PW Consulting: Oral Mucositis Drugs Market to Reach USD 263.11M by 2032 (7.38% CAGR)

Other |

2026-07-08 08:47:41

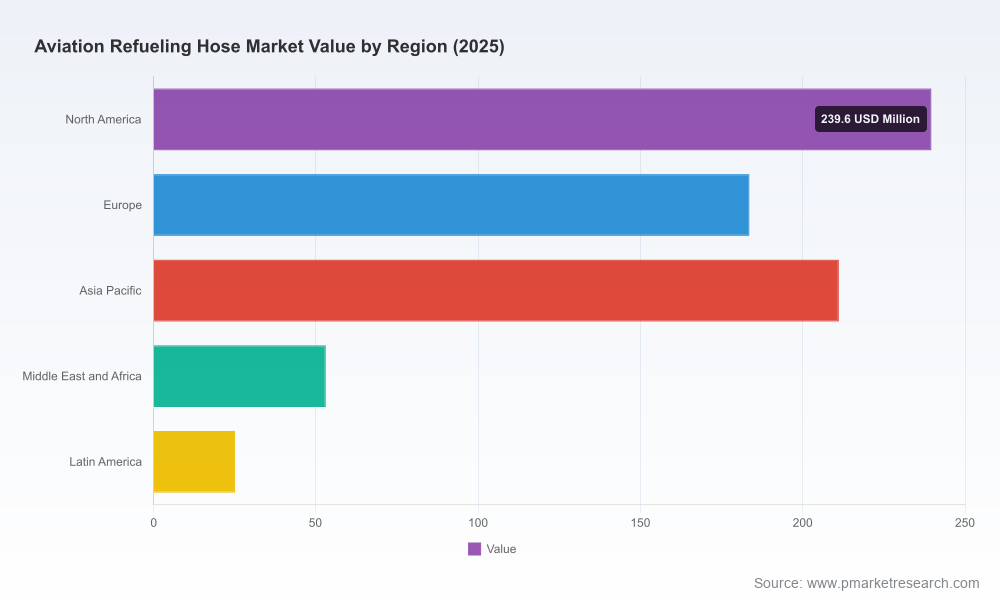

PW Consulting today publishes an executive briefing accompanying our forthcoming Worldwide Aviation Refueling Hose Market report. The study synthesizes five years of historical data (2020–2025) and delivers a granular forecast (2026–2032) built for executive action. At the macro level, the market base year (2025) measures approximately USD 712.5 Million and the model anticipates a steady compound annual growth rate (CAGR) of 5.22% through the forecast period, lifting the market into the approximately USD 1.0+ Billion range by 2032. These headline metrics capture a category that has rebounded from pandemic disruption and is now being reshaped by fleet renewals, defense recapitalization, and the gradual adoption of sustainable aviation fuels (SAF).

Worldwide Aviation Refueling Hose Market

Translate macro momentum into procurement and R&D priorities: With mid-single-digit CAGR and predictable year‑on‑year expansion, procurement teams must convert demand visibility into strategic sourcing and inventory actions to avoid shorts in critical elastomers and reinforcement materials.

Worldwide Aviation Refueling Hose Market

De‑risk supply chains before costs compound: The report identifies material and component pinch points that can create outsized operational exposure—especially for firms reliant on specific polymers, textile cord, or specialty couplings produced in concentrated geographies.

Worldwide Aviation Refueling Hose Market

Position for SAF compatibility: As SAF adoption scales, OEMs and tier‑1 suppliers will require validated hose systems that maintain electrical continuity, pressure integrity and chemical resistance across new fuel blends; 2026 is the pivot year to fund targeted material qualification programs.

Prioritize certification throughput: Regulatory compliance (EI 1529, ISO 1825, API 1529, NFPA 407 and related national standards) and 100% hydrostatic and electrical testing are non‑negotiable—capacity for testing and traceable serialisation is a near‑term competitive advantage.

Transparent forecasting model with scenario variants (base, accelerated SAF adoption, defence‑led surge) and sensitivities mapped to raw material and fuel‑type shifts.

Procurement playbook for 2026: supplier scorecards, minimum viable qualification checklists, lead‑time mapping and suggested contractual clauses for supply continuity and material change control.

Regulatory compliance toolkit: consolidated requirement matrices across global standards, recommended inspection regimes (including hydrostatic and electrical continuity protocols), and sample test certification templates.

Supply‑chain risk heatmap and mitigation playbook: north‑to‑south supplier diversification options, near‑term mitigation levers (safety stock, forward buys), and long‑term strategies (localisation, strategic partnerships).

Commercial and aftermarket growth strategies: win themes for OEMs, MRO service bundling recommendations, and pricing strategies to capture value across new fuelling paradigms.

Competitive intelligence and M&A radar: vendor scorecards (capability, certification status, manufacturing footprint), and a short‑list of bolt‑on targets and partnership candidates aligned to materials, testing and geographic coverage.

The market shows moderate concentration, with the three largest suppliers together accounting for a substantial share of available demand and the top five expanding that footprint further (CR3 ≈ 42.5%; CR5 ≈ 58.8%). Several legacy manufacturers and specialist houses combine global scale with differentiated capability sets—understanding their strengths and gaps is essential for 2026 vendor strategies.

Hewitt (Husky Corporation) — A leading US‑based provider of aviation fueling hoses, notable for qualified jet‑fuel‑grade constructions, permanent coupling options and full hydrostatic certification processes. Their product breadth across diameters and applications positions them as a default partner for many commercial and private refuelling programmes.

Continental (ContiTech) — European engineering heritage and standards compliance (EI/ISO/NFPA) underpin Continental’s lightweight and durable hose platforms. Their product focus on both fueling and defueling use cases and hydrant service makes them a strong counterparty for airports and ground‑service operators.

Parker Hannifin (Parker Industrial Hose) — Offers branded lines (Gold Label, Jetcord C) that emphasize standardized certification and global serviceability; their channel reach into industrial fleets supports aftermarket penetration.

Icon Aerospace — UK‑based specialist focused on bespoke in‑flight refuelling hoses for defence applications; their lightweight designs for varying pressure and altitude conditions address a technically demanding segment where performance requirements drive premium pricing.

Eaton (Aeroquip) — Integrates hose assembly capability with broader fluid systems expertise, appealing to integrators who seek end‑to‑end fluid transfer solutions with aerospace traceability standards.

Additional players — Carter (Durodyne unit), Aero‑Hose Corp., Elaflex HIBY, and regional manufacturers in Asia provide competitive breadth. These firms often compete on certification speed, customization, and local service presence—factors that matter to airports and national defence programmes.

Recent sector activity highlights the strategic realignments currently underway: Trelleborg’s acquisition activity in high‑performance materials (2025) and Metrea’s force structure contracts and fleet acquisitions (2024–2025) underline increased defence‑driven demand and vertical consolidation in material supply chains. Exhibitions and product launches continue to spotlight coupling innovations and testing equipment as companies race to reduce total cost of ownership and raise safety margins.

Raw materials exposure: Nitrile‑based elastomers, textile reinforcement systems and steel/composite strengths drive both cost and technical performance. Fluctuations in polymer feedstocks and steel supply chains can compress margins quickly.

Standards and qualification intensity: Aviation hoses require 100% hydrostatic testing, electrical continuity verification and traceable serialisation. This testing overhead is a gating factor for new entrants and a competitive moat for established manufacturers.

Fuel chemistry shift: The roll‑out of SAF and blended fuels is driving new chemical compatibility testing and material change control; firms that pre‑qualify hoses for multi‑fuel use will gain early commercial advantages.

Geopolitical and trade considerations: Presence of capable manufacturers in Asia, Europe and North America creates both diversification opportunities and exposure to trade policy risk—buyers should model tariffs and transport lead times when sizing programmes for 2026 deployment.

Lock forward volumes for critical elastomers: Negotiate conditional forward purchase agreements with suppliers of nitrile and specialty polymers to stabilise input costs and ensure continuity of supply during fleet ramp phases.

Dual‑certify materials for SAF compatibility: Fund accelerated qualification of hose linings and covers against anticipated SAF blends; aim to complete testing cycles and obtain updated certificates before 2027 market inflection points.

Invest in localised testing capacity: Add hydrostatic and electrical continuity testing capacity in key regions or partner with accredited labs to reduce lead times for commissioning and service turnarounds.

Targeted M&A and partnerships: Pursue bolt‑on acquisitions that add composite reinforcements, permanent coupling technology, or certified assembly capacity—these assets shorten time‑to‑market for integrated hose systems.

Monetise aftermarket services: Build service contracts that bundle preventative inspection, recertification and rapid‑change hose assemblies; this creates recurring revenue and reduces buyers’ operational risk.

For executives preparing 2026 budgets, supplier RFQs, and new product roadmaps, the PW Consulting market analysis provides a decision‑grade view of demand trajectories (base market midpoint and upside scenarios), supplier positioning, and actionable mitigation templates for materials and testing risks. The full report contains the detailed segmentation, vendor scorecards, and downloadable modelling tools needed to execute the tactical moves above—information we are deliberately preserving within the full publication to ensure clients obtain the complete decision support package.

To obtain the comprehensive dataset, vendor benchmarks and the scenario model that underpins our USD‑denominated forecast, visit the PW Consulting report page and request the Worldwide Aviation Refueling Hose Market report. The granular segmentation and downloadable strategy playbooks will equip procurement, engineering and corporate development teams for a decisive 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Aviation Refueling Hose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com