PW Consulting Announces Strategic Brief: Worldwide Automatic Wafer Dicing Saw Market — Critical Guidance for 2026 Decision-Makers

As semiconductor supply chains accelerate into a new phase of advanced packaging and heterogeneous integration, PW Consulting’s latest market study on the Worldwide Automatic Wafer Dicing Saw Market delivers timely, actionable insight for executives planning capital allocation, sourcing, and technology roadmaps in 2026. Drawing on a five‑year historical base and a fresh seven‑year forecast, this briefing highlights where the market is headed, the competitive dynamics that will shape supplier choice, and the procurement and regulatory pressures buyers must plan around.

Worldwide Automatic Wafer Dicing Saw Market

Market trajectory at a glance

Our analysis shows the automatic wafer dicing saw market has moved from an emerging, capacity‑led cycle into a structurally expanding market driven by advanced packaging and new substrate materials. Measured on a total revenue basis, the market expanded notably between 2020 and 2025, and PW Consulting projects continued expansion through the 2026–2032 forecast horizon. Base‑year figures and our forecast indicate a compound annual growth rate (CAGR) of 6.98% for the forecast period — a sustained growth profile that elevates the category from tactical equipment spend to strategic manufacturing enabler for both front‑end and advanced back‑end fabs.

Worldwide Automatic Wafer Dicing Saw Market

For procurement and capital planning teams, the implication is clear: the dicing saw is no longer a fungible commodity line item. Investments made in 2026 will influence throughput, yield on thin and reconstituted wafers, and the cost structure of downstream packaging operations for the better part of this decade.

Worldwide Automatic Wafer Dicing Saw Market

Key macro drivers shaping demand

- Advanced packaging adoption: Technologies such as 2.5D/3D integration, fan‑out wafer‑level packaging and chiplet assemblies are increasing demand for high‑precision singulation of thin, fragile and reconstituted wafers. These applications place a premium on systems capable of controlling kerf, minimizing chipping, and supporting novel dicing patterns.

- New substrate materials: Growth in wide‑bandgap devices and optoelectronics has elevated processing of hard and brittle substrates (e.g., SiC, sapphire), where non‑contact and water‑assisted laser approaches are competing with diamond‑blade mechanical cutting.

- Automation and inline intelligence: Manufacturers are upgrading to systems with AI‑enabled monitoring, robotic wafer handling and SEMI‑compliant automation to reduce cycle time variability and stabilize yields across larger wafer formats.

- Consumables and aftermarket economics: Diamond blades and blade management represent a significant share of consumable spend; optimized blade life management and supply agreements can materially change unit economics over the lifetime of a tool.

Competitive structure — a concentrated market with distinct playbooks

The vendor landscape remains highly concentrated, with the top suppliers commanding the large majority of market revenue. This concentration creates a dual reality for customers: access to mature, high‑reliability technology comes from incumbent suppliers with deep installed bases, while pockets of innovation emerge from specialized vendors focusing on laser dicing and niche applications.

- DISCO Corporation (Tokyo): The company continues to set the product cadence with high‑precision, dual‑spindle platforms and incremental innovations such as AI‑driven kerf monitoring and SEMI‑compliant robotic interfaces. Recent product introductions underline its focus on scaling automation for larger format wafers and package singulation.

- Tokyo Seimitsu / Accretech (Tokyo): Accretech’s road map emphasizes 300mm readiness and blade life automation, and strategic partnerships to secure tooling inputs (e.g., joint development of hub blades) strengthen its vertical control over performance‑critical components.

- Advanced Dicing Technologies (ADT) / Kulicke & Soffa: ADT’s twin‑spindle architectures and ADT’s channel via parent companies broaden commercial reach into back‑end lines where compatibility with package formats like QFN and BGA matters most.

- Synova (Switzerland): Laser MicroJet technology positions Synova as the go‑to vendor for damage‑sensitive or hard substrates; its approach is a salient alternative where mechanical dicing meets material limits.

- Regional and emerging OEMs: A set of China‑based vendors and specialist European/U.S. suppliers supply differentiated price‑performance tradeoffs, faster local support, or niche process capabilities. These vendors are important for procurement diversification and regional supply resilience.

Collectively, the market’s concentration and vendor differentiation mean that selection of a dicing saw supplier is both a technical and strategic decision — involving service coverage, roadmap alignment, consumables provisioning and geopolitical risk.

Technology and product trends to watch in 2026

- AI and inline metrology: Expect broader deployment of real‑time kerf and blade wear monitoring integrated with factory MES systems. These features shift the value proposition from pure throughput to predictable yield and lower rework costs.

- Laser and hybrid singulation: For hard substrates and thin‑wafer singulation, laser options are transitioning from specialized proof‑points to semi‑mainstream choices where damage‑free cutting justifies capital premium.

- Automation ecosystems: SEMI‑standard robotic interfaces and interoperability with wafer handling and AGV systems will become baseline expectations for new purchases in advanced packaging lines.

- Consumables optimization: Blade life management, automated dressing and supply‑chain contracts for diamond tooling will be a decisive differentiator in total cost of ownership (TCO) analyses.

Regulatory and supply‑chain considerations

Two intersecting regulatory developments will materially affect sourcing strategies in 2026 and beyond: recent U.S. federal procurement proposals and trade investigations that target critical semiconductor equipment and related imports. These measures introduce potential constraints on government procurement channels and could cascade into private sector supplier evaluations, particularly for buyers with U.S. government contracts or multisource needs across jurisdictions.

For procurement leaders, the strategic imperative is to stress‑test supplier roadmaps against foreseeable restrictions, secure alternative sourcing for critical consumables (notably diamond blades), and consider commercial terms that preserve flexibility, such as multi‑year service agreements with transfer clauses or regional stocking commitments.

Implications for 2026 corporate strategy — five action points

- Reframe CapEx decision criteria: Prioritize systems that deliver demonstrable yield stability for thin and reconstituted wafers over headline throughput metrics alone. Require vendors to provide TCO models that include blade and consumable trajectories.

- Diversify supplier risk: Establish at least two validated suppliers per critical process class (mechanical dual‑spindle and laser/hybrid) and negotiate regional service SLAs to mitigate geopolitical and logistics disruption.

- Invest in automation and data integration: Mandate SEMI‑compliant interfaces and AI‑enabled monitoring capabilities in new purchases to reduce process variability and lower per‑device singulation costs.

- Lock in consumables economics: Move from transactional blade purchases to strategic supplier partnerships that include performance‑based pricing, lifecycle warranties and shared KPIs for blade life.

- Scenario plan for regulatory shocks: Incorporate regulatory stress tests into supplier qualification, including alternate sourcing, re‑routing logistics and contractual escape mechanisms.

What PW Consulting’s full report delivers

The published study is designed as a practical playbook for 2026 planners. It includes:

- Robust market sizing and historic trend analysis through 2025, and a 2026–2032 forecast model (including CAGR assumptions and sensitivity scenarios).

- Competitive intelligence profiles for leading OEMs and specialized vendors, including product road maps, installed base assessments and strategic positioning.

- Technology radar mapping mechanical, laser and hybrid singulation approaches with recommended application fit‑maps (by substrate and packaging type).

- TCO and CapEx decision frameworks, including consumables modeling, maintenance cost curves and ROI calculators tailored for packaging and discrete device lines.

- Regulatory and supply‑chain risk matrices with mitigation playbooks and procurement templates for multi‑jurisdiction deals.

- Actionable M&A and partnership targets identified for both equipment OEMs and tooling/consumable specialists.

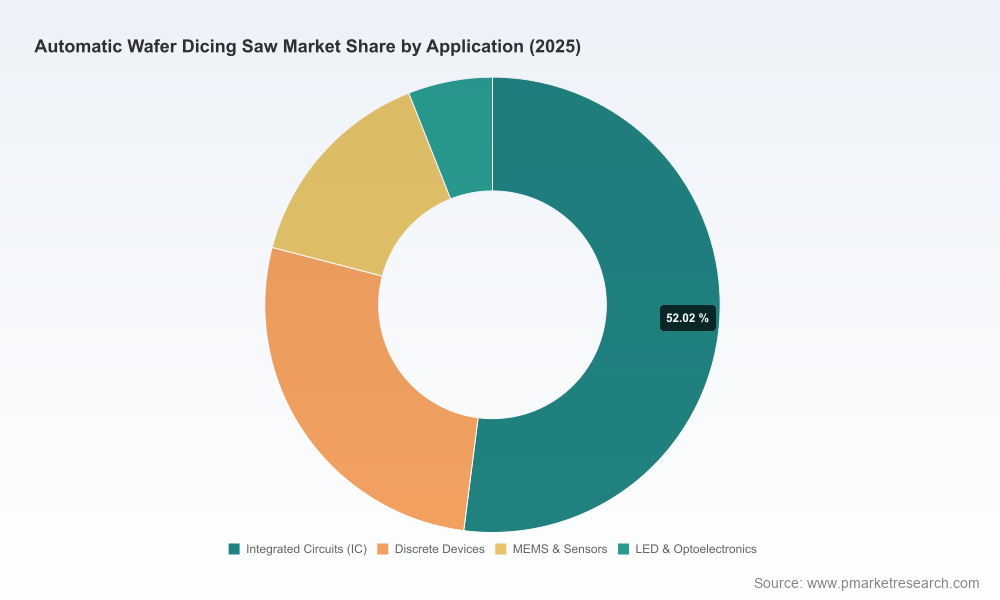

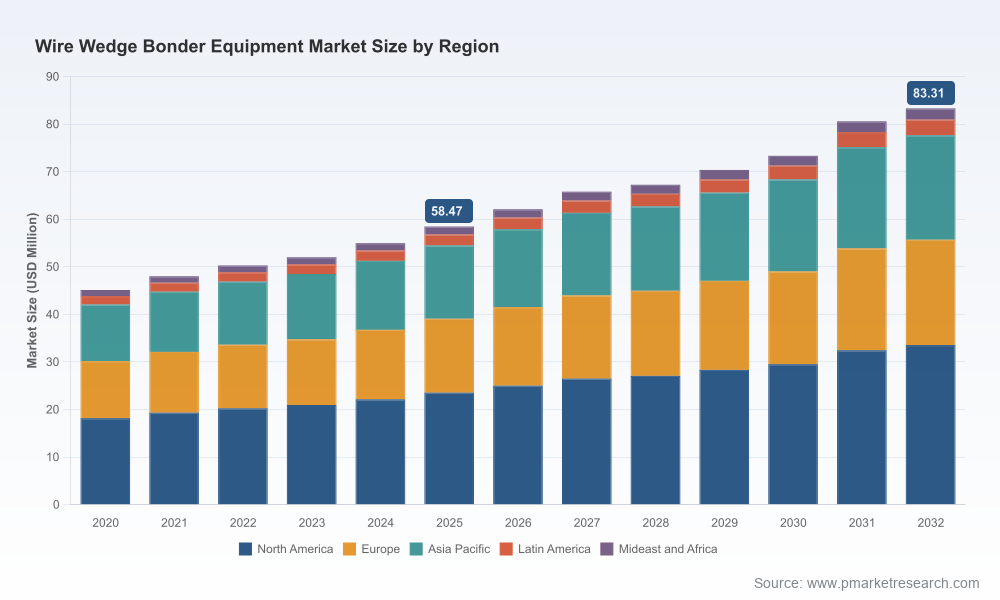

Note: In keeping with our “preview” principle, this announcement highlights strategic conclusions and market dynamics. Detailed segmentation and numeric breakdowns for regions, application splits and individual product segments are reserved for the full report and the accompanying datasets on PW Consulting’s report page.

Final assessment — why 2026 is a strategic inflection point

The combination of a steadily expanding market base, technology shifts toward non‑contact and AI‑assisted processes, and heightened regulatory scrutiny creates a window in 2026 where forward‑looking buyers can lock in durable advantages. Whether the priority is driving cost per singulation down, enabling new package types, or de‑risking the supply chain, decisions taken this year will shape manufacturing flexibility and unit economics for the remainder of the decade.

PW Consulting’s Worldwide Automatic Wafer Dicing Saw Market report equips executives with the analytic tools and strategic recommendations necessary to convert that window into measurable competitive advantage. For access to the full dataset, vendor matrices and procurement playbooks, please refer to the report landing page for licensing and enquiry options.

For detailed analysis of this topic, please visit the official page:Worldwide Automatic Wafer Dicing Saw Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com