Worldwide Automatic Gearbox Valves Market — Strategic Outlook for 2026

Executive summary

PW Consulting’s latest market study on the Worldwide Automatic Gearbox Valves Market establishes a concise strategic baseline for 2026 decision-making. The market—measured in USD Million—registered a 2025 base of approximately 4,688.1 and is projected to expand to about 5,002.0 in 2026, with a compound annual growth rate (CAGR) of 5.12% across the 2026–2032 forecast window. By the end of the forecast period the model anticipates a market size consistent with long-term secular trends in powertrain electrification, tighter emission regulations and continuous improvements in transmission efficiency.

Worldwide Automatic Gearbox Valves Market

This release is intentionally positioned as a high-value executive preview: it surfaces prioritized strategic insights, risk triggers, and tactical implications for 2026 planning cycles while withholding detailed subsegment tables and granular regional or application-level figures to guide readers to the full report for complete operational intelligence.

Worldwide Automatic Gearbox Valves Market

Why this report matters for 2026 corporate planning

- Capital allocation: informs where to focus CAPEX and capacity expansion in the near term given projected market growth and supplier concentration dynamics.

- Product roadmaps: clarifies which valve technologies and valve-body integrations will drive differentiation as OEMs pursue fuel-economy and shift-quality targets.

- Supply chain resilience: highlights near-term raw material and production risks that should be addressed in procurement and sourcing strategies.

- Commercial & regulatory compliance: equips powertrain and transmission teams with the regulatory context needed to prioritize electronic control and validation investments.

Market dynamics shaping 2026 decisions

Three converging forces are shaping near-term strategy for gearbox valve makers, Tier‑1s and OEM powertrain organizations:

Worldwide Automatic Gearbox Valves Market

- Regulatory pressure: Stricter fuel economy and emissions mandates (including evolving USD and EU regimes) are accelerating demand for more sophisticated electronically controlled valve bodies that can optimize shift strategy and reduce losses across both conventional and electrified transmissions.

- Technology integration: The move toward electro-hydraulic integration, shift-by-wire architectures and hybrid powertrains is raising both technical and testing complexity. Valve architectures that enable precise pressure modulation, low power consumption and robust electronic interfaces will command premium positioning.

- Input-cost and materials volatility: Price swings in aluminum and specialty steels affect valve-body casting and spool machining economics, driving supply-chain redesigns, material-substitution strategies, and hedging considerations.

Competitive landscape — what incumbents and specialists are signaling

The gearbox valves market exhibits a mid-to-high level of consolidation: the leading three companies capture a meaningful share of global revenue, with the top five concentrating an even larger portion. This concentration creates both barriers and opportunities for new entrants and for adjacent suppliers seeking to scale quickly via OEM partnerships or tiered supply agreements.

Key participants and strategic postures worth noting:

- BorgWarner (Auburn Hills, Michigan) — Strengths in electro-hydraulic solenoids and valve-body assemblies give it a strong play in multi-speed and hybrid transmission programs. Expect emphasis on shift quality optimization and integration with vehicle control software.

- Aisin Corporation (Kariya, Aichi) — With deep OEM ties and in-house transmission manufacturing, Aisin’s integrated valve offerings are positioned for programs where OEMs prioritize vertical control and parts integration.

- ZF Friedrichshafen (Friedrichshafen, Germany) — Focuses on electronic-hydraulic system integration and passenger/commercial transmission platforms, pushing innovations that tie valve design closely to transmission control units.

- Bosch GmbH (Gerlingen, Germany) — Leverages a broad powertrain electronics portfolio to offer valve products as part of comprehensive control systems, emphasizing diagnostics and software-enabled value-adds.

- Specialists (TLX Technologies, HUSCO Automotive, Parker Hannifin, TLX, etc.) — These players excel at customized solenoid technologies and rapid engineering turnarounds; they are attractive partners for OEMs seeking differentiated valve performance or faster time-to-market on niche programs.

Recent market signals that should inform strategy:

- Facility expansion by a specialist supplier in late 2024 indicates capacity scaling to meet demand for electro-hydraulic valves used in shift-by-wire and start-stop systems.

- A major recall affecting a high-volume OEM’s transmissions due to a control valve defect underscores the reputational and warranty risk inherent in valve-system quality; it reinforces the value of stringent supplier qualification and end-of-line validation.

- Cross-industry partnerships demonstrating zero-emissions or low-emissions valve actuation tech illustrate how broader solenoid advances can be repurposed into automotive transmission control systems.

Strategic implications and recommended actions for 2026

PW Consulting recommends a pragmatic portfolio of strategic moves for OEMs, Tier‑1s and investors planning for 2026:

- Prioritize system-level differentiation: Invest in valve-electronics co-design and model-based control to secure OEM programs that value shift quality and efficiency gains over low-cost components.

- Hedge raw-material exposure: Implement commodity hedging, contractual indexation, and supplier collaboration programs to mitigate aluminum and specialty-steel price volatility affecting valve bodies.

- Balance vertical integration and strategic outsourcing: Where reliability and IP matter most, strengthen in-house capabilities; for scale and flexibility, form long-term partnerships with proven solenoid specialists.

- Double down on validation and field monitoring: Given the severe implications of control-valve failures, expand testing protocols, digital twin use for validation and aftersales telemetry to detect early failure modes.

- Optimize manufacturing footprint: Align capacity with regional demand patterns and lead-times—localize assemblies for high-volume platforms while centralizing specialized machining to contain fixed costs.

- Pursue targeted M&A and alliances: Look for acquisitions that add sensor-fusion, actuation efficiency or software calibration capabilities, rather than only incremental hardware scale.

- Embed regulatory foresight into product planning: Design valve systems with headroom for future emissions and efficiency targets to minimize mid-cycle redesigns and costs.

What’s inside the full PW Consulting report (practical deliverables)

The comprehensive report is structured to support executable decisions across commercial, engineering and procurement teams. Key deliverables include:

- Base-year market sizing and forward-looking demand model (by year through 2032) with scenario analysis and sensitivity testing.

- Segmentation analytics (by region, valve type and transmission architecture) with forecasted trends and adoption timelines.

- Competitive benchmarking and fifty-plus supplier profiles, including technology positioning, program wins, manufacturing footprint and strategic intent.

- Supply-chain maps, value-stream cost analysis and raw-material exposure models.

- Product-technology scorecards covering electro-hydraulic integration, spool materials/coatings, and lightweight casting options.

- Regulatory impact briefings and compliance roadmaps aligned to anticipated Euro and US standards.

- Deal tracker covering recent M&A, capacity investments, and strategic partnerships relevant to valve technologies.

- Action playbooks for procurement, manufacturing, product development and aftersales risk mitigation.

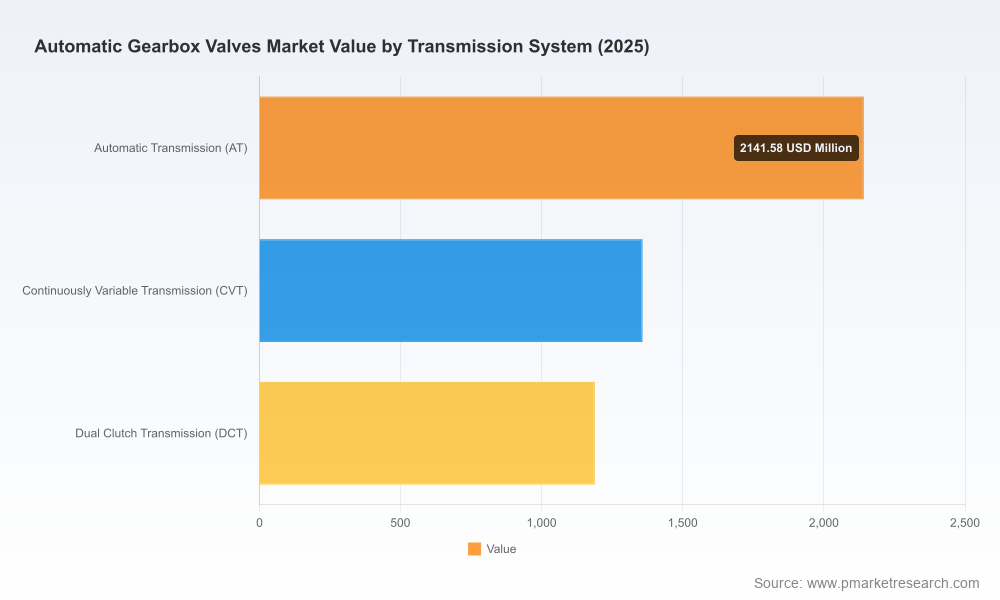

Please note: this executive release intentionally omits granular subsegment tables and specific regional/application-level percentages. Those detailed data tables, supplier-level revenue breakdowns and customer-program mappings are included exclusively in the full report and associated data appendices.

How to use this intelligence in 90/180/365 day plans

- 90 days — Rapid assessment: Run a supplier robustness check against our risk matrix; update commodity hedging triggers and accelerate validation protocols for critical valve families.

- 180 days — Tactical moves: Commit to shortlist partnerships for capacity scaling or technical collaboration; launch product re-engineering initiatives focused on power draw and thermal resilience.

- 365 days — Strategic positioning: Rebalance CAPEX toward integrated valve-electronics capabilities, consider acquisitions to plug capability gaps, and finalize localized supply strategies for prioritized platforms.

Next steps and access

For procurement directors, product leaders and corporate strategists preparing 2026 budgets, our report provides the decision-grade detail required to turn these insights into measurable outcomes. Access to the full dataset, supplier revenue breaks, regional forecasts and program-level intelligence is available through PW Consulting’s Worldwide Automatic Gearbox Valves Market report. Contact our advisory desk to arrange a briefing, obtain the complete dataset, or commission a tailored workshop aligning these findings to your product and supply-chain plans.

For detailed analysis of this topic, please visit the official page:Worldwide Automatic Gearbox Valves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com