Smart Badges Help North American Organizations Improve Workforce Management and Security

Other |

2026-06-30 14:10:54

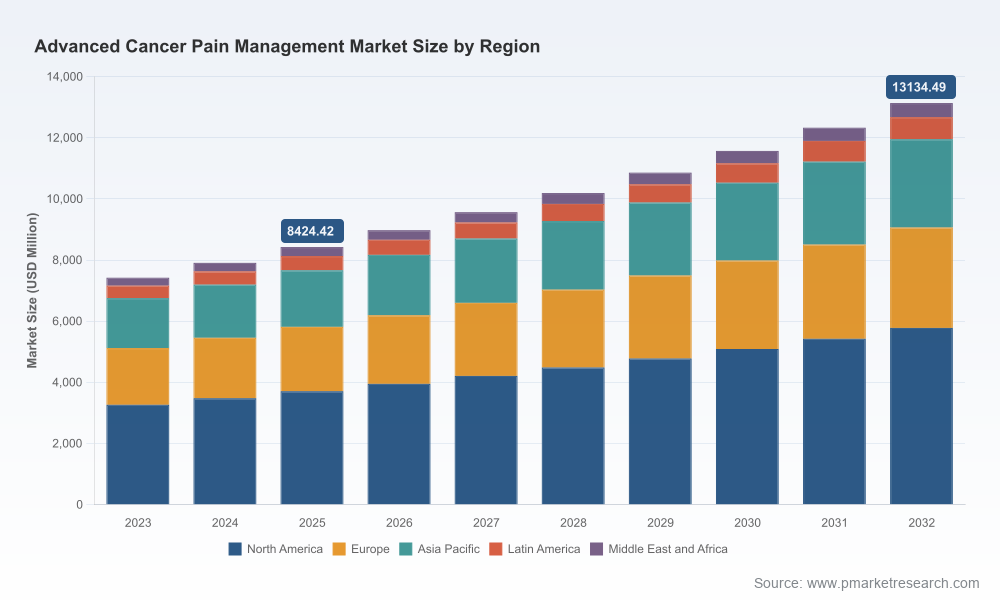

PW Consulting’s latest market research report — base year 2025, historical window 2020–2025, forecast 2026–2032 — synthesizes clinical innovation, regulatory shifts, reimbursement design, and competitive positioning to inform high-stakes corporate decisions in 2026. The global market for advanced cancer pain management has shown steady expansion from a 2023 base and reached approximately USD 8,424.42 Million in 2025. Under our central-case assumptions, the market grows at a compound annual growth rate (CAGR) of 6.55% through the forecast period, reaching roughly USD 13,134.49 Million by 2032. This brief highlights why the report is strategically relevant for life-sciences executives, investors, and health-system leaders considering product launches, portfolio reallocation, M&A, or market-entry strategies in 2026 — while deliberately withholding the full segment-level numerics to preserve the report’s role as the primary source for granular decision data.

Worldwide Advanced Cancer Pain Management Market

Timing: 2026 is a pivotal year when regulatory and reimbursement changes intersect with emerging non-opioid clinical data and maturing interventional technologies. Executives who align strategy to these inflection points can capture premium pricing, accelerate reimbursement acceptance, and shorten commercialization timelines.

Worldwide Advanced Cancer Pain Management Market

Risk mitigation: The market’s projected mid-single-digit CAGR masks important heterogeneity in modality, channel, and therapeutic approach. Our analysis provides scenario-based downside and upside cases that quantify clinical, regulatory, and policy risk to revenue streams — enabling stress-testing of investment theses before capital deployment.

Worldwide Advanced Cancer Pain Management Market

Competitive advantage: The report integrates a granular competitive-playbook and clinical-pipeline tracker that allows leadership teams to identify white-space opportunities where incumbents are under-invested, and where specialized entrants can establish durable footholds.

Between 2023 and 2025 the market demonstrated consistent expansion, reflecting a confluence of demographic demand, greater emphasis on supportive oncology care, and incremental product innovation. Our base-year analysis documents the market at about USD 8.42 billion in 2025, with a modeled increase to approximately USD 8.98 billion in 2026 under the baseline scenario. Looking further, the 6.55% CAGR we apply across 2026–2032 results in a near-term to medium-term trajectory that sees the market exceed USD 13.1 billion by 2032.

These macro figures are essential for portfolio-level sizing, but they do not substitute for the segment-level economics that determine profitability for specific therapies and technologies. That is precisely why PW Consulting’s full report pairs macro forecasts with adaptable financial models and scenario toggles — to translate aggregate growth into actionable revenue and margin expectations for individual product strategies.

Regulatory posture and opioid stewardship: Existing CDC guidance continues to differentiate policy toward cancer and palliative contexts, explicitly supporting appropriate opioid use for patients in active cancer care and end-of-life scenarios. Simultaneously, the DEA’s 2026 production quotas for major opioids have introduced supply-side discipline that can affect availability and pricing of controlled analgesics. Strategic implication: manufacturers and distributors should model supply constraint scenarios and prioritize continuity-of-care programs and alternative therapy pathways.

Reimbursement rewiring in favor of non-opioid options: CMS actions implemented under the NOPAIN Act (including separate Medicare payment for qualifying non-opioid treatments and electronic infusion pumps beginning January 1, 2026) materially change economic incentives for providers selecting between opioid-centric and non-opioid modalities. Companies with device-enabled, non-opioid solutions or combination therapy models can capitalize on this temporary reimbursement tailwind through focused value dossiers and payer pilots.

Accelerated non-opioid development: The FDA’s 2025 guidance to accelerate safe, effective non-opioid analgesics has catalyzed earlier-stage investment and earlier regulatory engagement. For firms investing in small molecules, biologics, or neuromodulation approaches, an aggressive evidentiary strategy is now warranted to secure expedited pathways and label differentiation.

Clinical innovation and interventional growth: Recent clinical developments — notably long-term data releases and trial expansions for interventional techniques — underscore a shifting therapy mix where precision nerve-targeted approaches and novel biologics are progressing from proof-of-concept to broader clinical evaluation. These modalities present opportunities to de-risk revenue concentration on traditional pharmacotherapies.

The sector exhibits moderate concentration: our CR3 and CR5 measures indicate that top-tier multinational players command meaningful share, but a sizeable portion of the market remains accessible to specialized entrants and innovative device- or biologic-focused companies. Incumbent pharmas continue to underpin the market through established opioid and supportive-care portfolios. Key archetypes observed in the competitive set include:

Global pharmaceuticals with broad analgesic franchises (examples include established multinationals): these players leverage scale, distribution, and lifecycle management to defend market share in traditional opioid and specialty pharmacotherapy segments.

Generic / high-volume manufacturers: they exert pricing pressure on commodity analgesics and create margin compression for branded products.

Device and interventional innovators: smaller, clinically-focused companies developing radiofrequency ablation technologies, targeted neuromodulation, and infusion-delivery platforms are proving clinical differentiation in targeted indications, particularly for visceral and neuropathic cancer pain.

Novel biologic and cannabinoid-based entrants: early clinical signals for non-traditional modalities indicate new therapeutic classes may emerge as adjuncts or alternatives to opioids in certain patient subsets.

For executives, the strategic tasks are clear: incumbent biologics and big-pharma should selectively invest in adjunctive non-opioid portfolios and device partnerships to hedge against policy and quota risks; specialty-device and biotech entrants should prioritize payer engagement and robust real-world evidence to accelerate adoption under revised reimbursement constructs; private equity and strategic buyers should use the market’s moderate concentration as a platform for bolt-on acquisitions to capture cross-modality synergies.

Interventional evidence maturation: long-term clinical data and trial expansions for transvascular radiofrequency ablation have broadened the potential addressable population beyond single-indication use. This material change increases the commercial upside for device-focused firms and investors willing to underwrite expanded pivotal programs.

Positive mid-stage signals for novel therapeutics: favorable Phase IIb data for investigational agents addressing chemotherapy-induced neuropathic pain validate non-opioid approaches and strengthen the case for expedited regulatory pathways and payer pilots.

Reimbursement shifts favoring devices and non-opioid profiles: the inclusion of electronic infusion pumps in separate Medicare payment schedules and the temporal payment provisions under recent legislation create commercialization windows that should be exploited with targeted value-based contracting and early adopter site engagement.

Actionable revenue forecast models (interactive Excel) aligned to base-year 2025 inputs and scenario toggles across clinical success, regulatory timelines, and reimbursement outcomes.

Segment-level demand curves, patient-flow assumptions, and channel economics that translate aggregate growth into product-level P&L impacts (note: detailed segment tables are included in the full report and are intentionally not reproduced here).

Competitive matrices mapping capability gaps, pipeline timelines, and potential M&A targets — annotated with likely integration synergies and post-acquisition value capture levers.

Reimbursement playbooks and payer engagement templates that reflect the latest CMS policy changes and include negotiation-ready value propositions for Medicare and major commercial plans.

Regulatory risk register and mitigation strategies tied to opioid stewardship policies and DEA quota volatility, including contingency plans for supply disruptions and alternative sourcing.

Market-entry and commercialization blueprints for devices, biologics, and combination products — including clinical development roadmaps, KOL engagement plans, and hospital/procurement contracting tactics.

Prioritize quick-win reimbursement captures by launching payer pilots in jurisdictions where non-opioid and device reimbursement changes reduce adoption barriers.

Redeploy R&D capital into modalities with clear regulatory acceleration pathways and early positive clinical signals; defer marginal investments in high-risk, low-differentiation commodity analgesics.

Target M&A: identify bolt-on assets that strengthen multi-modal portfolios (pharma + device + digital pain-management services) and that can be integrated to capture cross-selling with oncology franchises.

Build supply-resilience strategies to mitigate the impact of controlled-substance production quotas, including secured manufacturing agreements, alternative formulations, and patient-access programs.

PW Consulting’s Worldwide Advanced Cancer Pain Management Market report equips decision-makers with the macro context and the transaction-grade tools needed to make defensible, value-maximizing choices in 2026. The market’s steady growth trajectory (CAGR 6.55% through 2032) and recent policy and clinical inflections create both opportunity and risk — and the differential management of those forces will determine market winners. For executives preparing board-ready investment cases, for investors evaluating platforms and tuck-ins, and for commercial teams building reimbursement strategies, the full report provides the granular datasets and playbooks you will need. Visit the report landing page to access the dataset, download the evidence appendices, and arrange a bespoke briefing with PW Consulting’s senior analysts.

For detailed analysis of this topic, please visit the official page:Worldwide Advanced Cancer Pain Management Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com