Industrial Automation Driving the Future of Axial Flow Compressor Technologies

Other |

2026-05-18 13:08:35

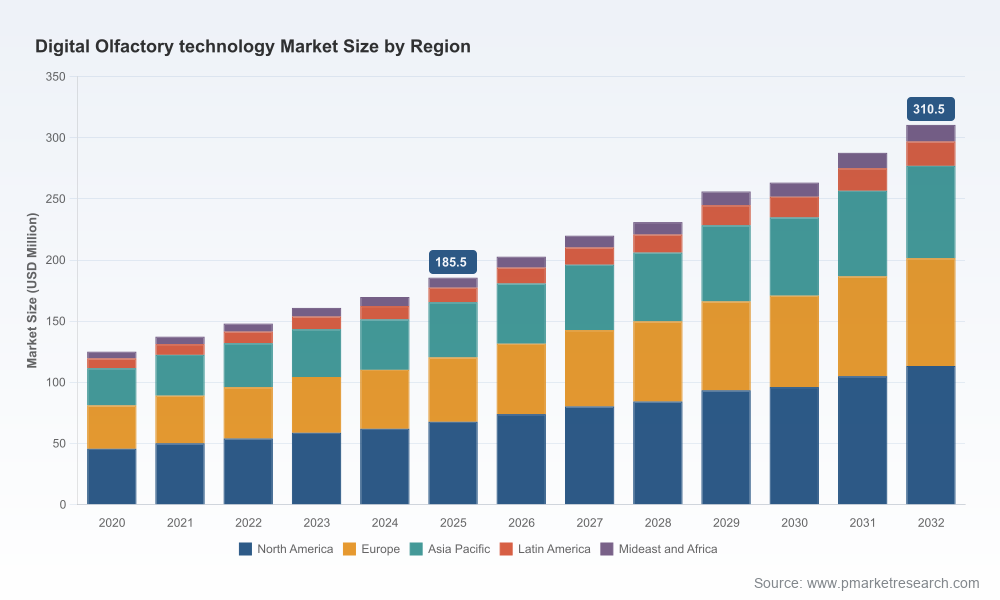

As companies across manufacturing, healthcare, consumer electronics, and immersive media reassess their innovation roadmaps for 2026, digital olfactory technologies are moving from niche research curiosity to operationally relevant capability. PW Consulting’s latest market study — anchored on a 2025 base year and a rigorous 2026–2032 forecast — projects a sustained compound annual growth rate (CAGR) of 7.63%. Our model shows global market value roughly doubling in the forecast window, reflecting accelerating commercialization, new sensor modalities, software-led differentiation, and the maturation of business models such as SmellTech-as-a-Service.

Digital Olfactory technology Market

This brief explains why that trajectory matters for executive decision-making in 2026, what strategic moves separate winners from laggards, and how our full report supplies the practical tools leaders need to execute with confidence. Per the “trailer” principle of this release, we present high-confidence, actionable insight while intentionally withholding the granular segmentation tables and revenue-by-region breakdowns that are available in the full report on our portal.

Digital Olfactory technology Market

Commercial readiness: 2025–2026 marks a transition from laboratory demonstrations to products and manufacturing scale-up. Several vendors have moved from prototype to productionized modules and scent synthesis systems, enabling real-world pilots.

Digital Olfactory technology Market

Regulatory and standards inflection points: Medical device classifications, evolving calibration standards, and upcoming symposia are aligning incentives for interoperable solutions and credible clinical pathways.

Value chain unlocking: Software analytics and platformization are shifting value from hardware alone to data and models, enabling continuous improvement despite persistent sensor drift and environmental variability.

Our forecast model — built from historical performance (2020–2025) and scenario-based drivers for 2026–2032 — quantifies a clear expansion opportunity. The market’s mid-single-digit to high-single-digit CAGR reflects two parallel dynamics: steady adoption in industrial and quality-control applications, and rapid experimentation in consumer and entertainment domains where multisensory UX is becoming an investment priority.

For 2026 strategy-setting, three implications follow:

Prioritize platform and API architectures. Early adopters who embed olfactory telemetry into existing IoT and analytics stacks will lock in downstream revenue from analytics and model licensing.

De-risk early pilots by partnering with established sensor and synthesis vendors rather than attempting in-house full-stack development. The vendor landscape is fragmented and specialized; pragmatic integration accelerates time-to-value.

Plan for regulatory gatekeeping in healthcare and certain safety applications. Certification timelines and clinical validation requirements should be baked into 2026 product roadmaps and procurement decisions.

Driver — Software and AI: Advances in machine learning for pattern recognition, drift compensation, and scent mapping are multiplying the impact of incremental hardware improvements. Commercial models are moving from one-off analytic reports to subscription analytics and ontology services.

Driver — Vertical use-cases: Food & beverage quality control, clinical diagnostics (breath analysis), environmental monitoring, and immersive entertainment are generating differentiated requirements that are accelerating modular product development.

Bottleneck — Hardware reliability: Sensor drift, calibration needs, and sensitivity to temperature and humidity remain the most frequently cited technical obstacles. Buyers should evaluate vendors on their calibration protocols, field recalibration tooling, and environmental compensation strategies.

Bottleneck — Standardization: Ongoing efforts to define interoperability, performance metrics and test protocols are nascent. This creates short-term vendor lock-in risk but long-term opportunities for companies that lead standard-setting activities.

Regulatory context: Some olfactory diagnostic devices fall under established medical device regulation; classification and special controls exist in major markets. Firms pursuing clinical or diagnostic claims must align R&D and QA investments with regulatory requirements from the outset.

The competitive field mixes deep technical specialists, AI-first entrants, and legacy sensory-analysis vendors. Market concentration is moderate: the top-three players control a significant minority of revenue, while the top-five collectively account for roughly half of the market — a structure that favors both focused scale-ups and partnering with established leaders.

Osmo (Elizabeth, NJ, USA) — An AI-native player focused on teaching machines to read, write and map scents. Osmo’s Olfactory Intelligence platform and recent commercial investments signal an aggressive push to own fragrance-ingredient discovery and scent teleportation as IP-rich product lines. Notably, Osmo’s 2026 facility expansion and reported patent outputs underscore its intent to scale manufacturing and proprietary models rapidly.

Ainos, Inc. (Houston, TX, USA) — Brings a MEMS-based, full-stack electronic nose with strong sensitivity and a service-led commercialization model. The company’s late-2025 commercial module launch and SmellTech-as-a-Service positioning make it a practical partner for industrial and semiconductor customers seeking reproducible, field-deployable sensors.

Aryballe Technologies (Grenoble, France) — Specializes in biomimetic sensors coupled with optics and ML. Its strength lies in integrated sensor-software packages tailored to industrial and healthcare analytics, making it a candidate for co-development in regulated environments.

Alpha MOS (Toulouse, France) — A pioneer in electronic nose and tongue systems with deep adoption in food, beverage and aroma profiling. Legacy domain expertise and established customer relationships give it advantage in quality-control workflows.

Olorama Technology (Spain) — Focused on scent synthesis and multisensory experiences for VR/AR and cinema. Its patented scent synthesizers and creative integrations position it as the go-to vendor for entertainment and experiential marketing pilots.

Aroma Bit (Japan) — Developing odor imaging chips and e-nose modules; a vendor to watch for compact, low-power applications in consumer electronics.

The eNose Company (Netherlands) — Concentrates on medical breath analysis and screening devices; regulatory alignment and ISO 13485 certification make it a partner of choice for clinical pilots.

AIRSENSE Analytics GmbH (Germany) — Produces portable analyzers for environmental and industrial use, differentiating on ruggedness and field usability.

Recent industry milestones — including major facility openings, patent milestones, and commercial product launches — are accelerating the move from bespoke experiments to repeatable commercial deployments. Conferences and societies are consolidating knowledge and standards, further reducing buy-side uncertainty.

Value layering: Compete on integrated value — sensor + model + continuous learning — rather than single-component specs. Vendors that can monetize analytics and provide robust model-ops will command higher multiples.

Partnership ecosystems: Strategic partnerships across sensor manufacturers, cloud analytics, regulatory consultancies, and systems integrators will shorten pilots and reduce procurement friction.

Commercial models: Flexible pricing (SaaS, outcome-based, device-plus-subscription) will help overcome buyer reluctance to invest in early-stage hardware.

Standards leadership: Firms that invest in standards development and third-party validation will win enterprise trust faster, especially for safety-critical and clinical applications.

Forward-looking market model (2026–2032) with scenario analysis and sensitivity testing for adoption rates, price erosion, and business model splits.

Vendor benchmarking toolkit covering technology readiness, regulatory posture, manufacturing capability, and go-to-market fit. Includes scoring templates and RFP language to accelerate vendor selection.

Use-case playbooks for prioritized verticals (industrial QC, clinical diagnostics, consumer UX, environmental monitoring) with implementation timelines, KPIs, and cost/benefit examples.

Integration and deployment readiness checklist addressing calibration regimes, environmental compensation, and continuous validation protocols to mitigate sensor drift.

M&A and partnership heatmap identifying strategic targets, capabilities gaps, and integration synergies for strategic acquirers and corporate venturing teams.

Regulatory and standards dossier summarizing current classification frameworks, certification pathways, and implications for clinical claims and safety-critical deployments.

C-suite: Treat olfactory technologies as a strategic adjacence that can differentiate product platforms and unlock recurring revenue — allocate a small, protected budget for rapid pilots and partnerships in 2026.

Product leaders: Build modular interfaces and data contracts that allow olfactory telemetry to feed existing analytics; require vendors to deliver model-ops and calibration workflows.

Procurement & legal: Embed regulatory milestone clauses, performance SLAs, and escrow arrangements for critical ML models in supplier contracts.

R&D: Focus on drift compensation and environment-adaptive algorithms; consider co-development with sensor vendors to accelerate ruggedization.

Digital olfaction is entering a decisive growth phase. Our 2026-focused analysis shows that while the market is still consolidating, it is large enough and growing fast enough to justify deliberate corporate engagement. Organizations that move now — adopting interoperable architectures, securing strategic vendor partnerships, and aligning development programs with regulatory realities — will be best positioned to capture disproportionate value as the technology transitions from lab to mainstream.

For executives and practitioners preparing 2026 plans, PW Consulting’s full report provides the quantitative models, vendor due diligence tools, and executable playbooks necessary to act. To review the detailed segmentation tables, regional dashboards, and revenue-by-use-case models that underpin our conclusions, please consult the full report on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Digital Olfactory technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com