Independent Escort In Sharjah +971563559726

Other |

2026-07-01 12:51:07

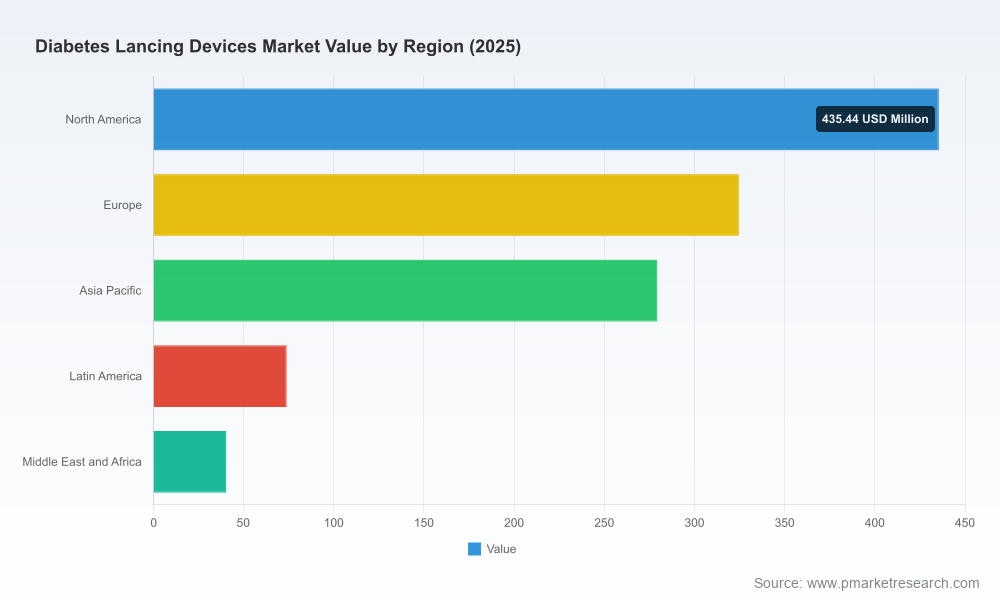

PW Consulting’s latest market intelligence on Worldwide Diabetes Lancing Devices frames 2026 as a pivotal year for executives, investors and product leaders seeking to convert steady market growth into sustainable advantage. The global market for lancing devices has expanded from approximately USD 820 million in 2020 to about USD 1,153 million in 2025, and our forward-looking modeling anticipates growth to near USD 1,870 million by 2032, representing a compound annual growth rate (CAGR) of 7.15% over the 2026–2032 forecast window. This briefing summarizes the practical, decision-focused insights contained in the full report while intentionally withholding granular subsegment figures to direct stakeholders to the source for full, transaction-grade intelligence.

Worldwide Diabetes Lancing Devices Market

Macro momentum: The market’s multi-year expansion is driven by persistent diabetes prevalence, broader uptake of self-monitoring in home care, and an ongoing device refresh cycle focused on safety, comfort and integration with glucose monitoring ecosystems.

Worldwide Diabetes Lancing Devices Market

Regulatory reset: Recent and continuing regulatory decisions are reshaping product pathways and time-to-market expectations. Key reclassifications and labeling expectations increase the bar for safety documentation and post-market controls, while certain device categories now face more onerous premarket requirements.

Worldwide Diabetes Lancing Devices Market

Payer dynamics: Reimbursement codes and coverage policy shifts are materially influencing product commercialization economics. New coding for integrated monitoring cartridges and evolving quantity and device replacement limits under major payers create both constraints and commercial levers.

Consolidation and differentiation: Market concentration metrics indicate a market where a relatively small set of incumbents capture a majority of revenue, but there is still room for innovation-led entrants to disrupt via differentiated comfort/safety features and ecosystem partnerships.

Actionable market sizing and forecast: A transparent top-line and scenario-based forecast through 2032 to inform revenue planning and portfolio prioritization.

Regulatory & reimbursement playbook: Step-by-step guidance on approvals, labeling, and coding strategies needed to secure market access and payer reimbursement.

Competitive benchmarking: Company profiles, capability maps and capability gaps that highlight where incumbents are vulnerable and where new entrants can compete without triggering price wars.

Commercial go-to-market scenarios: Segmented GTM approaches for direct-to-consumer, institutional procurement and pharmacy channels, with break-even analyses for common pricing and reimbursement assumptions.

M&A and partnership blueprints: Target criteria, valuation sensitivities, and integration checklists tailored to the lancing device ecosystem.

Risk register and mitigation playbook: Regulatory, clinical, supply chain and payer risks prioritized by likelihood and business impact, with mitigation playbooks keyed to decision gates in 2026.

The market is characterized by a handful of established medical-device and diagnostics companies that combine legacy channel access, brand recognition and scale manufacturing with a series of smaller, innovation-focused entrants. Aggregate concentration measures show that the top three players account for a clear majority of market activity, and the top five expand that dominance further — a dynamic that simultaneously raises barriers to entry and creates arbitrage opportunities for niche innovators.

F. Hoffmann‑La Roche Ltd (Roche Diabetes Care): Best-in-class channel integration and a strong product portfolio that ties lancing devices to meter ecosystems. Roche leverages brand trust and regulatory footprints to protect premium placements.

Abbott Laboratories: Deep systems integration with glucose-monitoring platforms and a focus on seamless patient workflows; high strategic value for partners seeking meter/lancet compatibility.

Becton, Dickinson and Company (BD): Scale manufacturing and global distribution in both disposable lancets and reusable lancing devices; cost and supply advantages are core strengths.

Ascensia Diabetes Care and LifeScan (OneTouch): Strong presence in consumer meters and matched lancing solutions, enabling channel cross-sell and loyalty-led retention tactics.

Owen Mumford, ARKRAY, Terumo and B. Braun: Regional strength and specialized product lines focused on safety, ergonomics and compliance with evolving labeling expectations.

HTL‑STREFA and Sejoy Biomedical: Notable for sterile safety lancets and recent regulatory activity—Sejoy’s FDA 510(k) clearance in late 2024 highlights the acceleration of more diverse suppliers into regulated markets.

Genteel LLC: An example of differentiation through patient experience innovation (vacuum-assisted, low-pain sampling), offering premium niche potential if paired with effective reimbursement strategies.

The full report contains expanded competitor dossiers including IP positioning, recent approvals (for example, notable 510(k) clearances by leading players), go-to-market case studies and M&A activity mapping to help buyers and defense teams structure 2026 plays.

Regulatory: Recent reclassification moves and labeling guidance have clarified that single-patient use labeling is strongly encouraged to mitigate infection risk, while some multi-user scenarios now face higher regulatory scrutiny. These changes affect product design choices, packaging, and clinical evidence expectations.

Reimbursement: Major payers and Medicare maintain specific HCPCS coding and quantity frameworks that materially influence unit economics and replacement cycles. For example, certain HCPCS codes define typical quantity allowances that companies must account for when modeling price and volume. New code introductions for integrated monitoring cartridges add another layer of commercial strategy for integrated-device players.

Commercial implication: Companies without an articulated coding and payer engagement strategy risk losing price discipline or facing exclusion from key procurement channels; conversely, early engagement and pilots can secure favorable formulary placement and durable volume.

Prioritize integrated ecosystems: Seek partnerships or product integrations that align lancing devices with meters and monitoring platforms to capture higher lifetime value per user.

Differentiate on safety and comfort: Invest in clinical substantiation that demonstrates reduced infection risk and improved patient adherence—two levers that payers reward.

Lock in coding early: Map products to existing and emerging HCPCS codes and secure payer pilots to de-risk commercialization assumptions.

Target niche entry points: For challengers, focus on under‑served clinical or geographic niches where incumbent scale is less protective and regulatory pathways are manageable.

Prepare for consolidation: For strategic acquirers, develop pre-vetted target lists and integration playbooks that prioritize rapid time-to-market and distribution lift.

PW Consulting’s forecast uses a 2025 base year with historical analysis covering 2020–2025 and scenario modeling through 2032 (currency: USD, revenue unit: Million). Our methodology triangulates vendor financials, shipment data, payer rules, regulatory filings and primary interviews across manufacturers, payers and provider networks. The projected CAGR of 7.15% for the forecast interval is supported by sensitivity testing across demand, reimbursement and regulatory scenarios. Market concentration metrics embedded in the full analysis provide a quantitative basis for assessing competitive dynamics and transaction opportunities.

This briefing highlights the strategic value of our Worldwide Diabetes Lancing Devices Market report for decision-makers preparing 2026 strategies. To obtain the full dataset — including granular device-type, regional and end-user splits, pricing matrices, downloadable model files and comprehensive company profiles — please consult the PW Consulting publication page or contact our client services team. The report’s trailer approach is intentional: we present enough depth to guide hypothesis generation and immediate planning while reserving the segment-level intelligence and transaction-grade tables for the full deliverable.

PW Consulting is available to support rapid briefings, custom deep dives, and transaction advisory for companies and investors looking to act in 2026. Our analysts can model scenario-specific outcomes using organization-specific assumptions to convert market insight into executable plans.

For detailed analysis of this topic, please visit the official page:Worldwide Diabetes Lancing Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com