Middle East and Africa Testing, Inspection, and Certification (TIC) Market Analysis: Supply Chain, Pricing, and Forecast 2025 –2032

Health |

2026-07-06 08:25:37

PW Consulting’s latest market study on the Worldwide Mobile Phone Protective Cases Market delivers the actionable intelligence executives need to set priorities for 2026. With a clear historical base (2020–2025) and a forward-looking forecast (2026–2032), the report quantifies a durable expansion pathway — driven by device replacement cycles, accessory premiumization and faster feature adoption — and models an expected compound annual growth rate of 7.34% through the forecast window. The base-year assessment (2025) and our scenario outputs for 2026–2032 provide the foundation for investment, sourcing and go-to-market decisions in the year ahead.

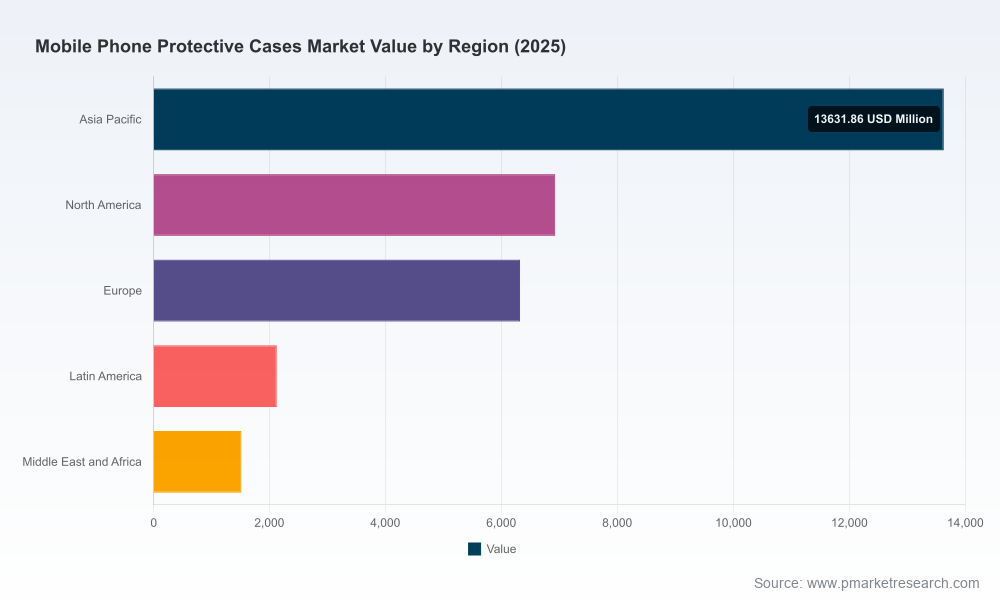

Worldwide Mobile Phone Protective Cases Market

Timing of strategic moves: 2026 will be a year when supply-chain restructuring, regulatory compliance and feature-led product differentiation intersect. Companies that align product roadmaps and sourcing strategies to these inflection points will capture outsized share and margin.

Worldwide Mobile Phone Protective Cases Market

Trade and regulation are no longer peripheral risks: tariff regimes and materials restrictions will materially affect landed costs and compliance obligations; our report quantifies exposure across sourcing scenarios and product archetypes.

Worldwide Mobile Phone Protective Cases Market

Channel economics are shifting: consumers are buying more accessories online and expect faster fulfillment, personalization and integrated payment/financing options — requiring operators to reassess channel mix and margin models.

Validated market sizing and growth trajectories from 2020 through 2032, anchored on the 2025 base year and segmented by product architecture, distribution model and region (note: granular segment tables are available in the full report).

Scenario-based demand models showing the sensitivity of revenue and margin to device launch cadence, tariff intensity, raw material inflation and premiumization rates.

Competitive benchmarking and strategic positioning maps for 12+ leading brands, including product-technology differentiation and go-to-market strengths.

Supplier-sourcing heatmaps and a supplier risk index to prioritize nearshoring, dual-sourcing or reshoring investments.

Regulatory compliance playbook for REACH and other jurisdictional material mandates, plus an operational checklist for product testing and documentation.

Commercial playbooks: pricing elasticity matrices, retail vs. DTC margin optimization templates, and partnership frameworks for carrier/OEM collaboration.

M&A and partnership diagnostic to identify tuck-in targets and integration playbooks that accelerate scale without eroding brand equity.

Resilient, mid-single-digit-plus growth: The accessory market continues to expand on a multi-year basis, supported by sustained device replacement cycles, more consumers opting for premium protective solutions, and rising feature-led demand (MagSafe, integrated lens protection, antimicrobial finishes). This creates both volume and margin opportunities for firms that can execute quickly.

Raw material and manufacturing cost volatility: TPU resin and other polymer inputs have shown notable price elasticity; for example, recent quarters have seen upward pressure on TPU pricing. Firms must integrate commodity hedging and supplier scorecards into 2026 procurement plans to preserve gross margins.

Regulatory tightening and compliance overhead: New material mandates in key markets (phthalate-free and equivalent restrictions) increase the cost of non-compliance. Product development calendars must include material qualification windows and contingency formulations to avoid recalls or market access delays.

Tariff exposure and sourcing shifts: Trade measures targeting accessory imports have made landed-cost management a strategic priority. Executives should evaluate nearshoring and multi-hub manufacturing models to mitigate tariff drag and reduce single-source exposure.

Brand and channel premiumization: Consumers increasingly pay for differentiated design, integrated features (e.g., MagSafe compatibility), and personalization. At the same time, the market remains fragmented: our concentration analysis shows the top three players account for a modest share of sales, indicating room for consolidation and brand-led scale plays.

Quality and safety risks demand operational rigor: Recent large-scale recalls remind manufacturers and distributors that design-for-safety, supply-chain traceability and post-market surveillance are operational imperatives.

The market is populated by a spectrum of specialists and generalists. From rugged-defensive brands to slim-design incumbents and direct-to-consumer personalization plays, each cohort faces distinct strategic choices in 2026.

Rugged specialists (e.g., OtterBox, UAG, Mous): These brands compete on engineering depth and recognized protection claims. Their near-term opportunity lies in commoditizing premium protective attributes into long-tail SKUs while pursuing OEM/industrial partnerships for adjacency revenue.

Performance-slim players (e.g., Spigen, Ringke, Pitaka): Their advantage is in delivering slim profiles with feature compatibility (wireless charging, MagSafe). Priorities for 2026 include tight integration with evolving device interfaces and continued cost engineering to keep ASPs attractive.

Design and personalization leaders (e.g., Casetify, Nomad): These brands monetize style and storytelling. In 2026, expanding fulfillment footprints and modular personalization options will be critical to maintain higher ASPs and repeat purchase rates.

Value/rugged OEMs and scale manufacturers (e.g., ESR, Supcase): Their playbook centers on volume, channel partnerships and rapid product refreshes. Margin pressure suggests pivoting to proprietary materials or proprietary feature sets to avoid pure price competition.

Notable recent moves illustrate fast-follower behavior and product innovation: several leading firms introduced refreshed lines that emphasize device compatibility (latest-generation phone models), enhanced drop protection, and feature integration such as kickstands, MagSafe compatibility and lens protectors. These product initiatives signal that time-to-market and IP differentiation will be decisive in 2026.

Implement a three-horizon product roadmap that balances near-term SKU rationalization, mid-term feature integration (wireless charging, lens protection, antimicrobial finishes), and long-term material innovation (aramid, recycled composites).

De-risk supply chains with a dual-sourcing strategy: combine competitive manufacturing hubs with targeted nearshoring where tariffs and lead-times create disproportionate cost exposure.

Embed regulatory compliance into product development: allocate R&D calendar time for material qualification in regulated geographies and create a “compliance fast-track” for flagship SKUs.

Pursue selective premiumization: protect margin by bundling services (extended warranties, trade-in programs) and by introducing limited-edition collaborations with cultural partners to sustain ASPs.

Re-evaluate channel economics: prioritize online direct-to-consumer initiatives for higher lifetime value while negotiating performance-based economics with large retail and carrier partners.

Target M&A and partnerships that add manufacturing scale, proprietary materials or distribution reach. Given the industry’s modest top-tier concentration, well-executed consolidation can create strategic scale and higher bargaining power with platforms and component suppliers.

Operationalize product safety and traceability: invest in serialization and supplier audits to reduce recall risk and to shorten time-to-resolve should incidents occur.

Custom market-sizing and scenario work tailored to your SKU mix, channel footprint and sourcing map, including tariff-pass-through and material-cost sensitivity analyses.

Supply-chain redesign and negotiation support to implement dual-sourcing, nearshoring pilots and inventory optimization for shorter lead-times.

Regulatory and product-compliance playbooks and audit checklists for rapid certification across major markets.

Commercial transformation modules: DTC growth playbooks, retail-negotiation frameworks, and pricing-engine implementation to capture premiumization upside.

M&A advisory for bolt-on and roll-up strategies that create defensible scale, proprietary tech ownership and distribution reach.

The mobile phone protective cases market is at a strategic crossroads heading into 2026: robust overall growth and clear pockets of premium opportunity coexist with elevated cost and regulatory headwinds. With an industry structure that remains relatively fragmented, the next 12–18 months will reward companies that move from tactical product launches to integrated strategies — aligning materials, manufacturing, compliance and channel economics. PW Consulting’s full report provides the granular tables, regional and product splits, and company-level financial proxies that enable precise investment decisions; executives seeking the complete dataset and a tailored briefing can access our full release and advisory services on the PW Consulting website.

For detailed analysis of this topic, please visit the official page:Worldwide Mobile Phone Protective Cases Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com