Messaging Gateways Security Market Overview: Key Drivers and Challenges

Other |

2026-06-26 08:34:59

PW Consulting today releases an executive preview of our forthcoming market intelligence: the Worldwide Skin Perfusion Pressure (SPP) Testing Devices Market report. As healthcare providers, device manufacturers, investors, and policy teams plan for 2026, the evidence and scenarios in this study provide a practical, action-oriented roadmap. This preview highlights the near-term market trajectory, competitive dynamics, regulatory and reimbursement vectors, and the tactical playbook leaders will need to convert opportunity into scalable revenue — while reserving core segment detail for the full report.

Worldwide Skin Perfusion Pressure Testing Devices Market

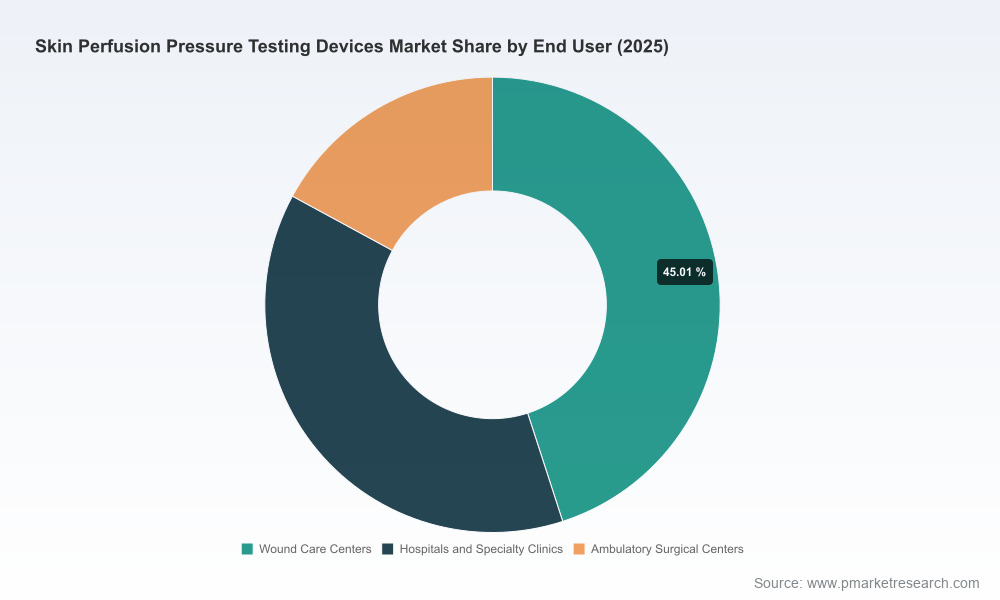

Skin perfusion pressure testing has moved from a niche diagnostic adjunct to a tactical clinical tool where microvascular assessment directly influences care pathways in wound management, vascular surgery, and diabetic limb preservation. Our analysis traces a clear acceleration in market adoption across clinical settings, driven by improving device ergonomics, tighter integration with wound-care protocols, and stronger clinical evidence demonstrating SPP’s role in predicting healing outcomes.

Worldwide Skin Perfusion Pressure Testing Devices Market

The overall market size illustrates that momentum. After rising from an estimated USD 178.5 Million in 2020 to USD 235.0 Million in 2025 (base year), the market is projected to expand to approximately USD 265.3 Million in 2026 and reach USD 348.6 Million by 2032 — reflecting a compound annual growth rate (CAGR) of 5.8% across the forecast window. These headline figures make the SPP device category a consistently growing specialty market with attractive margins for differentiated technologies and service-led models.

Worldwide Skin Perfusion Pressure Testing Devices Market

The full PW Consulting report is constructed to be operationally useful. Subscribers will get:

To honor the “trailer” principle, this public preview communicates the themes and strategic implications buyers need to evaluate in 2026, while the full report provides the granular segmentation, regional breakdowns, and downloadable datasets required for transaction-level decisions.

The market exhibits a moderate degree of concentration: the top three players account for a significant share of device revenues, and the top five firms capture a larger majority. This market structure shapes competitive strategy — scale matters, but there remains room for focused innovators that can deliver clinical differentiation or superior economics for care providers.

Recent vendor moves illustrate two clear competitive vectors in 2026: (1) incremental performance improvements (firmware, algorithmic filtering, sensor fusion) to improve diagnostic confidence in complex patients, and (2) commercial plays that bundle devices with services and training to accelerate clinical adoption. These priorities influence both product roadmaps and the nature of partnership conversations.

SPP devices are treated within established non-invasive vascular testing regulatory categories in major markets. For novel entrants and iterative device upgrades, a clear 510(k) strategy and early dialogue with regulators materially reduce technical and timeline risk. Payers evaluate SPP utilization through existing non-invasive vascular study codes and local coverage policies; therefore, manufacturers that can articulate and measure downstream clinical and economic benefits (e.g., improved wound-healing rates, fewer revascularizations) will find it easier to secure favorable reimbursement positioning.

Additionally, clinicians and guideline bodies continue to debate niche indications — for example, the role of SPP in patients with heavy vessel calcification — which affects positioning in specialty versus generalist care pathways. Companies that support peer-reviewed research in these areas will benefit from faster guideline adoption.

Our report is designed as a decision-support toolkit for 2026. It blends rigorous market modeling, validated primary research, and tactical playbooks to help executives prioritize investments, shape commercial models, and de-risk regulatory pathways. The dataset provides hospital- and clinic-level use-case insights and scenario stress tests to model ROI under varying adoption curves.

For executives planning launches, partnerships, or M&A in 2026, the report translates market momentum — from USD 235.0 Million in 2025 to an estimated USD 265.3 Million in 2026 and onward to USD 348.6 Million by 2032 — into concrete steps that reduce execution risk and accelerate value capture.

This preview highlights the strategic contours of the SPP device opportunity. For comprehensive datasets, detailed segmentation, vendor scorecards, and the practical templates required to operationalize these insights, access the full report. PW Consulting’s team is available to discuss tailored briefings, bespoke scenario modeling, and support for M&A diligence or go-to-market planning.

Invest strategically in 2026: the SPP testing market is maturing, and the winners will be those who convert device performance into measurable clinical value and durable commercial models.

For detailed analysis of this topic, please visit the official page:Worldwide Skin Perfusion Pressure Testing Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com