Biosimilar Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-08 12:02:43

PW Consulting’s latest market research — the Worldwide Low Voltage Insulators Market report (base year 2025) — delivers a tight, decision-grade view of a sector undergoing steady expansion and structural change. Our analysis shows the global low voltage insulators market reached roughly USD 4,500 million (base year 2025) after a multi-year recovery from the 2020 baseline, and PW Consulting projects continuation of this growth through our forecast horizon (2026–2032) at a compound annual growth rate (CAGR) of 5.5%. The report is designed to equip executives with the high-resolution strategic inputs they need to set product road maps, supply‑chain commitments and M&A priorities for 2026 and beyond.

Worldwide Low Voltage Insulators Market

Quantified market sizing and a transparent methodology: time-series market size from 2020 through the 2025 base year, and a seven-year forecast (2026–2032) built on bottom-up modelling and scenario overlays for commodity and policy risk.

Worldwide Low Voltage Insulators Market

Competitive benchmarking and capability mapping: profiles and capability assessments of leading vendors, with specific attention to material technology, manufacturing scale, geographic reach and product breadth.

Worldwide Low Voltage Insulators Market

Supply-chain and raw-material risk matrix: scenario-based sensitivity analysis for alumina, kaolin and polymer compound inputs and their impact on margins, unit economics and sourcing strategies.

Standards and regulatory heatmap: practical guidance on IEC conformity testing and its influence on market access, certification cost and time-to-market for new insulator designs.

Commercial playbooks: go-to-market options for OEMs, distributors and new entrants, including pricing levers, after-sales service models and channel strategies tailored to regional regulatory regimes and electrification projects.

Investment and M&A screen: deal templates and valuation sensitivities for targets across the value chain (manufacturing, compound supply, test labs and distribution).

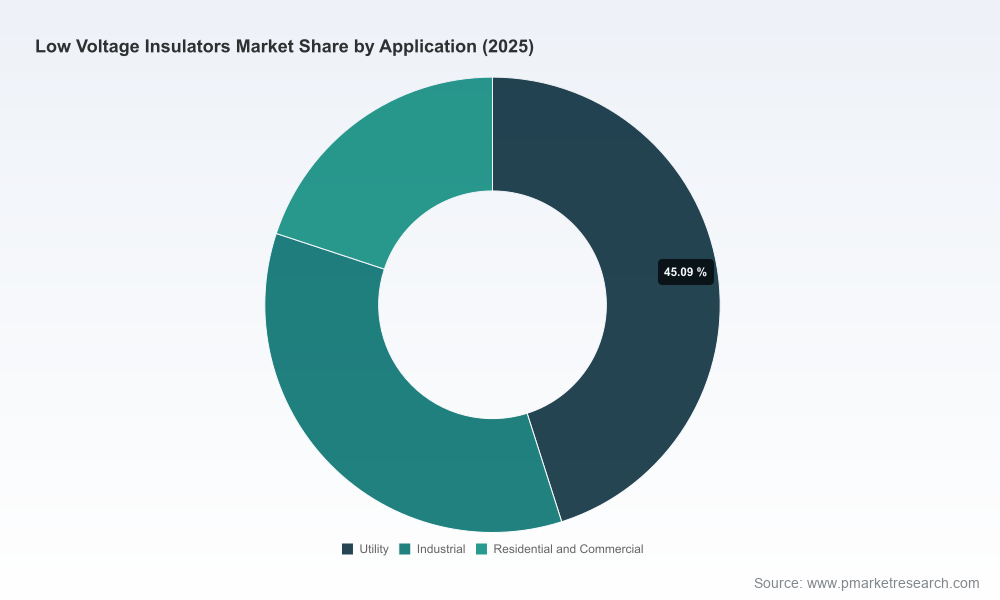

Steady top-line expansion with pockets of volatility. The overall market trajectory reflects continued demand from electrification of residential, commercial and infrastructure projects, while short-term margin pressure is driven by raw-material price swings and energy cost variability.

Material substitution and product differentiation. The market is evolving across three principal material families — ceramic/porcelain, glass, and polymer composites — each carrying distinct cost structures, manufacturing capital intensity and compliance pathways. Our modelling identifies where polymer composites are gaining share on system-level criteria such as weight, impact resistance and total lifecycle cost — and where ceramic and glass retain technical advantages for specific use cases.

Standards and certification are commercial gates. Compliance with international standards (notably IEC performance and test regimes) is non-negotiable for access to many export markets and for specification by utilities and major industrial buyers. Time and cost for laboratory validation materially affect new-product launch calendars.

Concentration and competitive tensions. Market concentration remains moderate, with the top three and top five vendors capturing a notable — but not dominant — share of industry revenue. This structure creates space for regional specialists and engineering-focused challengers to win specification business through superior application engineering and customer service.

Our assessment of incumbent vendors maps their strengths to the commercial plays that will matter in 2026:

nVent ERIFLEX (United States) — product depth and system compatibility: offers a wide range of stand-off insulators manufactured from glass-fibre reinforced polyester with metal inserts, positioning it strongly for busbar and enclosure applications where mechanical stability and leakage control are priorities.

Poinsa (Spain) — European distribution and material breadth: a manufacturer-distributor model spanning porcelain, ceramic and polymeric insulators that benefits from established relationships in distribution networks across multiple voltage classes.

Sediver (France) — glass specialist for overhead distribution: production of toughened and annealed glass insulators tailored to distribution networks underlines a differentiated play in line hardware and dead-end applications.

EREN Isolatoren (Turkey) — scale in SMC/BMC components: high-volume production of support and standoff insulators positions the company as a cost-efficient supplier to electrical equipment OEMs.

PPC Insulators (United States/Europe) — legacy porcelain capability: deep ceramics know-how and cross-Atlantic production footprint support customers needing IEC‑grade porcelain solutions and legacy compatibility.

VIOX Electric (China), TE Connectivity (Switzerland), Termate (UK), LAPP Insulators (Germany) and NGK Insulators (Japan) — complementary positions across busbar systems, enclosure insulators and materials innovation. Several of these players combine product engineering with global sales networks, which matter for large distribution and industrial OEM contracts.

Recent field-level activity underscores the competitive pulse: Zhejiang Haivo’s exhibition of composite insulators at an industry show and NGK’s presence at a leading European power-electronics conference reflect vendor strategies to highlight materials innovation and cross-industry applications into power electronics and grid equipment.

Raw-material cost volatility: alumina and kaolin experienced pronounced spot-price moves that fed through to porcelain and ceramic producers, particularly impacting smaller manufacturers with limited purchasing scale. Polymer compound costs, though exposed to petrochemical cycles, offer opportunities for forward hedging and long-term supply contracts.

Regional manufacturing economics: local availability of kaolinitic clay and beneficiation capacity can be a decisive factor for building or expanding ceramic plants. However, plant capital intensity and IEC compliance testing create a multi-year payback horizon that must be modelled explicitly in 2026 CAPEX plans.

Standards compliance as strategic moat: meeting IEC testing requirements not only protects end-user safety but also functions as a commercial credential. Companies investing early in accredited test capacity or partnering with qualified labs shorten customer acceptance cycles.

PW Consulting translates these dynamics into four executable imperatives for companies and investors planning activity in 2026:

Hedge and vertically secure key inputs. Procureors and smaller producers should prioritize multi-year contracts for alumina/kaolin or secure polymer compound supply via strategic partnerships. Larger players should evaluate backward integration or toll‑processing arrangements where scale justifies investment.

Choose materials strategically — not uniformly. Product portfolios should be rationalized by application economics: reserve ceramics and glass for applications demanding dielectric stability and thermal inertia; deploy polymer composites where mechanical resilience, weight and Total Cost of Ownership (TCO) win specification battles.

Invest in standards and testing as a go‑to‑market enabler. Faster, in-house IEC‑grade testing and accredited labs reduce approval timelines for major utility and industrial tenders. For companies targeting exports, compliance investments should be treated as commercial rather than solely technical spending.

Pursue targeted M&A and alliances to plug capability gaps. Given the sector’s moderate concentration (CR3 ~24.5%, CR5 ~32.8%), acquisitive moves can quickly elevate market position in selected geographies or material technologies without encountering prohibitive antitrust attention in most jurisdictions.

Manufacturers: Build a two‑track sourcing strategy — secure long-term contracts for ceramics feedstock while piloting polymer compound formulations that reduce cycle time and energy intensity. Quantify margin sensitivity to alumina and polymer prices in your 2026 budget cycle.

Distributors/OEMs: Strengthen technical specification services. Investing in application engineering and localized inventory stocking reduces project lead times and creates differentiation versus pure commodity suppliers.

Investors/PE: Target bolt-on acquisitions of accredited testing labs, compound suppliers or niche manufacturers producing high-margin specialty parts. Use our valuation templates to stress-test each target under commodity price and standards‑compliance scenarios.

With the base year established at 2025 and a clear forecast horizon to 2032, 2026 represents the first planning window in which firms will translate pandemic recovery lessons into durable strategy. Supply-chain resets, energy cost normalization and accelerating electrification projects make 2026 the moment to commit to material strategy, production footprint and standards investment. Our forecast (CAGR 5.5% through 2032) provides a bridge between tactical near-term actions and long-term portfolio bets.

This briefing highlights the structural themes and actionable levers we believe will drive competitive advantage in the low voltage insulators market. PW Consulting’s full Worldwide Low Voltage Insulators Market report includes granular segmentation models, downloadable Excel workbooks, supplier scorecards and scenario dashboards that quantify the commercial impact of every major decision outlined above.

For access to the full dataset, the interactive model and bespoke advisory engagements to implement the report’s recommendations, please contact PW Consulting’s Research Sales team or visit our report page on the PW Consulting website.

PW Consulting — translating market data into decisive action for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Low Voltage Insulators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com