Feed Grade Threonine Market Overview: Key Drivers and Challenges

Other |

2026-04-15 04:11:28

As subterranean threats migrate from episodic incidents to organized modalities, the market for tunnel detection systems is moving from niche procurements to mainstream security planning. PW Consulting’s forthcoming Worldwide Tunnel Detection System Market report — grounded in a 2020–2025 historical baseline, using 2025 as the reference year and projecting across 2026–2032 — delivers the kind of decision-grade intelligence procurement teams, program offices, and infrastructure operators will need to act decisively in 2026.

Worldwide Tunnel Detection System Market

Our market model shows a robust multi-year expansion: the global market expands from roughly USD 1.98 billion in 2020 to an estimated USD 4.87 billion by 2032, reflecting a compound annual growth rate (CAGR) of approximately 8.04% across the forecast window. Importantly for near-term planners, the market grows from a 2025 baseline (about USD 2.84 billion) to an initial post-base-year projection for 2026 (about USD 3.15 billion), signaling both renewed procurement momentum and budgetary opportunities beginning in 2026.

Worldwide Tunnel Detection System Market

These topline dynamics are being driven by three convergent forces: heightened border and critical-infrastructure security mandates, rapid improvements in sensor analytics (AI-assisted verification and multimodal fusion), and expanding public investment programs aimed at persistent subterranean surveillance. Notably, policy actions such as the U.S. Department of Homeland Security’s 2025 allocation of approximately USD 100 million to expand persistent surveillance and detection capabilities materially de-risk early investments and create clear program funding pathways for the year ahead.

Worldwide Tunnel Detection System Market

Comprehensive market sizing and scenario frameworks: Transparent methodology describing how we convert sensor-level performance characteristics into procurement-ready demand curves for 2026–2032.

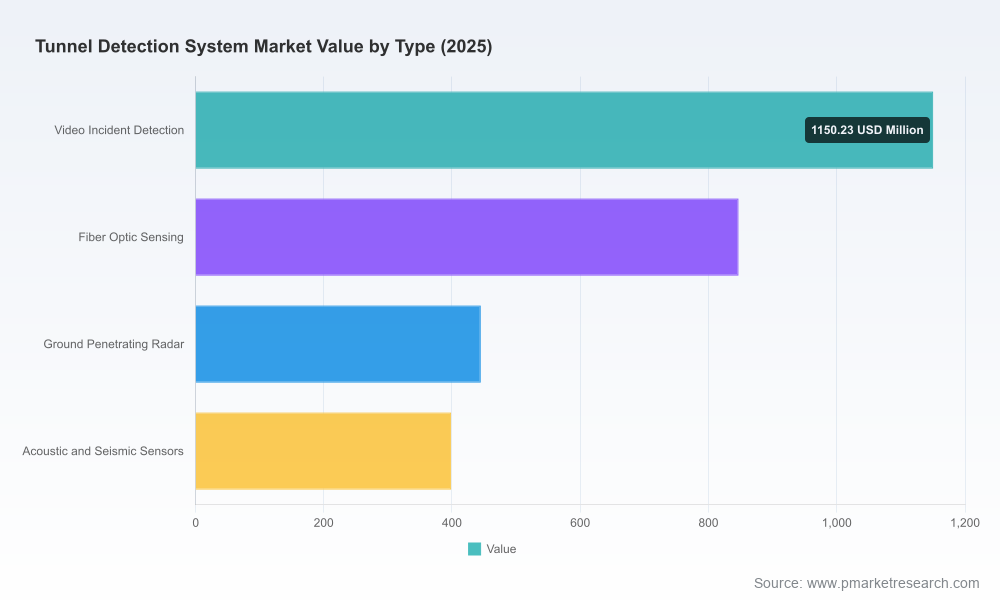

Technology assessment and deployment playbooks: Comparative evaluation of detection modalities (seismic/acoustic networks, fiber-optic sensing, ground-penetrating radar, video/incident-detection overlays), with operational pros/cons, environmental sensitivity matrices, and false-alarm mitigation strategies.

Integration and systems engineering guidance: Best practices for integrating subterranean detection feeds with VMS, command-and-control suites, and cross-domain ISR, including data throughput and latency targets for real-time interdiction.

Procurement and contracting templates: Recommended commercial models, performance-based metrics, service-level agreements, and maintenance lifecycle costing to accelerate RFP and PWS development in 2026.

Risk maps and component supply analysis: Identification of critical hardware dependencies (e.g., specialized geophones, accelerometers, fiber-optic and wireless sensor elements), single points of failure, and mitigation strategies for sourcing continuity and spares planning.

Vendor landscape and competitive profiling: Tactical profiles of incumbent and emerging vendors, mapped to capability clusters and contracting archetypes to help buyers shortlist partners for pilots and scale deployments.

Case studies and ROI models: Real-world deployment examples with quantified impact on detection timelines, false-alarm rates, and interdiction outcomes, plus models to calculate total cost of ownership and payback horizons under multiple operational scenarios.

The market exhibits moderate concentration — our analysis shows the combined share of the three largest players represents a material but not dominant portion of market revenue, with the top five accounting for under half of the market. This structure creates opportunities for established defense primes and agile niche technology providers alike. Below we summarize the operational profiles of leading vendors highlighted in the report:

SensoGuard Seismic Solutions (Israel | https://sensoguard.com): Specializes in wired and wireless seismic tunnel detection platforms (InvisiFence Plus, AIO XR) optimized for buried intrusion and tunneling detection to depths relevant for border and high-value perimeter protection. Their systems emphasize algorithmic threat classification, low false-alarm footprints, and native integration with VMS and control-room ecosystems — properties that make them a compelling vendor for infrastructure operators seeking rapid verification capability.

Geospace Technologies (United States | https://www.geospace.com): Offers SADAR arrays combining seismic and acoustic sensing for three-dimensional localization and real-time tracking of underground excavation activity. Their deployments have focused on port and border security and installations where continuous localization and multi-sensor fusion are operational requirements.

Elbit Systems (Israel | https://www.elbitsystems.com): Delivers a portfolio of acoustic, vibration, and sensor-based tunnel detection and counter-intrusion solutions with AI-enabled analytics and proven fielded systems for military and homeland security applications. Recent multi-year border security deployments underscore their ability to execute at scale on government contracts.

US Radar Inc. (United States | https://usradar.com): Focused on ground-penetrating radar (GPR) technologies, including deep-penetration systems for geophysical imaging and subsurface void detection. GPR continues to be an essential modality where imaging and characterization (depth, void geometry) are prioritized.

Lockheed Martin (United States | https://www.lockheedmartin.com): Leverages advanced gravity gradiometry and GPR-based systems to detect and characterize subterranean threats, with expertise in airborne and surface sensor integration and defense-oriented program execution.

Product and capability rollouts — SensoGuard’s 2026 promotional updates emphasize AI-assisted verification within its buried seismic systems, illustrating the trend toward on-sensor intelligence to cut false alarms and reduce operator burden.

Program-level deployments — Elbit Systems’ contract activity through 2025 (additional integrated surveillance towers with AI-enabled sensors) is an indicator of sustained demand from large government customers that prioritize modular, extendable systems.

Policy and funding tailwinds — Government allocations to persistent subterranean surveillance technologies are creating explicit procurement pathways and opening funding windows for pilot-to-scale transitions in 2026.

Organizations preparing budgets or designing procurements for 2026 must treat tunnel detection capability as an integrated system procurement, not a point-sensor buy. Key strategic takeaways drawn from our report:

Prioritize pilot-to-scale pathways: Initiate structured pilot programs in 2026 with clearly defined performance metrics (detection latency, probability of detection, false-alarm rate, integration readiness). Use pilots to validate sensor fusion strategies before committing to full-scale purchases.

Design for integration: Select vendors and architectures that offer open, standards-based APIs and proven VMS/command-and-control integrations to limit lock-in and simplify multi-vendor fusion.

Mitigate supply-chain concentration: Identify alternate suppliers for key components (geophones, accelerometers, fiber-optic sensing elements) and include spares and logistics clauses in contracts to address lead-time risk.

Leverage funding windows: Align RFP timelines with government funding cycles and grant programs active in 2025–2026 to maximize the likelihood of funding approval and accelerate procurement execution.

Emphasize lifecycle economics: Negotiate performance-based maintenance and health-monitoring contracts that shift operational risk to vendors while enabling predictable lifecycle costing.

Consider strategic partnerships: For operators lacking in-house integration capability, partnering with systems integrators or selecting vendors with proven integrator partnerships can shorten fielding timelines.

Plan for analytics evolution: Expect incremental improvements in AI-enabled classification and anomaly detection — procure systems that can accept model updates and support secure OTA (over-the-air) analytics refreshes.

This preview outlines the strategic contours decision-makers will face in 2026, but the actionable edge comes from granular modeling, vendor comparisons, and procurement-ready artifacts contained in the full report. PW Consulting’s complete research includes scenario-based demand curves, detailed vendor scorecards, integration checklists, negotiated contract language examples, and TCO/ROI models that will materially shorten procurement cycles and reduce program risk.

If your 2026 plans require certainty — about timing, technology trade-offs, supplier risk, or budgetary justification — the full Worldwide Tunnel Detection System Market report provides the playbook to move from assessment to acquisition with confidence.

For detailed analysis of this topic, please visit the official page:Worldwide Tunnel Detection System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com