PW Consulting — Strategic Brief: Worldwide Industrial and Electrical Fuses Market (2026 Outlook)

PW Consulting today releases an executive briefing drawn from our forthcoming market research: "Worldwide Industrial and Electrical Fuses Market, 2026–2032." Built on a detailed historical review (2020–2025) and forward-looking scenario modelling (2026–2032), the study provides the practical intelligence that executives, product leaders, procurement teams and corporate development groups will rely on when making strategic choices in 2026.

Worldwide Industrial and Electrical Fuses Market

Headline market context

At the aggregate level, the global industrial and electrical fuses market demonstrated steady expansion through the base period and is projected to maintain momentum across the forecast window. Our consolidated model shows growth from the mid‑2020s base to a high‑single‑digit cumulative uplift through the early 2030s, under a central-case compounded annual growth rate of 5.21% across the forecast period. The discipline of our approach—reconciling manufacturer output, installed base replacement rates, capex on power distribution and broad infrastructure programmes—means the topline figures are investment-grade inputs for 2026 planning.

Worldwide Industrial and Electrical Fuses Market

Why this matters for corporate decision-makers in 2026

- Planning precision: With a market expanding on a stable trajectory, capital allocation for new manufacturing, product development and M&A must align to medium-term demand rather than short-term cyclical noise. Our topline projections provide the time horizon investors need to size investments.

- Procurement and cost strategy: Raw-material volatility—most notably copper exposure within fuse elements and conductive hardware—can materially alter unit economics and competitiveness. Procurement teams will want to pair market demand forecasts with the commodity scenario work contained in the full report.

- Product and regulatory roadmaps: Standards and certification timelines are converging with product refresh cycles. Firms that sequence R&D, testing and certification efficiently can convert regulatory requirements into commercial differentiation.

- M&A and consolidation opportunities: Market concentration metrics indicate a sector where scale, distribution breadth and product depth create enduring advantages. Both strategic buyers and private equity sponsors will find our company-level coverage and screening tools actionable for deal origination.

Core dynamics shaping 2026 strategic choices

- Electrification and infrastructure investment — Ongoing electrification across industry, grid modernisation and expansion of transport electrification sustain demand for reliable overcurrent protection solutions. These drivers are durable and form the foundation of the forecast.

- Commodity cost cycles — Copper is a central input: sector analysis indicates copper accounts for a substantial share of costs in low-voltage fuse elements and associated hardware. Price volatility has been elevated; copper briefly surpassed USD 14,500 per tonne in January 2026, and market forecasters project a wide trading range for 2026. Sensitivity to these swings is modelled explicitly in the report.

- Standards and certification pressure — Recent and updated standards (for example EN IEC 60269-1:2025 and the North American UL 248 series) raise technical and testing thresholds for many product families. These changes create short-term compliance costs but also long-term opportunities for premium positioning.

- Supply-chain resilience — Lead times for specialized components and regional production footprint choices are now integral inputs to customer service levels. Manufacturing agility—nearshoring or multi‑site capacity—will be a decisive discriminator for suppliers competing on speed and reliability.

What the report contains — practical, actionable modules

The full PW Consulting study is organised to translate market intelligence into executable plans. Highlights include:

Worldwide Industrial and Electrical Fuses Market

- Top‑down and bottom‑up market sizing with reconciled demand drivers, replacement cycles and installed-base dynamics.

- Commodity sensitivity models that quantify margin exposure to copper and other key inputs across alternate price scenarios.

- Regulatory and standards matrix, with compliance timelines, testing requirements and likely certification bottlenecks by product family.

- Go-to-market playbooks and pricing frameworks tailored to industrial, energy/utilities, transportation and commercial customers.

- Supplier risk heatmaps and manufacturing footprint optimisation tools to support procurement and operations decisions.

- Competitive intelligence dossiers: strategy, product portfolios, channel coverage and capability gaps for the leading suppliers in the sector.

- M&A and partnership screening tools, including valuation frameworks calibrated to sector multiples and consolidation scenarios.

Competitive landscape — structure and strategic implications

The market exhibits moderate concentration: our concentration metrics indicate that the top three and top five suppliers capture a notable portion of global revenue, reflecting a competitive environment where scale and technical breadth both matter. This structure creates predictable channels for consolidation while leaving room for specialised entrants with differentiated technology or service models.

Leading firms covered in the report include established global industrial-electrical players and specialist fuse manufacturers. Each of these names presents a distinct strategic posture:

- Littelfuse, Inc. (Chicago) — Broad portfolio across industrial and semiconductor protection. Recent product presentations and technical seminars underscore a continuing focus on systems-level protection and aftermarket services; the company’s engagement with manufacturing technology forums in early 2026 highlights its emphasis on educational outreach and channel enablement.

- Eaton Corporation plc (Bussmann series) — Deep power-management and fuse offerings integrated into larger electrification product suites, creating cross-sell opportunities with switchgear and distribution solutions.

- Mersen S.A. — Strength in high-performance and semiconductor fusing that serves demanding industrial and power-electronics applications, a strategic asset as power-conversion equipment proliferates.

- ABB Ltd., Siemens AG, Schneider Electric SE — These electrification and automation leaders integrate fuses into broader power distribution ecosystems, using systems sales and project-level relationships to secure long-term demand.

- Specialists such as S&C Electric, SIBA, Schurter and Bel Fuse — Offer portfolio depth in utility, medium/high-voltage and niche industrial applications where reliability and specification compliance are paramount.

- Mid‑market manufacturers (e.g., DENCO Fuses) — Continue to compete on quality, responsiveness and specialist product variants in select geographies.

Strategic playbook for 2026

- Hedge and source: Create a layered procurement strategy that combines index‑linked purchase agreements, strategic stockpiles and alternative material exploration to mitigate copper price shocks.

- Prioritise compliance‑first R&D: Sequence product refreshes to align with the most impactful standard changes, converting compliance into a feature that supports premium pricing.

- Manufacturing footprint optimisation: Use scenario modelling to evaluate nearshoring versus centralised manufacturing, balancing labour, logistics and tariff exposures against service-level targets.

- Commercial segmentation: Distinguish offerings between project-driven utility business and recurring industrial replacement demand; allocate sales and service resources accordingly.

- M&A and partnerships: Target acquisitions that add channel access, testing/certification capabilities, or complementary product lines to enhance cross-sell potential without duplicative capex.

- Product innovation: Invest selectively in higher‑value fuses and integrated protection modules that embed sensing, diagnostics and remote monitoring—areas where OEMs and end users will pay for reliability and uptime.

Scenario insights: how 2026 could diverge

Our modelling includes three illustrative scenarios—base case, accelerated-electrification upside, and commodity‑stress downside. In the upside scenario, faster grid modernisation and transport electrification accelerate replacement and retrofit cycles, expanding addressable volumes. In the downside scenario, prolonged copper price shocks compress supplier margins, drive price pass-through frictions and incentivise substitution or extended service life initiatives. Each scenario maps to quantified impacts on unit economics and capital plans; the full report provides downloadable model workbooks for client use.

How to use this intelligence

Buy‑side executives should use the report to align procurement contracts and inventory policy with expected demand and price volatility. Product and engineering leaders will find the regulatory and performance matrices critical to prioritising certification efforts. Corporate development teams will use the competitive dossiers and consolidation scenarios to size and prioritise targets. Finally, operations managers can apply the manufacturing optimisation tools to reduce lead times and increase resilience.

Next steps

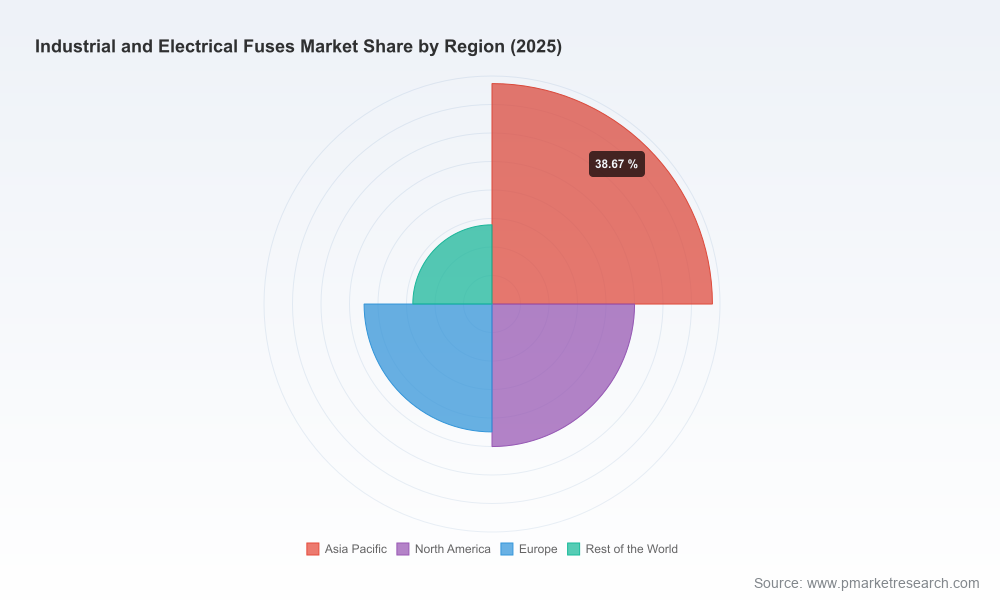

This briefing intentionally shows the depth and applicability of our analysis while omitting the detailed segmentation tables and proprietary, company-level market shares that are included in the full publication. PW Consulting’s complete report contains the granular regional, voltage-tier and end‑use segmentation models, downloadable scenario workbooks, supplier scorecards and transaction screening tools that corporate teams need to act in 2026.

To obtain the complete study, including the full set of segmentation matrices, methodology annex and the interactive forecasting models, please visit PW Consulting’s research page or contact your advisory representative. For organisations seeking bespoke modelling—tailored to a manufacturing footprint, procurement contract or acquisition thesis—PW Consulting offers customised engagements that operationalise the findings for rapid implementation.

For detailed analysis of this topic, please visit the official page:Worldwide Industrial and Electrical Fuses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com