Worldwide Non-woven Sponge Market: Strategic Outlook for 2026 Decision-Making

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I am pleased to introduce our latest market intelligence brief — a forward-looking, practitioner-focused synopsis drawn from the Worldwide Non-woven Sponge Market report (base year 2025, forecast period 2026–2032). This executive narrative is designed to help C-suite executives, commercial leads, procurement officers, and M&A teams orient their 2026 choices around near-term demand, cost dynamics, and competitive positioning — while preserving the granular model outputs and segmented datasets for subscribers who require the full analytical toolkit.

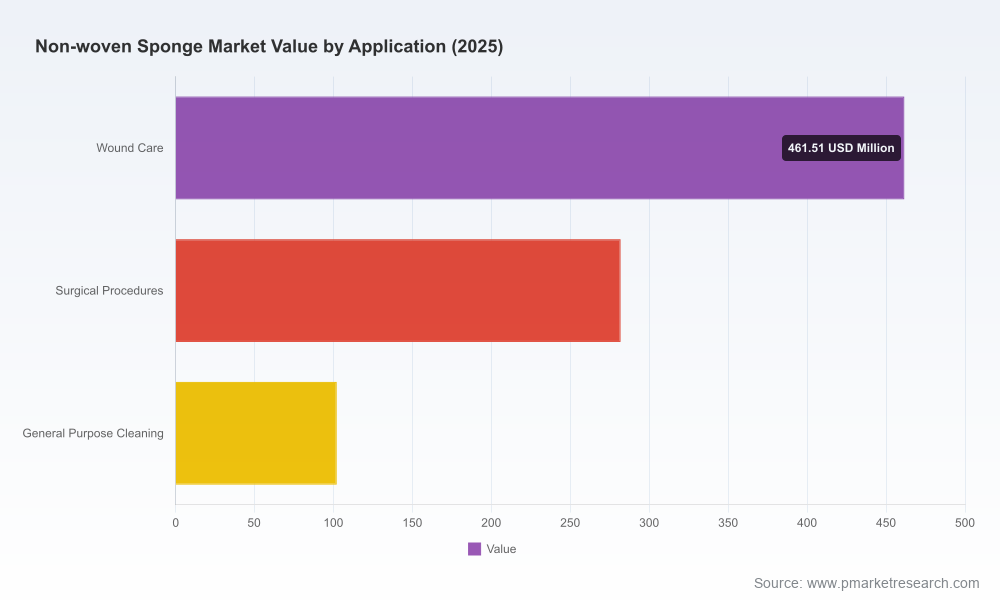

Worldwide Non-woven Sponge Market

Market in a snapshot: what the macro numbers tell us

Non-woven sponges, a core consumable across wound care, surgical procedures and hygiene applications, show steady expansion. Our compiled series indicates growth from a mid-single‑hundred million market in 2020 to USD 845.5 Million in 2025 (base year), with a trajectory that accelerates through the forecast horizon to reach approximately USD 1,173.9 Million by 2032. Over the modeled forecast window (2026–2032) the market exhibits a compound annual growth rate (CAGR) of 4.82%.

Worldwide Non-woven Sponge Market

Two structural features are apparent from the top-line dynamics: first, demand is resilient and underpinned by healthcare utilization and single‑use product adoption; second, volatility in upstream inputs and trade/regulatory frictions materially shape near-term margins and sourcing choices. Competitive concentration is moderate — our concentration ratios indicate meaningful scale advantages for the largest suppliers, but room for differentiated players and contract manufacturers to capture segment-specific value.

Worldwide Non-woven Sponge Market

Why this matters for 2026 strategy

- Investment timing: With mid-single-digit CAGR and clear upside in certain clinical-use segments, 2026 is a strategic inflection year for capacity investments and contract renegotiations. Firms that lock in flexible supply agreements now will capture margin relief as demand normalizes.

- Sourcing and tariffs: Current tariff regimes and material cost cycles require procurement to be more scenario‑driven. Firms reliant on cross-border supply from regions subject to tariffs must model duty impacts against near-shore and domestic production options.

- Regulatory compliance as a market discriminator: As regulators refine medical device and sterile-packaging expectations, the cost of non-compliance (or delayed certification) can be immediate and revenue‑eroding. Prioritizing regulatory readiness will be essential for speed-to-market in 2026.

Key demand and supply dynamics shaping the 2026 playbook

Our assessment highlights four interrelated dynamics that will determine winners and laggards next year.

- Clinical demand elasticity and product mix. Wound-care traction and procedural volume recovery are the primary demand engines. Manufacturers that can provide sterility-assured, low-lint, high‑absorbency formats will command premium shelf space and hospital formularies.

- Raw material pressure and pass-through strategies. Polypropylene — the dominant feedstock for many non-woven formats — averaged roughly USD 1,200 per metric ton in Q4 2024. That level, combined with feedstock volatility, makes cost-pass-through mechanisms, hedging strategies, and alternative polymer sourcing central to 2026 margin plans.

- Regulatory and trade constraints. The European regulatory baseline for medical non-wovens and ongoing tariff regimes (including duties on certain imports) are shifting sourcing economics. Compliance investments (e.g., meeting Class I sterile packaging requirements) are fast becoming preconditions for participation in higher-margin hospital channels.

- Labor and manufacturing economics. Labor cost inflation in key manufacturing jurisdictions (U.S. fabrication costs rose in the order of several percent year-over-year in 2024) is altering the calculus between in-house production and outsourcing to lower-cost contract manufacturers.

What the report delivers — practical, decision‑grade tools

We built this report to be operational. For 2026 planning cycles, executives will find the following modules immediately actionable:

- Top-line forecasting model (2026–2032) with scenario toggles for volume, price, and contract mix — built to export into corporate planning tools.

- Raw material sensitivity analysis that quantifies margin impact across polymer price scenarios and identifies break-even points for cost pass-through vs. absorption.

- Regulatory impact matrix outlining jurisdictional requirements, certification lead-times, and compliance cost estimates for sterile medical applications.

- Manufacturing footprint optimization playbook that contrasts CAPEX expansion, retrofit, and contract manufacturing—with a modeled TCO (total cost of ownership) by option.

- Procurement and supplier scorecards for vendor selection, including service-level KPIs, quality metrics, and risk indicators (tariff exposure, single‑source dependence).

- M&A and JV screening criteria with a prioritized target list for manufacturing scale, geographic access, or additive capabilities (e.g., absorbency technologies).

- A go‑to‑market and commercial playbook for winning hospital formularies, dispel packs, and private-label channels, including pricing strategies and tender play simulations.

- Regulatory and compliance checklist tailored for sterile packaging and medical-device-adjacent products — designed for rapid audits and certification planning.

Competitive landscape: what incumbents and challengers are doing

The market is populated by global medical distributors, large materials manufacturers, dedicated non-woven specialists and regional exporters. Market leaders leverage scale, integrated distribution, and established quality credentials; mid-sized specialists compete through customization, OEM partnerships and nimble product development. Recent public developments illustrate these strategic moves:

- Cardinal Health expanded its surgical prep portfolio with enhanced absorbency products in late 2024 — a move that signals continued investment in premium sterile formats and bundled procedural solutions.

- 3M refreshed its product catalog in 2024 with new sterile sizes and configurations, underscoring the demand for inventory breadth in sterile surgical consumables.

- Medline’s ISO 13485 recertification earlier in 2024 reaffirms certification as a competitive necessity for suppliers seeking hospital and OEM contracts.

From a strategic standpoint, incumbent advantages include scale purchasing, distribution reach, and existing formulary relationships. Opportunities exist for contract manufacturers and regional suppliers to win through cost competitiveness, speed of customization, or value-added services (sterile packaging solutions, private label partnerships, or integrated logistics).

Strategic playbook recommendations for 2026

Based on our modeling and client engagements, we recommend five priority moves for leaders and investors active in the non-woven sponge market in 2026:

- Operationalize a raw material hedging and sourcing strategy. Quantify exposure to polypropylene price swings and create alternate-sourcing lanes with clear duty and lead-time profiles.

- Prioritize regulatory readiness investments for sterile product lines. Certification timelines are non-linear; early investment secures market access and pricing power.

- Adopt a hybrid manufacturing approach. Combine core in-house production for high-value sterile SKUs with vetted contract manufacturers for commodity non-sterile formats to preserve margin and flexibility.

- Differentiate through product and service bundling. Hospitals increasingly preference simplified procurement — packaged procedural kits, validated sterilization partners, and integrated logistics win contracts.

- Pursue targeted M&A or JVs to secure upstream feedstock or regional distribution channels — especially in markets where tariffs or freight volatility significantly change landed cost economics.

Where the report intentionally holds back — and why

In this briefing we have highlighted the macro trajectory, competitive posture, and strategic implications for 2026 planning. Deliberately, we have not disclosed granular regional, application-level splits, or full company-level segment revenues in this public summary. Those detailed segmentations, node-by-node forecasts, supplier scorecards and financial model templates are core deliverables of the full report and are available through our subscription channels. This “trailer” approach lets decision-makers validate strategic direction here, while preserving the full, actionable datasets for subscribers who need execution-ready intelligence.

Next steps for executives

If your 2026 plan requires rigorous scenario modeling, contract negotiation ammunition, or a prioritized M&A shortlist, PW Consulting can deliver a tailored engagement derived from the report’s models. Typical quick-start engagements we run for clients include: a two-week raw material exposure assessment, a four-week manufacturing footprint optimization, or a six-week tender and formulary win program that maps directly to hospital purchasing cycles.

To access the full data toolbox — including segmented forecasts, supplier scorecards, and downloadable Excel models — please refer to the report landing page. The full study provides the actionable line-by-line intelligence procurement teams, product managers and corporate development professionals need to convert 2026 uncertainty into strategic advantage.

Prepared by: PW Consulting — Global Health & Materials Practice. For inquiries about bespoke briefings or to license the full Worldwide Non-woven Sponge Market report, contact our research desk.

For detailed analysis of this topic, please visit the official page:Worldwide Non-woven Sponge Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com