Building a Better Learning Experience with SevenMentor

Other |

2026-07-15 10:38:37

PW Consulting today releases an executive companion to our comprehensive Worldwide Plant Activator Market report (base year 2025, forecast 2026–2032). As agricultural input portfolios shift toward lower-residue, biologically driven solutions, plant activators are transitioning from niche tools to strategic levers for yield resilience, integrated pest management, and sustainability-linked market access. This briefing summarizes the report’s strategic value for corporate leaders planning 2026 initiatives—product launches, portfolio prioritization, go‑to‑market investments, and M&A—while reserving the granular segment tables and scenario models for the full report.

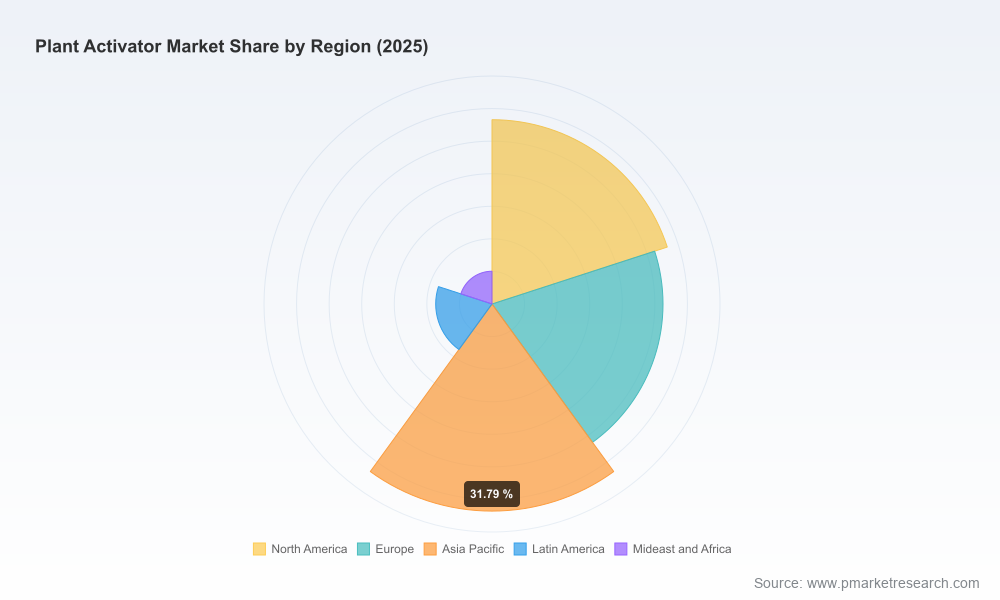

Worldwide Plant Activator Market

Following sustained growth across 2020–2025, the worldwide plant activator market reached approximately USD 1,450.5 Million in 2025 (base year). Our forecast, built on primary interviews, proprietary field-trial syntheses, and regulatory pipeline modelling, projects a compound annual growth rate (CAGR) of 6.78% through 2032. That trajectory lifts the market to roughly USD 2,296.1 Million by 2032, with the first forecast year (2026) showing continued expansion over the 2025 baseline. The rate reflects accelerating commercial adoption of biological activators, shortening regulatory timelines for qualifying biologicals in key markets, and growing farmer incentives for low-residue, climate-resilient inputs.

Worldwide Plant Activator Market

Timing of commercial launches: The 2026 planning horizon is a pivot point. With regulatory windows narrowing for biological approvals in Europe and several expedited pathways available in the U.S., firms that align late‑stage development and registration investments to submit dossiers by mid‑2026 can capture first-mover advantages in 2027–2028 commercial cycles.

Worldwide Plant Activator Market

Portfolio rationalization: As activators migrate from adjunct experimental use to standard IPM and biostimulant stacks, R&D and marketing budgets should be rebalanced toward combination formulations and application protocols. Our analysis shows value migration to products that demonstrate clear yield and quality delta under abiotic stress—those should be prioritized for scale-up.

Channel and farmer economics: Subsidy programs in several EU markets and select national schemes encourage adoption of biological inputs. Companies that construct channel incentives and education investments tailored to subsidy eligibility will accelerate on‑farm trials and early uptake in 2026–2027.

M&A and partnership windows: Consolidation remains moderate—the top three players do not dominate the market outright, and the top-five concentration indicates a mid‑level fragmentation profile. This creates attractive targets for bolt-on acquisitions of niche biological platforms, precision fermentation capabilities, or formulation specialists that enable differentiation at scale.

Forecast framework: Annual market sizing (historical 2020–2025, forecast 2026–2032) with scenario lanes that stress-test adoption under regulatory, commodity price, and climatic shock scenarios.

Segment intelligence: Granular segmentation by region, product type, and application with proprietary price‑elasticity modelling and SKU-level revenue curves—intended to help product managers prioritize SKUs and allocate marketing spend. (Segment breakdowns are intentionally not reproduced in this press summary.)

Competitive playbooks: Company-level strategic profiles, capability maps, and acquisition likelihood scoring to guide BD and corporate development teams in 2026 pursuit planning.

Regulatory and go‑to‑market checklists: Practical timelines, dossier templates, and post‑registration stewardship recommendations for biologicals and low‑residue chemistries across key jurisdictions.

Field-evidence synthesis: Meta-analysis of efficacy trials by crop class and stress condition, including confidence weightings for repeatability and scale effects—designed for quick integration into sales pitchbooks or extension programs.

The market is shaped by an interplay of global crop protection majors, specialised biological developers, and regional innovators. Market concentration metrics indicate room for both scale and differentiated specialists—CR3 and CR5 are consistent with an industry in oligopolistic transition rather than full consolidation. The following competitive observations are derived from primary interviews, patent landscape mapping, and public disclosures:

Syngenta (Switzerland) leverages its global distribution and portfolio bundling ability to position systemic activators as part of integrated disease management packages. Their Actigard offering exemplifies a strategy of embedding activators alongside conventional chemistries in high-value fruit and vegetable segments—an approach other multinationals may emulate to defend premium channels.

BASF SE (Germany) is pivoting toward combined root growth and stress resilience solutions, reflecting a broader industry pivot to dual‑benefit products. Their emphasis on formulations that support nutrient mobilization enhances adoption among growers focused on input efficiency.

Certis Biologicals (U.S.) differentiates through microbial-based activators and a field-evidence centric go‑to‑market. Recent trials that evaluate disease suppression via induced resistance demonstrate the commercial pathway for microbial activators in potatoes and other row crops.

NutriAg / HGS BioScience and Gowan Company represent the mid‑market innovators bringing unique technologies—ACE/LEX platforms and amino-acid/peptide formulations—that are well-suited for licensing or bundling with seed and fertilizer offerings.

Futureco Bioscience, Isagro, Plant Health Care plc, and other EU/Med players combine biotech R&D with regional go‑to‑market nuance; they are likely acquisition targets for global players seeking localized scientific benches and distribution networks.

Lier Chemical (China) has a strategically important local IP position with its Methiadinil small‑molecule activator—an example of a domestic innovation that can alter competitive dynamics in large regional markets if regulatory hurdles are cleared. Recent registration reviews in China underscore the regulatory complexity that buyers must model into valuation.

UPL and other India-headquartered firms are positioned to scale via cost‑efficient formulation and distribution in emerging markets, making them logical partners for rapid geographic extension of biological portfolios.

Product innovation continues: New small-molecule and microbial activators reached public visibility in 2025, including Methiadinil and new biologicals launched through partnerships. These innovations demonstrate the dual pathways for competition—novel chemistry and refined biologicals.

Regulatory momentum favors biologicals in many jurisdictions: Europe’s streamlined approval for qualifying biologicals and multiple U.S. tolerance exemptions for microbial strains reduce time‑to‑market for many activators. However, registration reviews (for example, teratogenicity data requests in China) can materially delay local commercialization and must be stress‑tested in launch plans.

Supply chain and input dynamics: The shift toward microbial fermentation and precision fermentation platforms increases reliance on biotech CMO capacity and predictable biological raw-materials supply—areas where long‑lead agreements or vertical integration may offer competitive advantage.

Prioritize late‑stage regulatory submissions for products with clear multi‑year stewardship and efficacy packages; fast-track trials in jurisdictions offering accelerated biological pathways.

Structure M&A screens to prioritize platform technologies (e.g., fermentation, elicitor chemistry) and regional players with high-quality local data—these assets can be integrated into global go‑to‑market engines with moderate execution risk.

Design commercial pilots that align with subsidy and sustainability programs to accelerate adoption, and pre‑load agronomic support content to shorten farmer learning curves.

Invest in formulation science and compatibility testing to enable bundling with fertilizers and seed treatments—combination offerings will win shelf and field trials.

Model regulatory and data‑generation costs explicitly into ROI calculators; different jurisdictions carry asymmetric data requirements that can erode near‑term margins if not anticipated.

The full Worldwide Plant Activator Market report is a decision-ready deliverable for corporate strategy, BD, and product teams. It contains downloadable model files, step-by-step regulatory checklists, M&A candidate scoring, and a field‑trial meta‑database designed to be repurposed into commercial trial design. This press summary highlights strategic directions; the full dataset and proprietary segment matrices—the engine of tactical decisions—are available in the full release.

For executives preparing 2026 strategy cycles, our recommendation is to convene a cross‑functional steering group (R&D, regulatory, commercial, BD) in Q3 2025, use the PW Consulting scenario models to stress-test portfolio choices, and secure at least one partnership or acquisition due-diligence slot focused on biological platform technologies by Q2 2026. To access the complete report, proprietary models, and a tailored briefing with PW Consulting’s senior analysts, please visit the report landing page or contact our global advisory desk.

PW Consulting’s Worldwide Plant Activator Market report converts emerging science and policy signals into concrete actions. In an era where biologicals are rapidly evolving from experimental adjuncts to core inputs, this analysis equips leaders with the timing, priority, and risk lens required to turn 2026 initiatives into market share and sustainable growth.

For detailed analysis of this topic, please visit the official page:Worldwide Plant Activator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com