Worldwide Photobiostimulation Devices Market — 2026 Strategic Briefing

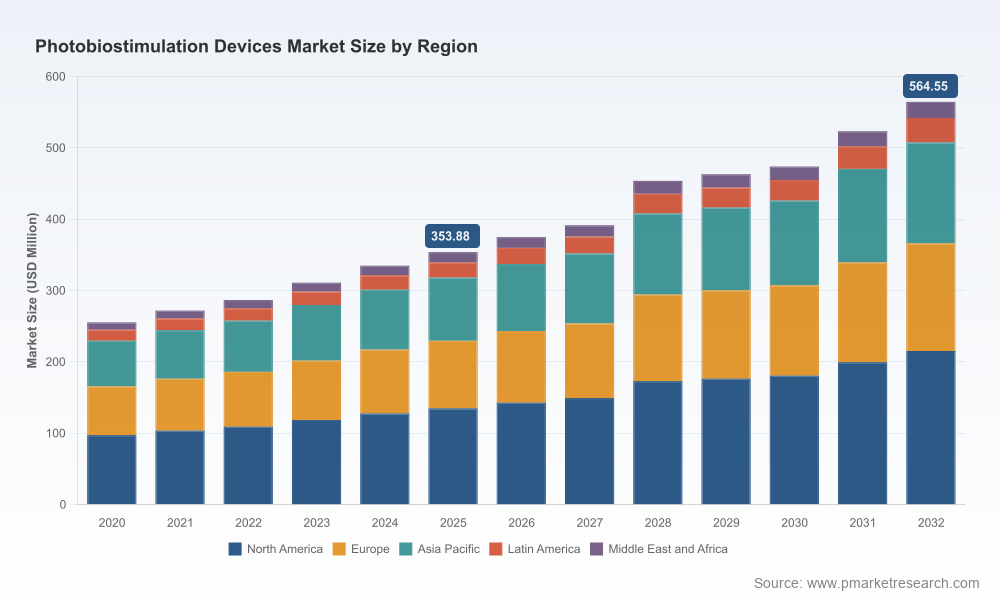

PW Consulting today publishes a targeted industry briefing derived from our comprehensive Worldwide Photobiostimulation Devices Market report (base year 2025). The analysis documents a market that has matured rapidly over the past half‑decade and is positioned for sustained growth: total market value rose from approximately USD 255 million in 2020 to roughly USD 354 million in 2025, with forecasts pointing to continued expansion through 2032 and a compound annual growth rate (CAGR) of 6.9% over the 2026–2032 forecast period. For executives planning capital allocation, R&D pipelines, or M&A activity in 2026, this briefing highlights the strategic inflection points that will determine winners and losers — while preserving the granular segmentation data that remains available only in the full report.

Worldwide Photobiostimulation Devices Market

Why 2026 Is a Strategic Inflection Year

Several concurrent dynamics are compressing decision cycles and elevating the stakes for market entrants and incumbents alike. Regulatory clarification and landmark authorizations have reduced uncertainty for certain clinical indications; reimbursement coding for retinal photobiomodulation is beginning to form; clinical evidence packages are advancing beyond small-scale studies toward regulatory-grade trials; and participating firms are demonstrating increased appetite for consolidation and platform expansion.

Worldwide Photobiostimulation Devices Market

- Regulatory momentum: The FDA’s draft guidance on photobiomodulation devices (January 2023) has crystallized expectations for non‑clinical testing, clinical study design, and labeling. A recent de novo authorization for an ophthalmic PBM device has further validated pathway options beyond the traditional adjunctive 510(k) route.

- Reimbursement signals: The creation of a category III CPT code for retinal PBM sessions (effective January 1, 2025) and early Medicare payment estimates are beginning to establish a billing precedent — a prerequisite for durable clinical adoption in many care settings.

- Commercial validation: Strategic transactions and device clearances over the last 18 months demonstrate industry confidence in select indications and technologies, catalyzing capital inflows and partnership activity.

What the Full Report Delivers (Practical, Transaction‑Ready Content)

PW Consulting’s full market study is built for corporate strategy teams, investors, and product leaders who need executable insights in 2026. The report combines market intelligence with practical deliverables:

Worldwide Photobiostimulation Devices Market

- Top‑down and bottom‑up market sizing with a transparent methodology covering historical (2020–2025) and forecast (2026–2032) horizons.

- Scenario financial models that stress‑test revenue outcomes under alternative adoption, reimbursement, and pricing assumptions.

- Regulatory playbooks tailored to 510(k) and de novo pathways, including recommended non‑clinical packages and clinical study endpoints for high‑value indications.

- Reimbursement engagement templates and value dossiers calibrated to US CPT, Medicare dynamics, and selected international payor ecosystems.

- Commercial go‑to‑market frameworks for clinic, hospital, veterinary, and direct‑to‑consumer channels.

- Vendor due‑diligence dossiers and an M&A playbook that identify capability gaps, integration risk factors, and expected consolidation vectors.

To preserve the strategic purpose of this release as a sectional preview, we intentionally withhold the report’s detailed splits by region, product, and application here; those data are included in the full document and the supporting Excel models.

Competitive Landscape — Who Matters and Why

The commercial ecosystem is populated by a mix of clinical specialists, consumer‑oriented innovators, and a growing number of platform players. Market concentration is moderate: the top three firms account for roughly 38% of market revenue and the top five for about 52%, leaving meaningful space for differentiated entrants and vertical consolidators.

- THOR Photomedicine (UK) — A clinically focused device developer with CE and FDA‑cleared systems for multiple pain and mucositis indications. THOR’s combination of regulatory certifications and clinical partnerships positions it as a trusted supplier to healthcare providers seeking evidence‑backed adjunctive therapies.

- Erchonia Corporation (US) — A leader in low‑level laser therapy with an extensive portfolio of FDA clearances across pain, fat removal, and other indications. Erchonia’s breadth of clearances exemplifies the pathway of building a cumulative regulatory moat.

- Vielight (Canada) — A prominent player in at‑home, LED‑based brain stimulation and wellness devices. Vielight highlights the consumer/treatment hybrid opportunity in long‑term care and wellness markets.

- LightForce & LumaCare (US) — Focused on deep‑tissue and portable clinical lasers, respectively, these firms demonstrate the therapeutic demand for higher‑power, clinic‑grade devices for musculoskeletal care.

- Microlight, Avant, ARRC LED, LightMD, TheraLight, NovoTHOR and others — These firms represent specialization across modality (laser vs. LED), treatment scope (local vs. full‑body), and channels (clinic, home, veterinary). Each approach maps to distinct go‑to‑market and evidence requirements.

- LumiThera / Alcon — The LumiThera Valeda de novo authorization for dry age‑related macular degeneration and Alcon’s announced acquisition intent are the most notable strategic signals of late: they illustrate how legacy ophthalmic primes may absorb PBM capabilities to accelerate commercialization into specialty care.

Regulatory & Reimbursement Imperatives

In 2026, regulatory and reimbursement strategy is no longer an afterthought; it is a primary product design and commercialization consideration.

- Regulatory teams must align preclinical dosimetry, bench penetration profiling, and clinical endpoint selection with FDA expectations articulated in recent guidance documents. For novel ophthalmic and vision applications, the de novo route has proven viable but requires rigorous functional endpoints and patient‑reported outcomes.

- Reimbursement teams should prioritize engagement with specialty societies and payors to translate new CPT coding into repeatable payment pathways. Early evidence suggests session‑level reimbursement can be meaningful for clinic economics; however, allowed amounts and coverage policy remain variable and require active stakeholder management.

- Quality and manufacturing certifications (e.g., ISO 13485) are table stakes for global commercial rollouts and for enabling institutional purchasing agreements.

Technology and Clinical Trends Shaping Product Strategy

Successful 2026 product strategies will reconcile clinical efficacy with usability, dosing reproducibility, and data capture:

- Modalities: Laser‑based systems continue to lead certain therapeutic niches that demand tissue penetration and focused dosing, while LED platforms are expanding home and wellness applications due to cost and safety profiles.

- Form factors: The market bifurcates between clinic‑grade platforms (including class IV deep‑tissue lasers and full‑body beds) and portable/at‑home devices. Each channel requires differentiated regulatory, clinical, and commercial playbooks.

- Data & software: Integration of treatment logging, patient adherence tracking, and remote monitoring enhances clinical evidence generation and payor value propositions. Companies investing early in digital therapeutics adjacencies will be better positioned to demonstrate outcomes at scale.

Actionable Recommendations for 2026 Decision‑Makers

Leaders preparing budgets, product roadmaps, or transactional strategies this year should prioritize the following:

- Lock in regulatory strategy before finalizing product architecture. Early alignment with regulators reduces rework risk and accelerates time‑to‑market.

- Invest in at least one randomized, well‑powered clinical study aligned to payer endpoints for any indication targeted for broad clinical adoption.

- Pursue partnerships with channel incumbents (clinical networks, specialty practices, veterinary groups) to accelerate real‑world evidence collection and adoption.

- Develop a two‑track commercialization plan that separates clinic/hospital commercialization from direct‑to‑consumer strategies, with distinct pricing and support models.

- Use M&A and licensing selectively to acquire capabilities (clinical trial infrastructure, distribution, IP) rather than incremental portfolios that increase integration risk.

- Prioritize manufacturing scale and quality certifications early if global roll‑out is anticipated; lead times for medical‑grade components and ISO processes can be a gating factor.

How This Report Helps You Move in 2026

PW Consulting’s full market study is designed as a decision‑grade tool. Subscribers receive not only the narrative and slide summary but also the underlying financial models, evidence matrices, regulatory checklists, and competitor dossiers necessary to support board‑level decisions, investor due diligence, and business‑unit planning. The report converts market commentary into transaction and execution playbooks — from valuation scenarios for M&A to step‑by‑step clinical trial designs that align with FDA expectations.

If your team must decide on R&D prioritization, partnership targets, pricing strategy, or M&A prospects in 2026, this briefing is the compact view. For the full suite of data — including detailed segmentation by region, product, and application; vendor‑level revenue splits; and the executable Excel models that underpin our forecasts — please refer to the PW Consulting report distribution channels or contact our commercial team for access.

Next Steps

PW Consulting is offering tailored briefings and workshop engagements for executive teams seeking to convert these insights into one‑year and three‑year roadmaps. To arrange a briefing or request the full report and its accompanying models, please contact PW Consulting’s market research desk via our website or corporate sales channels.

For detailed analysis of this topic, please visit the official page:Worldwide Photobiostimulation Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com