Transport and Logistics Market: Size, Share, and Future Growth

Other |

2026-06-15 05:51:01

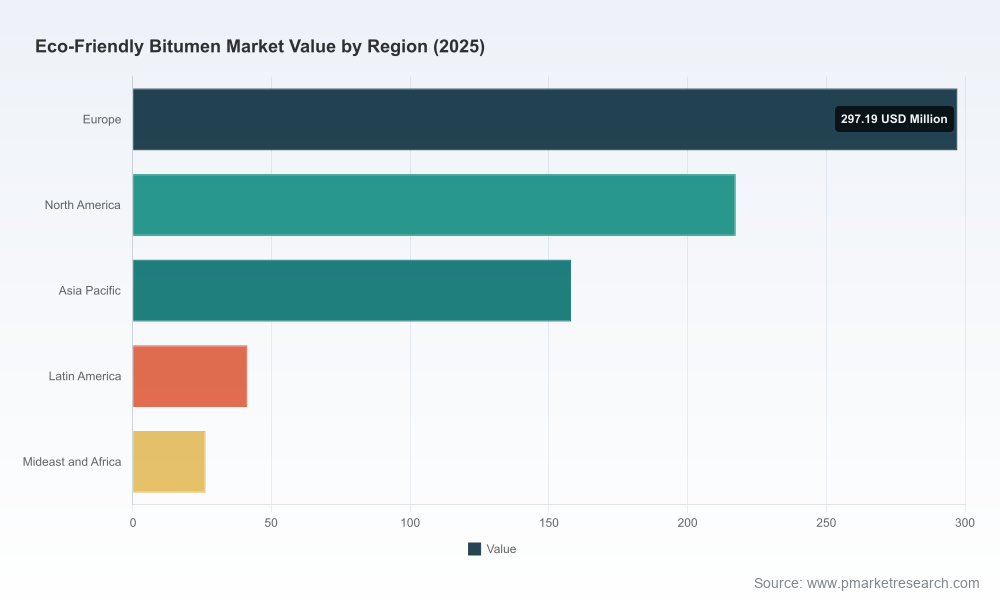

PW Consulting’s latest market study, Worldwide Eco‑Friendly Bitumen Market (base year 2025, forecast 2026–2032), presents an actionable intelligence package for executives preparing strategic moves in 2026. The global market has accelerated sharply in recent years — expanding from approximately USD 410.6 million in 2020 to USD 740.0 million in 2025 — and is forecast to continue at a compound annual growth rate (CAGR) of 12.54% through 2032, reflecting sustained policy push, procurement reform, and rapid product innovation. This briefing highlights the report’s strategic value without disclosing our proprietary segment-level datapoints, designed to prompt decision-makers to engage with the full study for transaction‑grade insights.

Worldwide Eco-Friendly Bitumen Market

Policy inflection points will drive procurement: mandates such as the EU Green Deal’s requirement for bio‑based content in public road contracts (effective from 2025) turn sustainability from a differentiator into a de‑facto procurement criterion. Aligning product portfolios and certification roadmaps to meet these requirements is urgent for suppliers targeting public infrastructure spend.

Worldwide Eco-Friendly Bitumen Market

Standards are lowering technical adoption barriers: the introduction of standardized testing protocols (e.g., AASHTO MP 45‑24 in the U.S.) reduces adoption risk for road authorities and contractors, accelerating market uptake for certified bio‑modified binders.

Worldwide Eco-Friendly Bitumen Market

Input volatility and trade policy reshape cost models: feedstock markets matter — vegetable oil prices, a key input for many bio‑binders, rose materially into Q4 2024 — and trade actions (for example, tariffs on certain imports enacted in early 2025) are already influencing sourcing strategies and near‑term margins.

Three structural dynamics will determine winners in 2026 and beyond: regulatory alignment, feedstock and recycling economics, and scale‑efficient manufacturing. Our study documents how these forces interact and provides playbooks that convert them into executable moves.

Regulatory alignment: Suppliers that combine product performance with third‑party certification are breaking into large public tenders. Iterchimica’s EN 15381 certification for its ReRoad rejuvenator (June 2024) is an example of a certification unlocking access to recycled asphalt programs across European highways.

Scale and industrialization: Capacity matters for price competitiveness. Green Asphalt’s capacity expansion in California (March 2024) signals that bio‑binder producers who can scale to mid‑five‑figure tonnages can materially influence local supply economics and contracting outcomes.

Technology breadth: Major players are pursuing differentiated technical levers — from bio‑naphtha blends to enzyme‑based rejuvenators and high‑recycled content mixes. Shell Bitumen’s October 2024 launch of a bio‑naphtha modified product, said to deliver significant CO2 reductions, underscores legacy suppliers’ push to industrialize low‑carbon options.

The sector remains only moderately consolidated: the combined share of the top three and top five players indicates meaningful room for regional specialists and new entrants to scale. Competitive behaviors fall into three distinct archetypes:

Tech‑centric innovators (small to mid caps) — focused on proprietary chemistries or recycling processes to win pilots and local contracts. Companies such as Iterchimica and Bituchem exemplify this route: fast certification cycles and niche performance advantages.

Resource‑integrated players — firms that combine feedstock sourcing, binder production and asphalt mix manufacturing to control cost and traceability. Some Canadian and European players pursuing high recycled content mixes illustrate this vertical model.

Incumbent majors — established oil and materials suppliers are retrofitting portfolios with renewable blends and low‑temp technologies, leveraging distribution networks to scale adoption. Shell Bitumen and Colas are examples of incumbents using brand, certification and channel reach to accelerate adoption.

Recent industry developments point to accelerating commercialization: Shell’s bio‑naphtha offering (Oct 2024), Iterchimica’s EN certification (June 2024), and Green Asphalt’s U.S. capacity expansion (Mar 2024) create a pattern — innovation, certification, scale — that new entrants must replicate or counter through strategic partnerships.

Our report is designed as an operational playbook for 2026 decisions. Highlights include:

Market sizing and high‑resolution forecasting (global and by major market drivers) with scenario variants that quantify the impact of feedstock cost shocks, tariff regimes and procurement mandates on revenues and unit margins.

Regulatory & standards matrix mapping regional mandates, procurement criteria and certification pathways that matter to suppliers targeting public works or large private portfolios.

Technology readiness assessments and performance benchmarking for bio‑modification, reclamation/rejuvenation, warm‑mix and high‑recycled formulations — each linked to practical test protocols and sourcing implications.

Supply chain and unit economics models: plant capex/OPEX benchmarking, break‑even analyses under various input price trajectories, and raw material procurement playbooks (including hedging and local sourcing strategies).

Commercial playbooks and tender templates for suppliers and contractors to translate environmental attributes into procurement wins and premium capture.

Vendor due‑diligence checklists and M&A screening scorecards for private equity or corporates assessing bolt‑on acquisitions or greenfield investments.

To preserve the study’s value as a transaction‑grade resource we intentionally withhold certain segment‑level figures in this briefing; the full report contains the granular breakdowns and downloadable models necessary to size opportunities and structure deals.

Manufacturers and binders: finalize certification pathways and align plant expansions to certified product demand windows. Prioritize investments that reduce CO2 intensity per ton and that are compatible with standardized testing protocols to fast‑track public procurement access.

Asphalt producers and contractors: pilot low‑temp and high‑recycled mixes on low‑risk corridors to build performance track records. Use life‑cycle cost metrics rather than capex alone to capture the whole‑of‑asset value, and build supplier partnerships that guarantee feedstock.

Investors and corporate development teams: screen targets using a three‑way lens — technology defensibility, certification/status, and scale economics. Expect attractive consolidation opportunities where technology leaders lack downstream distribution.

Public sector and procurers: adopt procurement frameworks that value life‑cycle emissions and recyclability, and create staged tenders that allow new technologies to scale without compromising performance or budgets.

Feedstock price volatility — mitigate through diversified sourcing, offtake agreements with agricultural processors, and blended product strategies that reduce single‑feedstock exposure.

Regulatory shifts and trade actions — maintain an active compliance and government affairs function; use scenario planning to stress test export/import strategies against tariffs and local content rules.

Technical acceptance risk — invest in third‑party certification and independent pilot projects with accredited labs and road authorities to accelerate mainstreaming.

Reputational risk — ensure transparent carbon accounting and chain‑of‑custody systems to prevent greenwashing accusations and to enable credible claims in tenders.

PW Consulting delivers end‑to‑end advisory for market entry, scale‑up, and transaction support in the eco‑friendly bitumen value chain. Engagement options include rapid due‑diligence sprints for M&A, full commercial diligence with integrated capex/OPEX models, procurement redesign workshops for public authorities, and bespoke pilot‑to‑scale implementation programs for manufacturers and contractors.

For executives making 2026 bets, the critical distinction will be between those who have scenario‑proofed supply chains, secured certification pathways, and structured commercial models that monetize environmental attributes — and those who have not. Our report supplies the quantitative models, competitive intelligence and operational templates to bridge that gap. Notable market signals — such as Shell’s renewed push into bio‑blends (Oct 2024), Iterchimica’s certification milestone (June 2024), and Green Asphalt’s capacity scale‑up (Mar 2024) — illustrate the pace at which the commercial environment is changing. Coupled with evolving standards and the dynamics of feedstock markets, these developments create both near‑term dislocations and medium‑term consolidation opportunities.

Access the full report for the detailed segmentation tables, downloadable financial models, supplier scorecards, and the tactical templates that enable immediate execution. PW Consulting’s analysts stand ready to brief boards and investor committees with tailored scenarios and to support the rapid deployment of the critical 2026 initiatives outlined above.

For detailed analysis of this topic, please visit the official page:Worldwide Eco-Friendly Bitumen Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com