بي شوت في الرياض لتحقيق نتائج طبيعية ومستدامة

Home |

2026-06-16 06:14:45

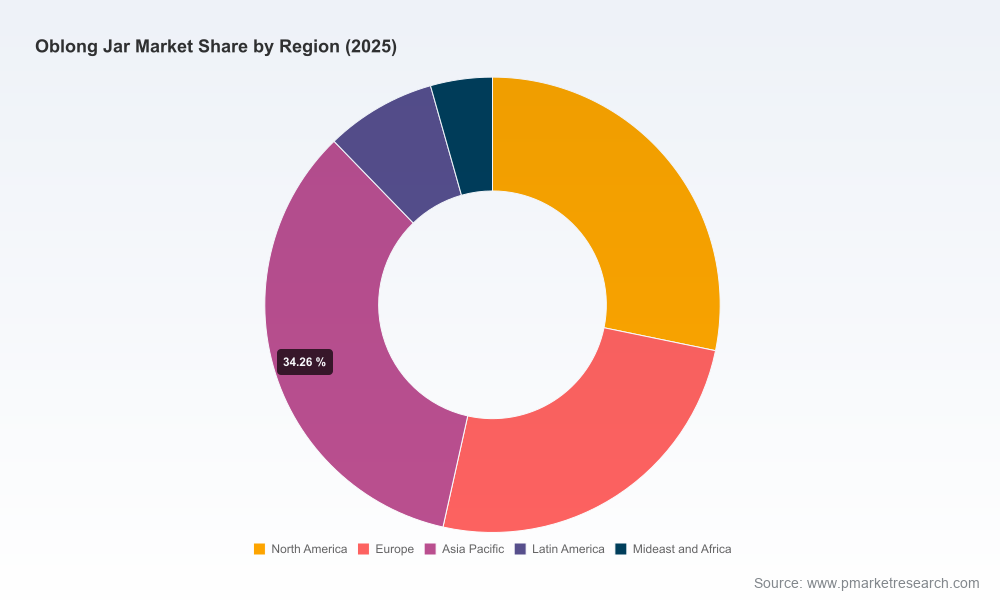

PW Consulting’s latest market intelligence on the Worldwide Oblong Jar Market, with a 2025 base year and a 2026–2032 forecast horizon, frames a pragmatic growth story for manufacturers, brand owners, and investors preparing decisions in 2026. Our topline sizing shows steady expansion from a 2025 base of USD 450.0 Million to an expected USD 669.99 Million by 2032, representing a compound annual growth rate (CAGR) of 5.85% across the forecast window. That trajectory masks important tactical inflection points — from raw‑material cycles to regulation-driven redesign mandates — that will determine winners and laggards as companies allocate capital and commercial effort next year.

Worldwide Oblong Jar Market

Demand momentum: The market’s mid‑single digit CAGR signals a category with healthy, durable demand—sufficient to justify capacity investment and product innovation, but not so rapid as to insulate incumbents from competitive disruption.

Worldwide Oblong Jar Market

Fragmentation: Industry concentration indicators highlight a fragmented supplier base (CR3 ~18.5%, CR5 ~24.3%), implying room for consolidation, scale plays, and channel specialization. Buyers retain negotiating leverage, yet scale economies matter for converters and distributors pursuing margin expansion.

Worldwide Oblong Jar Market

Cost and regulatory regime risks: Upstream cost volatility and an accelerating regulatory landscape (notably Extended Producer Responsibility frameworks) will create bifurcation between companies that proactively redesign packaging systems and those addressing compliance reactively.

Raw material and manufacturing cost signals — Glass product manufacturing prices remain elevated, with the US Producer Price Index for Glass and Glass Product Manufacturing reported at 182.420 in March 2026. For commodity glass jars, FOB converter pricing for mass‑produced soda‑lime formats sits in a narrow low‑cost band (approx. USD 0.18–0.35 per unit for common 8–16 oz SKUs), underscoring margin sensitivity to throughput and procurement contracts.

Regulatory momentum — Several US states now require producer responsibility for packaging. California’s EPR targets are especially consequential for formulation and material choices: 30% recycling rates by 2028, 40% by 2030 and 65% by 2032. Similar proposals and bills elsewhere create a rising compliance staircase that will materially affect material mix, design-for-recyclability choices, and end‑of‑life cost allocations.

Category economics — The market path from 2020 through 2025 shows a recovery and re‑acceleration pattern post‑2022, with 2025 acting as a pragmatic planning base. Our scenario models flag sensitivity to three variables: raw‑material price volatility, EPR cost pass‑through, and volume elasticity among downstream buyers (retail, industrial, cosmetic, and food processors).

The market features a mix of regional converters, national distributors, and a handful of legacy manufacturers serving specific channels. Key participants in the oblong jar value chain include Berlin Packaging, The Cary Company, Parkway Plastics (Parkway Jars), SKS Bottle and Packaging, O.Berk, Silgan Plastics, FH Packaging, and Illing Company. Collectively, these firms illustrate how supply models differ across channels: direct manufacturing, distributor-enabled fulfillment, and hybrid vertical offerings.

Berlin Packaging — Known for large footprint logistics and warehouse-retailer solutions. Strategic learning: logistics and assortment breadth create stickiness with large CPG customers; investments in distribution platforms will continue to be a high-payback lever.

The Cary Company — Supplier of functional, industrial-grade plastic jars with ergonomic features. Strategic learning: product differentiation via functional design (handles, wide mouths) supports margin premiums in industrial and commercial channels.

Parkway Plastics (Parkway Jars) — Longstanding producer with strong reuse/recycling narratives. Strategic learning: heritage producers can monetize sustainability pedigree as regulatory costs increase, but must back claims with measurable circularity plans.

SKS Bottle and Packaging & O.Berk — Distributors with broad SKU coverage across glass and plastic formats. Strategic learning: distributors will compete on integrated services—kitting, private label, and just‑in‑time replenishment—rather than on price alone.

Silgan Plastics & FH Packaging — Producers serving food and condiment markets through engineered containers. Strategic learning: food safety, barrier performance, and supply‑chain reliability are decisive procurement criteria for large food processors.

Illing Company — Niche supplier for industrial paste and wax applications. Strategic learning: niche specializations (resin variety, chemical compatibility) remain defensible and attractive for premium margin opportunities.

Across the competitive set, the clearest strategic plays are (1) scale and logistics integration to control cost and fill rates, (2) sustainability and circularity investments to preempt regulatory cost imposition, and (3) focused product engineering for channel‑specific needs (food safety, consumer aesthetics, and industrial durability).

This report is designed as an execution toolkit for 2026 decisions. It synthesizes historical performance (2020–2025), a detailed forecast (2026–2032), and operational modules you can deploy immediately:

Proprietary demand model and sensitivity matrices — scenario outputs at the SKU and resin/material level (note: detailed segment tables and downloadable datasets are reserved for subscribers).

Supply‑chain mapping and cost‑to‑serve analysis — factory footprints, logistics corridors, and break‑even curves for scale investments.

Regulatory impact assessment — granular modeling of EPR cost mechanics across major jurisdictions and implications for product redesign timelines.

Commercial playbooks — go‑to‑market templates for distributors and converters, customer segmentation and price elasticity guidance, and channel promotion strategies (retailer collaborative promotions, industrial direct sales, and DTC/brand partnerships).

M&A and partnership screen — target archetypes, valuation drivers, and integration checklists for consolidators seeking share or capability buys in a fragmented market.

Implementation roadmaps — stepwise timelines for cost reduction, circular design adoption, and SKU rationalization that align with regulatory milestones.

Procurement and hedging: Lock in strategic supply agreements for high‑risk inputs and evaluate hedging structures tied to glass and resin indices. Elevated glass PPI and low per‑unit glass pricing create a profile where scale and contract design determine margin capture.

Design for compliance: Prioritize material mixes and labels that meet upcoming EPR thresholds. For organizations selling into jurisdictions with aggressive EPR targets, plan redesign cycles now to avoid costly, last‑minute reformulations.

Channel segmentation: Use targeted product variants for high‑velocity retail SKUs and bespoke, value‑added formats for industrial customers. Distributors should bundle logistics and sustainability reporting to deepen buyer relationships.

M&A and partnerships: Seek bolt‑on acquisitions that close capability gaps—recycling partnerships, post‑consumer resin sourcing, and packaging engineering teams—rather than purely scale buys.

In line with the “teaser” approach of this brief, we present actionable strategic implications and market trajectories while preserving the granular segmentation tables, proprietary SKU‑level forecasts, and downloadable scenario models for the full report. That dossier contains the detailed regional, material and application‑level splits, contract pricing matrices, and the Excel‑based model purchasers use for transaction diligence. Access to those datasets will materially accelerate decision cycles and provide the precise inputs your commercial, procurement, and corporate development teams require.

For leaders preparing FY‑2026 planning rounds, the Worldwide Oblong Jar Market report from PW Consulting is designed to convert market visibility into executable initiatives. If your agenda includes capacity decisions, procurement renegotiation, regulatory compliance roadmaps, or targeted M&A, the report’s models and checklists will save months of analysis while reducing execution risk.

PW Consulting continues to track price indices, EPR legislation evolution, and competitive moves in real time. Our team stands ready to provide tailored workshops, scenario‑model updates, and integration support to convert the market intelligence into commercially viable outcomes for 2026 and beyond.

To access the full dataset, segmentation tables, and the Excel modeling suite, please consult the official report release on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Worldwide Oblong Jar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com