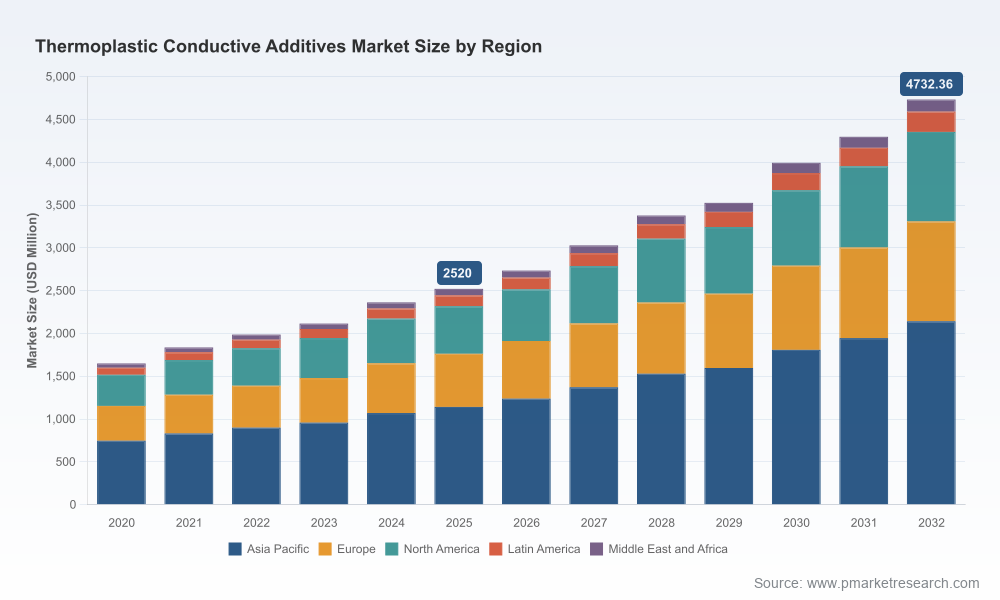

PW Consulting: Thermoplastic Conductive Additives Market Set to Surge at a 9.42% CAGR Through 2032

Other |

2026-07-02 12:47:39

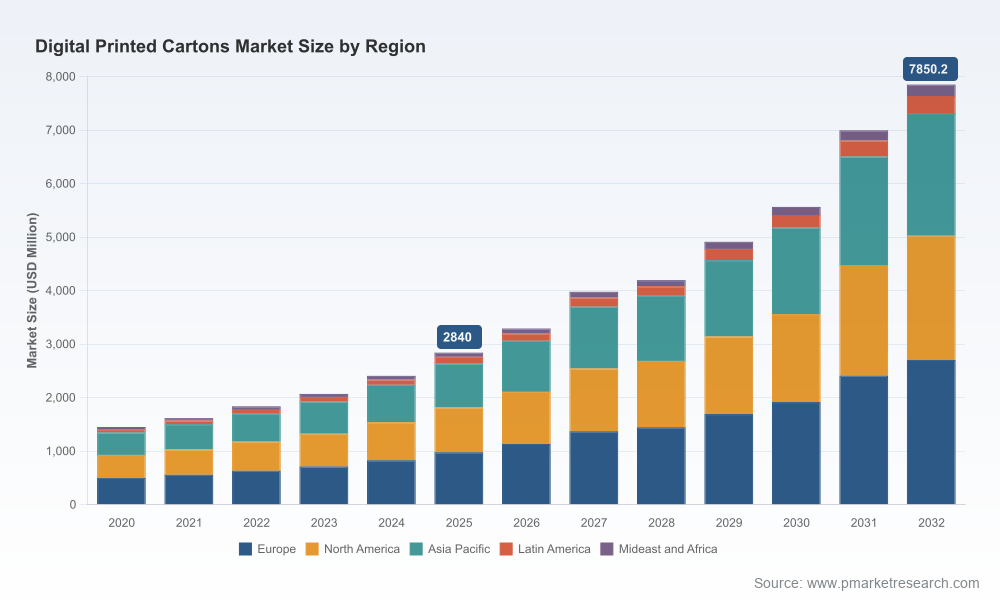

PW Consulting’s latest market intelligence on the Worldwide Digital Printed Cartons market is positioned as an operational playbook for executives making critical 2026 investment, sourcing, and M&A decisions. Using 2025 as a calibrated base year, our analysis traces market dynamics over 2020–2025 and projects the landscape through 2032. The market expanded rapidly in the past five years — reaching approximately USD 2,840.0 Million (revenue unit: Million USD) in 2025 — and is forecast to accelerate in the 2026–2032 window at a compound annual growth rate (CAGR) of 15.63%. Under our central scenario the market continues its multi-year expansion, reflecting converging forces of e-commerce personalization, sustainability regulation, and technology-led conversion economics.

Worldwide Digital Printed Cartons Market

Timing: 2026 is a watershed year in which digital printing moves from a differentiator to a core production capability for many brand owners and converters. Short-run economics, faster time-to-market and variable-data printing are reducing the friction around SKU proliferation and localized campaigns.

Worldwide Digital Printed Cartons Market

Regulatory pressure: Europe’s move to require all packaging to be recyclable by 2030, together with expanding Extended Producer Responsibility (EPR) schemes in multiple jurisdictions, is creating a structural tailwind for digitally printed paperboard solutions that enable mono-material construction and reduced reliance on multi-layer laminates.

Worldwide Digital Printed Cartons Market

Supply-side risk and opportunity: Volatility in recovered fiber and pulp prices and continued substrate lightweighting create both margin pressure and product innovation opportunities. Firms that combine digital print with material engineering (e.g., barrier coatings, mono-material barriers) will outperform on cost and compliance metrics.

Market structure: Concentration metrics in our study show a market that is neither atomized nor tightly consolidated — leaders are influential, but specialist players and regional converters retain meaningful share. That mix creates attractive niches for M&A and strategic partnerships.

This study is intentionally designed to be actionable. Beyond headline sizing and growth rates, the report contains:

Proprietary market model (2020–2032) with scenario-driven demand curves and sensitivity levers for price, substrate cost, and adoption rates.

Commercially oriented go-to-market playbooks for brand owners, converters, and equipment suppliers, including SKU rationalization frameworks and channel segmentation templates.

TCO and ROI calculators for greenfield digital lines, retrofit options, and hybrid workflows (digital + conventional), keyed to CapEx and Opex assumptions.

Supplier and technology assessment matrix — digital presses, ink systems, pre- and post-press converters — with vendor shortlists and procurement negotiation checklists.

Regulatory compliance mapping and EPR impact scenarios by jurisdiction, plus recommended product architecture changes to meet 2030 recyclability requirements.

M&A and partnership playbooks: target archetypes, valuation multiples, integration risks, and a watchlist of strategic-fit converters and IP owners.

Operational blueprints: pilot-to-scale templates, quality control KPIs, and workforce skilling plans for digital print adoption.

Benchmarking dashboards and a companion Excel model (gated) with granular inputs for unit economics, break-even analyses, and scenario outputs.

Note: The public preview above is comprehensive in context and methodology. Granular regional and end-use splits, named-case benchmarking tables and the full financial models are intentionally gated and available on the PW Consulting report landing page to support proprietary client use.

The transition to digitally printed cartons is being shaped by a mix of global integrators, specialized cartonmakers, and nimble digital-native converters. Key strategic archetypes represented among top players include full-system paperboard integrators, high-volume converters able to scale hybrid production, and boutique short-run specialists focused on speed and customization. Prominent companies and their strategic postures we profile in the report include:

Smurfit Westrock (Ireland / United States) — A global paper-based packaging leader that leverages broad converting footprint and digital printing capability to serve retail and consumer goods markets. Strategic emphasis: short-run customization at scale with sustainability credentials. (https://www.smurfitwestrock.com)

Graphic Packaging International (United States) — A major folding carton producer with deep converting capability and focus on food & beverage pack formats. Strategic emphasis: marrying high-volume converting with sustainable paperboard solutions. (https://www.graphicpkg.com)

Mayr-Melnhof Karton AG (MM Group) (Austria) — A European leader in cartonboard and folding cartons with premium print quality for regulated sectors. Strategic emphasis: pharma and luxury-grade digitally printed cartons with barrier and print quality performance. (https://www.mm-group.com)

DS Smith Plc (United Kingdom) — Specialist in retail and e-commerce packaging with a strong circular-economy narrative. Strategic emphasis: bespoke short runs and mono-material solutions for online fulfilment. (https://www.dssmith.com)

Amcor plc (Switzerland) — A diversified packaging supplier deploying digital print across multiple substrate families. Strategic emphasis: integrated hybrid solutions for cross-category brand portfolios. (https://www.amcor.com)

CCL Industries Inc. (Canada) — Focused on high-impact decorative and functional printed cartons, leveraging label-print heritage to deliver premium aesthetics. Strategic emphasis: value-added printing and embellishment. (https://www.cclind.com)

THIMM Group (Germany) — A specialist in digitally printed cartons and displays, strong in retail and point-of-sale applications. Strategic emphasis: advanced digital printing for retail activation. (https://www.thimm.com)

Stora Enso Oyj (Finland) — A renewable materials company embedding digital print into sustainable paperboard solutions. Strategic emphasis: recyclability and fiber-based innovation. (https://www.storaenso.com)

Mondi Group (United Kingdom) — Offers customizable paper-based solutions with a sustainability-first positioning. Strategic emphasis: fiber-based materials and custom print pathways. (https://www.mondigroup.com)

ePac Holdings, LLC (United States) — A digital-native converter focused on short-run, high-quality digitally printed cartons for agile brands. Strategic emphasis: speed-to-market and low-minimum runs. (https://www.epacflexibles.com)

Collectively, these players illustrate three near-term strategic moves that will define winners in 2026: (1) integrating digital printing into sustainable product architectures, (2) optimizing hybrid production economics, and (3) establishing localized short-run capacity for time-sensitive brand activations. Our concentration analysis shows top players hold meaningful influence without fully capturing the market — creating room for focused entrants and consolidation plays.

WEPACK 2026 showcased live digital production lines and end-to-end demonstrations, underscoring rapid equipment maturation and the lowering of technical barriers to adoption. Visibility into live runs shortens adoption cycles for buyers evaluating CapEx.

Technology adoptions such as the integration of Xeikon presses into existing folding carton workflows (reported 2025) highlight a pragmatic route for converters: retrofit to gain digital capability while preserving legacy volumes.

New facilities with digital-first intent (e.g., a high-capacity folding carton plant opened in 2025 serving pharma and healthcare) signal supplier confidence in regulated, high-margin end uses where print quality and traceability command premiums.

Revise capital plans to include pilot digital lines and hybrid retrofit projects this year; use phased investments that preserve optionality across substrate and ink chemistries.

Prioritize product architecture reviews to convert to mono-material, recyclable constructions where feasible. Regulatory timelines mean product redesigns commissioned in 2026 will need to be production-ready before 2030.

Hedge material risk via strategic fiber contracts and regional sourcing diversification; factor substrate price volatility into TCO models rather than relying on fixed-cost assumptions.

Evaluate M&A targets among short-run digital converters and specialist embellishment houses to quickly acquire capability and client relationships, using the report’s deal-sizing templates and integration checklists.

Operationalize digital value by piloting variable-data campaigns with lead customers to quantify margin uplift, inventory savings, and promotional effectiveness.

This article follows a “trailer” principle — it demonstrates the depth and rigor of PW Consulting’s analysis while intentionally withholding the granular segmentation tables, country-level regulatory mappings, and the full financial models that underpin our conclusions. The gated report includes exhaustive region-and-end-use breakdowns, technology-specific unit economics, company benchmarking by revenue and margin, and an editable Excel model to stress-test scenarios for board-level presentations.

For procurement teams, corporate strategists, and investors preparing 2026 budgets, the full report provides the transaction-ready inputs and playbooks required to convert insight into action. Visit the PW Consulting report landing page to download the complete study and companion tools.

Digital printing of folding cartons has moved beyond proof-of-concept. By combining the market’s strong growth trajectory (2020–2025 expansion into 2026 and beyond at a projected CAGR of 15.63%) with intensifying regulatory and commercial pressures, 2026 will reward companies that act decisively on capability, materials, and commercial models. PW Consulting’s report is structured to be your decision support engine for that pivot: rigorous, actionable, and calibrated for execution.

For detailed analysis of this topic, please visit the official page:Worldwide Digital Printed Cartons Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com