Worldwide Paper Release Liner Market — Strategic Outlook for 2026 Decisions

Executive trailer: Why 2026 is a pivot year for paper release liner strategies

As companies reposition for a post‑pandemic, sustainability‑driven supply chain environment, the paper release liner market is evolving from a commoditized input into a strategic lever. PW Consulting’s Worldwide Paper Release Liner Market report (base year 2025; historical 2020–2025; forecast 2026–2032) consolidates primary research, proprietary cost models and scenario stress‑tests to help executives convert market visibility into decisive action in 2026.

Worldwide Paper Release Liner Market

The market reached approximately USD 9.26 billion in 2025 and our modelling shows a continued upward trajectory through the forecast horizon, supported by a 2026–2032 CAGR of 4.2%. That long‑run expansion masks near‑term volatility and material‑driven margin pressure — dynamics that make 2026 a year to move from passive monitoring to proactive repositioning.

Worldwide Paper Release Liner Market

What this article gives you — and what we intentionally hold back

Below we surface the macro drivers, competitive moves and regulatory levers that will determine winners in 2026. To preserve the “trailer” quality of this brief — and to invite readers to the full dataset and segment‑level forecasts — we deliberately omit granular regional and application breakdowns. The full report contains the complete segmentation tables, year‑by‑year subsegment forecasts, Excel models and supplier scorecards used to underpin the strategic recommendations summarized here.

Worldwide Paper Release Liner Market

Macro picture: growth with pockets of cyclicality

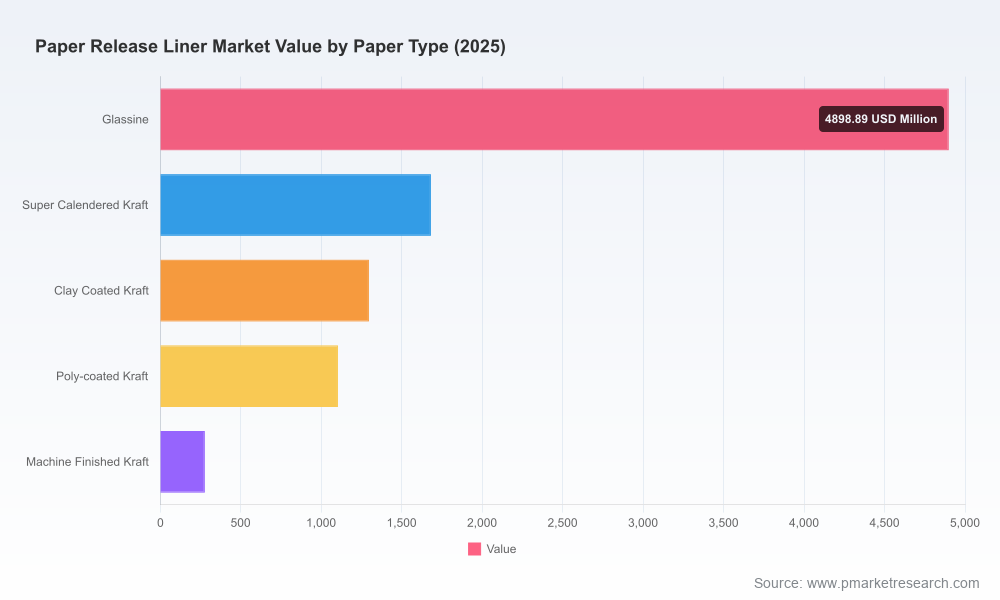

- Market scale and trajectory: From a multi‑billion dollar base in 2025, structural demand for paper release liners expands through 2032, reflecting steady growth in labeling, hygiene and industrial adhesives applications and selective premiumization toward high‑performance glassine and specialty kraft grades.

- Cyclic and investment effects: Our forecast captures short‑term fluctuations driven by capacity cycles, retrofit CapEx and episodic demand from adjacent industries (e.g., tapes, medical, and electronics). These create windows of constrained supply that materially affect pricing and contract terms.

- Consolidation profile: The market shows moderate concentration — the top three and top five players control a meaningful share, but not an entrenched oligopoly. This creates an environment where well‑timed M&A or capacity plays can substantially shift competitive positioning.

Key demand and supply dynamics for 2026 strategy

- Sustainability is not optional: Regulatory mandates (for example, EU recycled‑content requirements) and producer responsibility schemes in major markets materially change procurement specifications and cost allocation models. Buyers and producers must map compliance pathways into their 2026 sourcing strategies.

- Raw material volatility: Input cost pressure — exemplified by bleached kraft pulp price baselines and mechanical pulp/chemical pulp spreads — will be a key determinant of margins. Our price‑sensitivity module simulates supplier pass‑through and margin scenarios under multiple pulp and energy price paths.

- Performance premium: End users increasingly demand improved peel control, low‑migration silicones and recyclability. These feature sets justify premium pricing but require targeted R&D and manufacturing tolerances.

- Regulatory and food‑contact constraints: Silicone‑coated liners used in food and medical applications must meet strict regulatory frameworks; compliance is a gating factor for market access in certain segments.

Competitive landscape: what incumbents are doing — and what that implies for 2026

The sector combines global leaders with specialist regional producers. Our competitive review evaluates strategy across five vectors: product innovation, sustainability credentials, cost position, channel &alogistics, and M&A posture.

- UPM Raflatac (Finland) — A global leader with clear emphasis on recyclable paper liners and peel performance. Recent product launches point to a playbook focused on premium sustainable solutions for label applications. For buyers, UPM’s roadmap signals rising standards for recyclable liners; for competitors, it raises the innovation bar.

- Mondi Group (Austria) — Systematic moves toward certified recycled content and line‑level sustainability credentials demonstrate vertical integration of compliance. Its ISCC PLUS certification reflects how certification can be used as a commercial differentiator in procurement conversations.

- Sappi (South Africa) — Strong in glassine and coated kraft segments with a visible focus on low‑migration silicone coatings showcased at recent trade shows. Sappi’s activity highlights the intersection of premium technical performance and trade‑visibility as pathways to win share among brand owners.

- Nippon Paper Industries & Lintec (Japan) — These players emphasize specialized, lightweight glassine products and electronics/automotive niche applications, underlining the importance of product engineering and application alignment in defending high‑margin niches.

- Ahlstrom‑Munksjö, Delfort, Lecta, Fedrigoni — European and specialty paper houses focusing on silicone release, recyclability and premium grades for labels and hygiene applications. Their strategy mix shows that regional expertise and brand partnerships — not just scale — determine access to high‑value demand pockets.

- Verso Corporation (USA) — A North American supplier with a regional channel advantage for pressure‑sensitive applications; their role underscores the relevance of logistic footprint and service models in markets where lead times and local compliance matter.

Recent corporate moves reinforce these strategic themes: UPM Raflatac’s September 2024 recyclable liner launch, Mondi’s ISCC PLUS certification in May 2024, and Sappi’s product showcase in late 2023 collectively illustrate the race for certified, high‑performance liners. Our competitive heatmaps identify which players are likely to be acquisition targets, price‑leaders or technology partners through 2026.

Operational levers and what to do in 2026

Based on our cost‑and‑capability modelling, firms should prioritize a three‑track program in 2026:

- Procurement transformation: Move from commodity tenders to total cost of ownership (TCO) procurement. Include recycled‑content premiums, EPR cost exposure, and regulatory compliance costs in bid evaluations.

- Strategic product road‑mapping: Accelerate qualification of high‑value liners (e.g., low‑migration silicones, lightweight glassine) with CPG and medical customers. Time R&D and customer trials to capture premium contracts as regulation tightens.

- Capacity and footprint optimization: Use the report’s regional cost curves and logistics matrices to decide whether to retrofit existing machines for recycled content or to secure brownfield capacity via partnerships/M&A — particularly where top‑tier suppliers control local access.

What’s inside the full PW Consulting Worldwide Paper Release Liner report

The full publication is structured to be directly actionable for 2026 planning cycles and includes:

- Comprehensive market sizing and top‑down/bottom‑up reconciliations (2020–2032)

- Segment and subsegment forecasts by paper type, application and region (year‑by‑year), accompanied by interactive Excel models

- Supplier scorecards and a strategic M&A shortlist with financial proxies

- Raw material sensitivity and margin stress‑tests (pulp, energy, coatings)

- Regulatory impact modelling (including recycled‑content mandates and EPR implications on cost allocation)

- Procurement playbook: RFx templates, contract terms, and risk hedging strategies

- R&D and capex decision framework to evaluate retrofits vs. greenfield investments

- A scenario atlas that translates macro scenarios into procurement, pricing and capacity responses

Practical use cases: five decisions the report helps you make in 2026

- Supplier selection under new recycled‑content rules: Identify suppliers that meet both performance and compliance thresholds, quantify premiums and model contractual renegotiations.

- M&A target screening: Rapid shortlist of regional players and specialty mills that improve your route to market or add differentiated product capability.

- Pricing strategy: Calibrate pass‑through clauses and indexation mechanisms tied to pulp and glassine indices to protect margins.

- CapEx prioritization: Decide whether to retrofit silicone lines, invest in recycled pulps, or pursue co‑production agreements based on NPV and payback modelling.

- Regulatory compliance and labeling: Map product portfolios to food‑contact and medical compliance frameworks; prioritize certifications that unlock high‑value customers.

FAQ highlights (targeted, operational answers)

- Which certifications matter? Certification schemes for recycled content and circular inputs, plus food‑contact compliance codes, are decisive. For example, silicone‑coated release papers intended for food contact must be validated against applicable food‑contact regulations — compliance is non‑negotiable for entry into certain segments.

- How should procurement reflect EPR schemes? Include scenario lines for producer responsibility costs and potential collection fees in your TCO model; in markets with advanced EPR, these can materially change supplier economics.

- How to hedge raw material risk? Use a combination of index‑linked contracts, multi‑sourcing strategies and strategic inventory to buffer pulp price spikes and paper grade shortages.

Final note — the strategic value for 2026

2026 is the year to convert knowledge into competitive advantage. With the market growing on a mid‑single digit trajectory and regulatory and material pressures rising, companies that integrate sustainability compliance, product performance and procurement sophistication into a unified strategy will capture the higher‑margin growth segments. PW Consulting’s report provides the actionable intelligence — from calibrated cost models to supplier heatmaps — to execute that pivot. For teams preparing budgets, R&D roadmaps, or M&A pipelines in 2026, this report functions as both a playbook and a risk register.

For the full datasets, supplier scorecards and proprietary Excel models referenced above, access to the complete Worldwide Paper Release Liner Market report is required. PW Consulting clients and authorized stakeholders can obtain the complete deliverable through our client portal.

For detailed analysis of this topic, please visit the official page:Worldwide Paper Release Liner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com