptance.

Lock in supply chain resilience for high-Dk/t materials. Silicone hydrogel remains the technological focal point for therapeutic wear. Manufacturers and contract suppliers should secure polymer supply contracts and qualify secondary production sites to mitigate single-point disruptions.

Build distributor and clinical channel partnerships. Given concentration among leading purchasers, new entrants should pursue narrow, high-impact pilots with surgical centers or specialty clinics to create case-series evidence and local KOL support before broader rollouts.

Design reimbursement enablement kits. Success in 2026 will depend on the ability to make purchases administratively easy for clinics and hospitals: pre-populated coding templates, payer-contact dossiers, and educational modules for billing staff reduce adoption friction.

Explore bundling and service innovation. Consider post-operative service bundles (lens + fitting + tele-follow-up) to increase value capture and differentiate from commodity lenses available via distributors.

Assess M&A or partnership for scale. For players seeking rapid access to therapeutic channels or geographic reach, selectively targeting bolt-on acquisitions or exclusive distribution partnerships can be more time- and capital-efficient than greenfield expansion.

Beyond market sizing and a seven-year forecast, this research is designed as a practical execution toolkit. Subscribers receive the complete segmentation matrices, scenario model files that allow you to stress-test price and utilization assumptions, sample 510(k)-style evidence strategies, and payer engagement templates. The “trailer” you are reading now demonstrates our depth; the full intelligence pack contains the specific segment-level outputs and competitive revenue models you will need to finalize 2026 budgets and operational plans.

If you are an executive optimizing a therapeutic lens portfolio: prioritize evidence and reimbursement pilots, and request the dossier of comparator predicate claims included with the full report.

If you are a commercial leader at a distributor or hospital system: use the supplied payer-template kit to run a pilot program, and consult the scenario model to estimate margin impact and utilization breakpoints.

If you are an investor or M&A advisor: leverage the investor diligence appendix to screen targets against quality-system and clinical-evidence KPIs before committing diligence resources.

PW Consulting’s Worldwide Bandage Contact Lenses report positions you to convert the market’s projected growth (CAGR: 6.5% through 2032) into commercially viable moves in 2026. For complete segment tables, company-level benchmarking, and downloadable scenario models, request the full report and supporting datasets through our research desk.

For detailed analysis of this topic, please visit the official page:Worldwide Bandage Contact Lenses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com