PW Consulting: Aluminum Alloy Wheels Market Poised to Expand at 6.98% CAGR Through 2032

Other |

2026-06-29 17:21:17

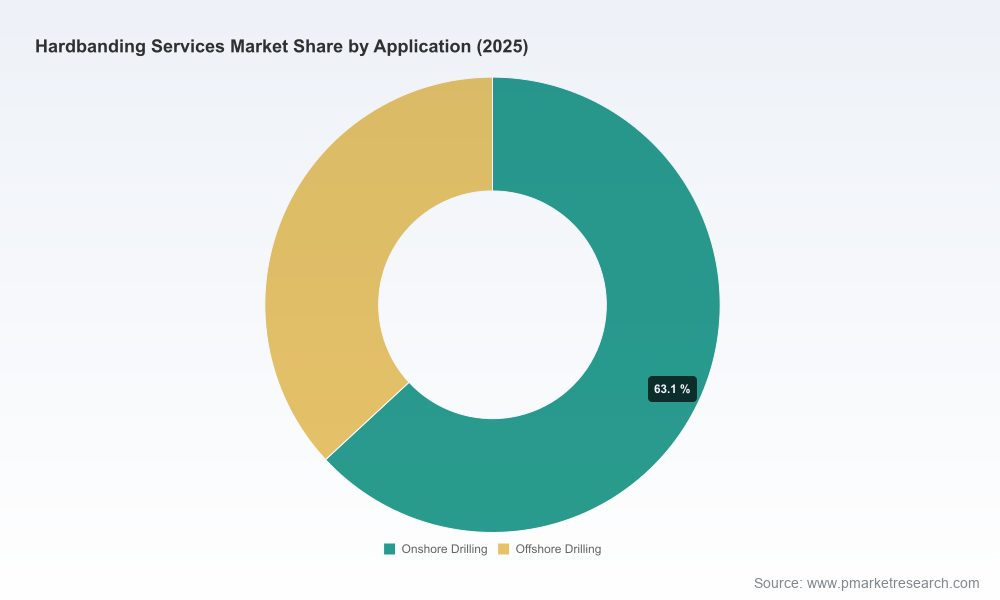

As upstream operators reset activity plans in response to cyclic oil and gas dynamics, hardbanding services are shifting from a tactical cost line item to a strategic equipment-protection program. PW Consulting’s new market study — covering historical performance (2020–2025) and a seven‑year forecast (2026–2032) — shows the global hardbanding services market reached approximately USD 450 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.1% through 2032, reaching roughly USD 637 Million by the end of the forecast window. Our analysis synthesizes field-proven service models, alloy and application trends, supply‑chain sensitivities, and competitive positioning to deliver decision-grade intelligence for 2026 planning cycles.

Worldwide Hardbanding Services Market

Budget prioritization: With predictable mid-single-digit CAGR growth, procurement and asset managers can plan multi‑year service contracts with greater visibility, optimizing total cost of ownership for drill‑string fleets rather than treating hardbanding as discretionary maintenance.

Worldwide Hardbanding Services Market

Supplier footprint and service model choices: Operators face a trade‑off between mobile on‑site applicators and centralized shop services. Our report maps these models to operational footprints and shows where network expansion or preferred‑provider agreements most materially reduce downtime risk.

Worldwide Hardbanding Services Market

Raw‑material and input price exposure: Key consumables—particularly tungsten carbide components used in wear‑resistant alloys—introduce a quantifiable procurement risk. We quantify how commodity price moves transmit to service pass‑throughs and advise on hedging and contract structures.

M&A and partnership timing: The market concentration metrics we track indicate a moderately consolidated supplier base. For corporate development teams, 2026 offers actionable windows for bolt‑on acquisitions and structured alliances that accelerate regional coverage without duplicative capex.

Historical performance and forecast model: A transparent, auditable financial model covering 2020–2025 with a 2026–2032 forecast built from bottom‑up service volumes, pricing scenarios, and macro linkages.

Scenario analysis and sensitivity matrices: Base, upside, and downside scenarios incorporating input cost shocks (e.g., tungsten carbide), drilling‑activity elasticity, and regulatory shifts; sensitivities for service pricing, utilization, and equipment life extension metrics.

Provider capability matrix: Operational profiles and capability heatmaps for leading hardbanding providers, assessing alloy portfolios, mobile vs. shop capacity, inspection and NDT integration, and preferred applicator networks.

Procurement playbooks: Contract templates and KPIs for fixed‑price vs. time‑and‑materials arrangements, SLA definitions tied to drill‑string availability, and recommended clauses to mitigate raw‑material pass‑through volatility.

Field testing & validation protocols: Step‑by‑step technical checklists for alloy selection, weld application controls, casing compatibility testing, and re‑application approval workflows aligned with industry standards.

Regulatory & compliance checklist: A concise guide to certification standards relevant to hardbanding consumables and application approvals, and how to document compliance for operator audits and insurers.

The market is served by a mix of global alloy specialists, integrated service providers, and regional mobile applicators. Market concentration is meaningful: our CR3 and CR5 metrics indicate the top three and top five providers account for a material share of market revenues, underscoring strategic advantages for scale, product breadth, and inspection service integration.

Hardbanding Solutions by Postle Industries (Cleveland, OH) — A recognized global leader with casing‑friendly, crack‑resistant alloys (Duraband NC, Tuffband NC) and a strong emphasis on application solutions. Their recent certification for re‑application approvals further cements their role in simplifying operator rework cycles.

Arnco Technology (Houston, TX) — Known for advanced alloy formulations (e.g., high‑performance XT grades) and heatless tungsten carbide options, Arnco’s technical orientation and preferred applicator network make it a strategic partner for operators prioritizing tool‑joint longevity and casing friendliness.

National Oilwell Varco (NOV) / Tuboscope (Houston, TX) — Integrates premium alloy offerings with inspection and drill‑pipe services, enabling a bundled value proposition that reduces interface risk between hardbanding and NDT/inspection workflows.

Castolin Eutectic (Lausanne, Switzerland) — Brings a long heritage in consumable development and rigorous wear testing; appeals to operators with complex abrasion, erosion, and sour‑service requirements.

Regional and mobile specialists — Firms such as Hard Band Industries, Pro‑Tech Hardbanding, Thompson & Thompson Group (W74), Bandit Tech, and Tech Energy Hardbanding provide critical on‑site capabilities, particularly in high‑activity basins where downtime avoidance is paramount.

Strategic takeaway: global alloy leaders drive material innovation and standards compliance, while regional mobile providers control the last mile of uptime. For 2026, operators should consider blended supplier strategies: a primary relationship with a globally certified alloy provider augmented by local mobile partners under a single SLA governance model.

Commodity exposure: Tungsten carbide remains a pivotal input for certain high‑wear alloys. Price moves and supply tightness materially affect cost pass‑throughs. For context, tungsten carbide pricing trends and the broader tungsten market size point to a stable but closely watched input market that operators and service providers cannot ignore when negotiating multi‑year agreements.

Standards and approvals: Industry approvals (for example, re‑application and consumable standards) materially alter permissible field practices. The emergence and adoption of formal approvals create differentiation for suppliers that secure them and add a compliance premium to their services.

Operational demand drivers: Upstream activity levels directly influence hardbanding volumes; as exploration and production programs normalize or expand, demand for tool‑joint protection—and therefore recurring hardbanding services—rises in lockstep, reinforcing the strategic value of long‑term supplier arrangements.

Service modality shift: We observe a gradual shift towards integrated offerings combining alloy supply, application, and inspection (NDT). Operators benefit from integrated SLAs that align application quality with inspection outcomes, reducing rework and unplanned downtime.

Adopt multi‑tier supplier strategies: Lock in material supply and technical approvals with at least one global alloy provider while maintaining regional applicator partners to ensure coverage and responsiveness.

Price‑index and hedging clauses: Insert commodity‑linked indexation or caps in multi‑year contracts for consumables tied to tungsten prices to protect both operators and providers from abrupt cost volatility.

Contractualize inspection outcomes: Tie payment milestones or bonus/penalty structures to NDT‑verified field performance (e.g., adherence to re‑application protocols and casing wear thresholds) to align incentives and reduce lifecycle costs.

Invest in capability audits: Before scaling a single supplier relationship, conduct operational audits that cover application procedures, mobile service readiness, and rework policies to avoid surprise compliance gaps.

Pursue targeted M&A or alliances: For service providers and private equity, focus on bolt‑on acquisitions that add mobile capacity or a preferred applicator network in strategic basins rather than duplicative capabilities.

Our study is designed as a practitioner’s guide: forecast models and scenario tools are delivered in editable formats, procurement playbooks are templated for rapid customization, and the provider capability matrix is built to plug into RFP and preferred‑supplier selection processes. We intentionally withhold the detailed segmentation tables and region/application line items from this release to ensure readers visit the report portal for full access to granular market splits, service‑level differentials, and calibrated price curves.

Certifications and approvals for re‑application pathways have reduced operational friction for certain alloy vendors, enabling faster turnaround on drill‑string life‑extension programs.

Industry publications and competitor intelligence released through 2025–2026 have increased transparency on alloy performance and pricing, tightening margins for undifferentiated service providers and elevating the premium for certified, casing‑friendly solutions.

Macro inputs such as tungsten carbide price movements and the broader tungsten market trajectory are contributing to a renewed focus on supply diversification and input indexation within contracts.

For operators, OEMs, and service providers setting 2026 budgets, PW Consulting’s Worldwide Hardbanding Services Market report is the operational toolkit you need to move from reactive maintenance budgeting to proactive asset‑protection strategy. Our report gives you the forecast, the scenarios, the supplier intelligence, and the procurement instruments to make decisions with conviction.

Access to the full report — containing the detailed regional and application segmentation, full supplier scorecards, and downloadable financial models — is available on our website. Engage with PW Consulting if you would like a tailored briefing or a customized scenario run for your fleet and procurement calendar for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Hardbanding Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com