Voice and Speech Recognition Market Top Industry Shareholders and CAGR Outlook to 2033

Other |

2026-02-12 08:13:33

PW Consulting’s newest market research release offers senior executives, defence procurement officers, and strategic investors a concise but deep preview of the Worldwide Anti‑Tank Missile System Market as they enter 2026. Built on a 2025 base year and a historical series covering 2020–2025, the study projects the market through 2032. Our high‑level forecast indicates market expansion from an estimated global size of approximately USD 7,200 Million in 2025 to just over USD 10,268 Million by 2032, reflecting a compound annual growth rate (CAGR) of about 5.2% across the 2026–2032 forecast window.

Worldwide Anti-Tank Missile System Market

Actionable intelligence amid heightened procurement cycles: Governments and prime contractors are executing multi‑year buys and capacity investments to address near‑term armored threats — our analysis identifies the inflection points and lead‑times that will shape 2026 contracting windows.

Worldwide Anti-Tank Missile System Market

Investment prioritisation for limited budgets: With moderate but sustained market growth, resource allocation between R&D, production scale‑up, and export support will determine winners; the report clarifies where marginal dollars generate the largest strategic return.

Worldwide Anti-Tank Missile System Market

Supply‑chain stress testing and mitigation: Raw‑material constraints and supplier concentration have moved from theoretical risks to operational constraints. We supply the decision frameworks needed to harden sourcing strategies and de‑risk production ramp‑ups.

Executive summary and decision memo: Two‑page briefings tailored for CEOs, procurement chiefs, and investment committees that translate market dynamics into immediate decisions for 2026.

Market sizing & forecast models: Annual historical series (2020–2025) and a transparent, scenario‑based forecasting engine for 2026–2032, enabling bespoke sensitivity testing against price, procurement cadence, and geopolitical scenarios.

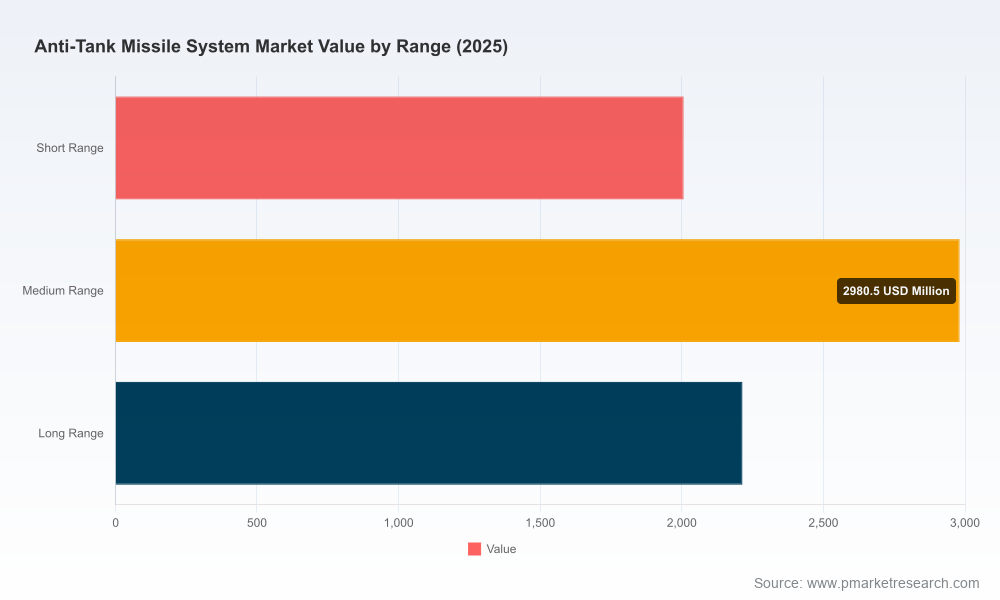

Segmentation frameworks: Rigorous breakouts by region, system type (man‑portable, vehicle‑mounted, air‑launched), and operational range (short, medium, long) with qualitative drivers and practical use cases. Note: this preview intentionally omits tabulated subsegment values — the complete tables and downloadable datasets are provided in the full report.

Supply‑chain & raw‑materials playbook: Assessment of critical inputs (high‑temperature alloys, rare‑earth magnets, specialty composites), supplier concentration risks, and actionable sourcing recommendations including hedging, stock‑pile triggers, and near‑shoring levers.

Competitor and capability maps: Comparative profiles of global primes, established regional manufacturers, and new entrants — including platform strengths, industrial base footprints, and likely moves in 2026–2028.

Procurement & industrial cooperation scenarios: Templates for multi‑year contracts, joint‑venture structures, local production offsets, and buy‑to‑print strategies designed to accelerate award to sustained production.

M&A and partnership heatmap: Tactical guidance on target archetypes (technology owners, niche subsystems, test facilities) that would be accretive in 2026 market conditions and beyond.

Appendices & data annex: Methodology, primary interviews, and the underlying time‑series datasets in machine‑readable format (available in the full purchase).

Geopolitical realignments and force modernisation: Heightened NATO commitments and regional defence initiatives have sustained demand for both procurement and in‑theatre replenishment. These drivers are less volatile than short‑term spikes and push programmes toward predictable, multi‑year contracting structures.

Operational doctrine evolution: The persistence of armoured threats in hybrid conflicts has reinforced demand for fire‑and‑forget and top‑attack capabilities, while urban and distributed operations increase emphasis on man‑portable and precision‑guided variants tailored to asymmetric engagements.

Industrial scale & capacity investments: Prime contractors and joint ventures are expanding production footprints to meet allied demand. These capacity investments bring near‑term supplier bottlenecks — particularly in propulsion and guidance subsystems — which will favour firms with secured supplier networks and automation‑led productivity gains.

Critical‑material exposure: Components for guidance and propulsion rely on specific alloys, rare‑earth materials, and advanced composites. Our risk matrix shows materials supply is a primary near‑term tension point that can materially affect lead times and unit economics if left unmitigated.

Regulatory and export dynamics: Export approvals, offset obligations, and local content requirements are becoming decisive elements of procurement outcomes. Suppliers who can offer credible industrial participation packages will substantially improve award probability in 2026 competitions.

The global competitive set combines long‑established western primes, agile regional manufacturers, and state‑backed enterprises. Market concentration is meaningful: the top three suppliers capture a substantial majority of reported industry revenue, and the top five extend that share further — a structure that rewards incumbency, scale, and integrated aftermarket capabilities.

Primes with integrated solutions: Industry leaders that pair missile airframes with advanced guidance and production scale retain preferential access to major procurement programmes and export frameworks. Joint ventures and production partnerships are a recurring theme as primes accelerate output.

Regional champions and niche innovators: A cohort of specialized suppliers and regional manufacturers supply competitive, lower‑cost alternatives and enable localised industrial participation, particularly in emerging procurement markets.

System integrators and platform partners: Vehicle and avionics integrators play a pivotal role in taking weapons from catalogue to fielded capability; their role in production and sustainment contracts increasingly influences procurement decisions.

Key illustrative players profiled in the full study include major western primes with joint‑venture production footprints, European missile consortia, Israeli electro‑optics and missile manufacturers, Turkish and South African systems with export momentum, and national champions in Asia and Russia. Each profile contains capability matrices, supplier networks, recent developments, and an “what to watch” timeline for 2026–2028.

Procurement continuity: Several major procurement and production programmes moved from one‑off buys to serial production in late 2025 and early 2026, signalling longer‑term demand stability and raising the value of production capacity commitments.

Export flows and capability alignment: Western deliveries for NATO alignment and regional support packages illustrate the premium placed on interoperability and supply assurance; firms offering training, spares, and integration services gained negotiation leverage in recent awards.

Production scale and supplier coordination: Prime contractors have publicly expanded supplier coordination efforts and automation investments to meet allied demand — a clear signal that suppliers capable of high‑quality, high‑volume output will be preferred partners in 2026 contracting rounds.

For primes: Prioritise supplier‑led acceleration programs (propulsion motors, seekers) and codify multi‑tiered capacity agreements to reduce single‑source exposure. Convert export support into long‑term service contracts to stabilise margins.

For subsystem suppliers: Focus on modular, drop‑in upgrades that address guidance, lethality, and cost‑to‑produce. Build certification pathways with multiple primes to diversify demand.

For governments/procurement agencies: Design procurement vehicles that balance near‑term replenishment speed with long‑term industrial benefits. Use phased awards and pre‑qualified supplier pools to accelerate deliveries while preserving competition.

For investors: Look for companies with demonstrable order books, verified supplier ecosystems, and technical IP in guidance and seeker subsystems. Asset plays in test facilities and production automation providers are attractive adjacencies.

Our topline figures and forecasts arise from a multi‑method approach: triangulation of public filings, defence procurement notices, supplier interviews, in‑market primary research, and a proprietary scenario model calibrated across historical outcomes. The base year is 2025 and the forecast window spans 2026–2032; sensitivity testing and upside/downside scenarios are provided in the full dataset so clients can model bespoke procurement or disruption cases.

This preview is designed to surface the strategic choices, systemic risks, and opportunity areas executives must evaluate in 2026. PW Consulting’s full Worldwide Anti‑Tank Missile System Market report contains the complete segmentation tables, downloadable time‑series data, vendor scorecards, and a suite of decision tools developed for rapid executive action. Organisations seeking to validate procurement timelines, prioritise supply‑chain investments, or evaluate potential acquisition targets for 2026 should consult the full report and data annex.

To access the comprehensive datasets, subsegment breakdowns, and vendor scorecards referenced in this preview, please refer to the PW Consulting report page for full purchase and licensing options.

For detailed analysis of this topic, please visit the official page:Worldwide Anti-Tank Missile System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com