Worldwide Coated Fabrics for Defense Market — Strategic Outlook for 2026 Decision‑Makers

PW Consulting’s latest market study on Worldwide Coated Fabrics for Defense frames the competitive and strategic battleground for manufacturers, prime contractors, and procurement agencies as they plan for 2026 and beyond. The global market — estimated at approximately USD 730 Million in 2025 — is forecast to expand at a compound annual growth rate (CAGR) of roughly 6.2% through the 2026–2032 forecast horizon, reaching just over USD 1.1 Billion by the end of the period. This briefing highlights the report’s practical value for executive decision‑making while deliberately withholding the full segmented datapack to encourage use of the source report for transaction‑critical details.

Worldwide Coated Fabrics for Defense Market

What senior leaders need to know — top takeaways

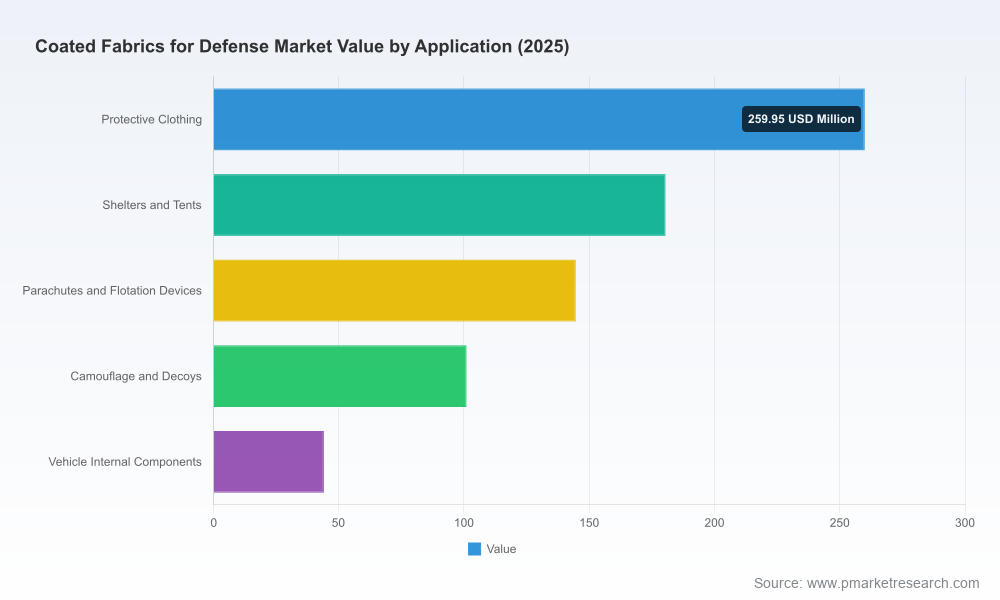

- Demand for multifunctional coated textiles (lightweight ballistic overlays, flame‑resistant shelters, and high‑durability protective garments) is rising in parallel with defense modernization programs and geopolitical risk.

- Supply‑side economics remain sensitive to petrochemical price volatility and resin availability; procurement strategies that ignore raw material exposure risk margin compression.

- The competitive landscape is moderately fragmented: the market’s top three and five suppliers capture meaningful—but not dominant—shares, leaving room for niche specialists and well‑executed consolidation.

- Compliance with military standards (MIL‑SPEC), domestic procurement rules (e.g., Berry Amendment considerations), and certification pathways are decisive gating factors for contract award and market access.

Why this report matters for 2026 corporate strategy

Defense buyers and OEMs face compressed procurement timelines and heightened performance requirements. Coated fabrics are no longer a commodity layer; they are engineered systems that must simultaneously deliver protection, durability, weight savings, and integration with other subsystems (ballistics, CBRN protection, wearable electronics). For 2026 planning cycles, executives need a defensible view of near‑term demand drivers, supplier risk profiles, and the investment priorities that will determine competitive positioning over the next three to five years.

Worldwide Coated Fabrics for Defense Market

Our study synthesizes macro market sizing and trajectory with tactical intelligence — i.e., where bids are likely to appear, which specifications drive premium pricing, and what capabilities primes expect from their suppliers. Rather than a static snapshot, the report maps the intersection of procurement pipelines, material science trends, and cost dynamics so management teams can prioritize R&D, capacity expansion, or strategic partnerships with clarity.

Worldwide Coated Fabrics for Defense Market

Practical, action‑oriented contents of the report

- Robust market sizing and forward projections (base year 2025) and scenario runs that stress test demand under alternate geopolitical and supply‑shock conditions.

- Supplier benchmarking and capability matrices covering polymer‑coated, rubber‑coated, and film‑backed constructions, plus assessments of certification readiness (MIL‑SPEC, Berry compliance, other national standards).

- Procurement intelligence: line‑of‑sight to upcoming program solicitations, likely spec changes, and prime contractor sourcing preferences that influence supplier selection.

- Cost‑to‑serve and raw‑material sensitivity models that quantify margin impacts from petrochemical price swings and provide hedging and sourcing playbooks.

- M&A and partnership playbooks highlighting where consolidation, vertical integration, or JV structures can unlock scale or proprietary material advantages.

- Technology roadmaps: fibre/film innovations, multi‑ply constructions, and finishing techniques that materially affect function and lifecycle costs.

- Operational readiness checklists for factory qualification, quality management (ISO/MIL), and export compliance to accelerate time‑to‑contract.

Competitive landscape: key players and strategic implications

The market comprises specialist material houses, large diversified technical textiles firms, and regional players focused on defence applications. The three‑firm and five‑firm concentration ratios indicate a market where the largest suppliers hold important shares but do not preclude new or mid‑tier entrants from carving profitable niches.

- The Rubber Company (UK) — A strong player in rubber‑coated and high‑strength fibre constructions; its expertise in non‑metallic armour and high‑performance fibres positions it well to win advanced protection contracts where bespoke laminates are required.

- Worthen Industries (US) — A producer of synthetic rubber and vinyl‑coated textiles with broad applicability in protective garments and industrial defence uses; its product breadth supports rapid response to tactical procurement needs.

- Tex Tech Industries (US) — A solutions‑led provider with a deep ISO certification portfolio and a high mix of tailored aerospace and military offerings; attractive to primes seeking low‑risk suppliers for demanding specs.

- Trelleborg AB (Sweden) — Engineered coated fabrics with differentiated product lines (e.g., high abrasion, flame resistance); appeals to institutional buyers prioritizing lifecycle performance.

- Colmant, Milliken, Seaman, Chemprene, CTT Group, HLC Industries — Collectively, these firms represent a mix of high technical capability, regional supply strengths, and niche product portfolios (shelters, vehicle interiors, camouflage, weight‑critical textiles).

Strategically, incumbents with proprietary fibre treatments, vertically integrated finishing, or scale in core resin supply enjoy advantages in margin resilience. Conversely, niche specialists that dominate specific technical niches (e.g., lightweight multi‑ply laminates or shelter membranes) remain attractive targets for primes seeking capability depth without bearing R&D burden.

Supply chain, procurement and regulatory dynamics

Three interlinked dynamics determine the operational playbook in 2026:

- Raw‑material volatility: Dependence on petrochemical feedstocks (PVC, polyurethane) creates price and availability risk. Procurement teams must model material exposure and pursue dual sourcing, strategic forward purchasing, or resin substitution where feasible.

- Standards and certifications: MIL‑SPEC compliance and domestic sourcing rules are non‑negotiable for many defence contracts. Suppliers that cannot demonstrate certification and traceability will be excluded irrespective of price.

- Geopolitical demand shocks: Rising defence budgets in certain theatres create surges in demand for lighter, more durable coated fabrics. Suppliers with agile capacity or geographic proximity to programmes can capture premium win rates.

For procurement leaders, the implication is clear: negotiate contracts that include raw‑material escalation clauses, hold strategic safety stock for critical resin inputs, and prioritize suppliers with demonstrated compliance and rapid qualification pathways.

Scenario planning: three plausible 2026 futures and recommended responses

- Base case (moderate growth): Demand expands steadily in line with the underlying market CAGR. Actions: invest in incremental capacity, accelerate product certifications, and optimize cost‑to‑serve for core product lines.

- Acceleration case (procurement surge): Renewed procurement due to regional escalations pushes demand well above baseline. Actions: immediate capacity scaling via contract manufacturing partnerships, fast‑track qualification for alternative suppliers, and prioritization of higher‑margin technical offerings.

- Supply shock case (petrochemical disruption): Raw‑material shortages or price spikes compress margins and delay deliveries. Actions: activate procurement hedges, qualify resin substitutes and alternate chemistries, and restructure contracts with escalation mechanisms to preserve cash flow.

How to use this research in boardroom decision‑making

Executives should treat this report as both a market map and an execution guide. Practical uses include:

- Aligning R&D pipelines to the product attributes that buyers will pay a premium for in 2026 (weight, multifunctionality, certification speed).

- Prioritizing capital allocation: where to expand capacity, where to partner, and where to pursue acquisitive growth.

- Informing procurement negotiations with quantified exposure scenarios and suggested contract clauses tied to material indices.

- Preparing commercialization roadmaps that integrate certification timelines into go‑to‑market plans so bids meet procurement windows.

Recent industry signals that validate the forecast

- The 2026 Joint Advanced Planning Brief for Industry (JAPBI) by DLA Troop Support reaffirmed longer‑term textile and clothing requirements, signaling procurement opportunities for certified coated fabric suppliers.

- Strategic positioning by firms such as CTT Group in 2025 underscores supplier efforts to accelerate advanced textile, polymer, and composite capabilities for protection and camouflage—consistent with demand for higher‑value, integrated solutions.

Next steps and how PW Consulting can help

For organizations planning 2026 investments, the report is configured as an actionable playbook: it pairs market trajectories (base year 2025, CAGR through 2032) with supplier intelligence, cost models, and certification timelines. To access the full segmented datasets, procurement‑grade forecasts, and vendor scorecards that support contract negotiations and M&A diligence, please consult the full PW Consulting report. Our advisory teams are available to run tailored scenario analyses, supplier due diligence, or transaction support based on the report’s datasets.

In an environment where materials science, procurement policy, and geopolitics converge to reshape defence textiles, leaders who pair disciplined scenario planning with operational readiness will capture disproportionate share and margin. PW Consulting’s research provides the evidence base and tools to make those 2026 choices with confidence.

For detailed analysis of this topic, please visit the official page:Worldwide Coated Fabrics for Defense Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com