Smarter Planning, Safer Execution: Why Availability Forecasting Is Now Essential

Other |

2026-04-07 07:04:04

As global vehicle platforms evolve, the Hill-Start Assist (HSA) market has quietly become a strategic node where safety regulation, electronic braking evolution, and sensor-driven ADAS convergence intersect. PW Consulting’s latest market study—anchored on a 2025 base year and projecting through 2032—shows a market that expanded from USD 3,450 Million in 2020 to USD 4,842.4 Million in 2025, with a forecasted compound annual growth rate (CAGR) of 7.2% across 2026–2032, reaching an estimated USD 7,878.16 Million by 2032. This trajectory represents a sustained growth opportunity for OEMs, Tier‑1 suppliers, and fleets, but it also creates tactical choices that will define winners and laggards through the next product cycle.

Worldwide Hill-Start Assist Systems Market

Market momentum and timing: The mid‑decade inflection reflected in our model—moving from USD 4,842.4 Million in 2025 to USD 5,233.56 Million in 2026—signals that near‑term investments in electronic braking integration, sensor fusion, and EPB-enabled hill‑hold capabilities will capture disproportionate share as vehicles increasingly bundle HSA with wider ADAS suites.

Worldwide Hill-Start Assist Systems Market

Competitive concentration: The market exhibits material concentration at the top end (CR3 ~58.4%; CR5 ~76.2%), indicating that strategic moves by dominant Tier‑1 players and selective consolidation will have outsized influence on supplier selection and OEM roadmaps.

Worldwide Hill-Start Assist Systems Market

Regulatory and safety tailwinds: Functional safety rules (ISO 26262), FMVSS brake standards, and evolving recognition of hill‑hold features in vehicle safety ratings (e.g., Euro NCAP, NHTSA) create both compliance mandates and competitive differentiation. Firms that embed verification-and-validation disciplines into their development cycles will avoid rework and market delays.

Risk vs. opportunity for fleet and commercial segments: Commercial vehicle adoption pathways for HSA (both hydraulic and electronic implementations) differ from passenger cars; operators and specifiers must weigh uptime, maintainability, and freeze‑resilience in cold climates, as highlighted by historical technical bulletins around valve freezing.

Prioritize EPB and electronic integration: With vehicles migrating toward electrified and software‑defined architectures, leaning into electronic parking brake (EPB) integration and ECUs that can be updated over-the-air will shorten feature‑delivery cycles and enable bundled ADAS value propositions.

Align product roadmaps with safety certification from Day‑1: Embed ISO 26262 processes and FMVSS-compliant test matrices in early development to avoid late-stage redesigns. This is a low-cost hedge given the market’s growth profile and penalties for non-compliance.

Use supplier concentration to negotiate value, not just price: The CR metrics suggest a buyer‑market nuance—while a few suppliers control share, their integrated capabilities (sensors, braking mechatronics, software stacks) deliver gating functionality. Negotiate IP-sharing, joint validation, and performance-based contracts rather than commodity pricing alone.

Targeted inorganic options: For companies seeking scale or capability fast, selective M&A focused on sensor fusion, inertial measurement expertise, or EPB algorithm IP will be higher-return plays than broad portfolio acquisitions. Our study identifies archetypal targets and valuation bands (full details in the report).

Design for serviceability in commercial fleets: Address historic issues (e.g., freeze-related valve faults) with system layout, heater or plumbing revisions, and diagnostic intelligence to minimize downtime—particularly relevant to heavy-duty OEMs and vocational fleets.

The HSA market sits within the broader braking and ADAS ecosystems. A cohort of global Tier‑1s and component specialists shape product direction through integration depth, software quality, and OEM partnerships. Key competitive observations from our vendor analysis include:

Robert Bosch GmbH (Gerlingen, Germany) — Bosch offers Hill Hold functions closely integrated with ESP and supplies a broad sensor portfolio that includes inertial and brake pressure sensors. Their approach emphasizes system-level validation and multi‑function ECUs, positioning them well where OEMs prefer consolidated suppliers for vehicle stability and ADAS functions.

Continental AG (Hanover, Germany) — Continental’s strength lies in electronic braking portfolios and ADAS integration, with hill‑start functionality implemented via rear‑axle brake intervention or EPB integration. They are a strategic partner for OEMs seeking holistic braking and lateral dynamics solutions.

ZF Friedrichshafen AG (Friedrichshafen, Germany) — ZF’s capability set in electronic braking and control systems makes them a natural integrator for passenger and commercial platforms, especially when ESC and EPB are bundled into a single subsystem.

Knorr‑Bremse and Bendix — With deep roots in commercial vehicle braking, Knorr‑Bremse (Munich) and its North American arm Bendix (Troy, Michigan) focus on EBS and hill‑start aids for heavy vehicles. Recent product integrations (e.g., Bendix Intellipark being made available on Class 8 platforms) exemplify the sector’s move toward integrated park‑to‑drive assistance for commercial fleets.

Tier‑1s from Asia — Aisin, Hyundai Mobis, BWI Group, Denso, and Murata provide a mix of braking hardware, sensors, and control electronics. Their global OEM relationships and local manufacturing advantages make them essential partners for regional production ramps.

HELLA — Specializes in electromechanical parking brakes with adaptive hill‑start functions, delivering jolt-free starts and wear-aware controls that address customer-perceived refinement.

Recent product activity underscores consolidation of functionality: Peterbilt’s December 2025 availability of Bendix Intellipark for medium‑ and heavy‑duty trucks is a case in point—manufacturers are standardizing on EPB‑capable units that provide hill‑start and rollaway mitigation as part of the base spec. Earlier vehicle integrations, such as city EV models adopting hill assist, demonstrate OEM willingness to include HSA in compact and urban vehicles when it complements overall safety positioning.

Functional safety (ISO 26262): ASIL-driven engineering is no longer optional for any HSA implementation that interacts with braking. Design teams must integrate hazard analysis, safety requirements, and verification plans into product backlogs from the outset.

FMVSS compliance: EPB and hydraulic systems intended to provide hill‑hold functionality must meet holding‑force and fail‑safe criteria. Test planning should reflect both normative requirements and worst‑case field scenarios.

Safety rating incentives: With Euro NCAP and NHTSA placing greater emphasis on ADAS availability, OEMs can leverage HSA as part of safety‑feature bundles that improve market positioning—an important marketing angle for 2026 model launches.

Field learnings: Technical service bulletins—such as those addressing valve freeze incidents—remind suppliers to combine design robustness with service diagnostics and in-field revisions rather than rely solely on warranty remedies.

Our full study is designed for operators and strategists who must convert market insight into action. Deliverables include:

A reconciled market‑sizing model (historical 2020–2025 and forecast 2026–2032) and scenario testing across macro and vehicle adoption pathways.

Supplier benchmarking with capability matrices (technology, software, sensor, and service strengths), go‑to‑market archetypes, and negotiation playbooks.

Regulatory impact assessments and a compliance checklist mapped to product development stages and test protocols.

Deal flow and M&A candidate profiles for capability or geographic expansion, with valuation frameworks and integration risk scoring.

Implementation blueprints for OEMs and fleets covering architecture choices (hydraulic vs electronic EPB), verification schedules, and cost‑to‑implement sensitivities.

Field failure case studies and mitigations—practical revisions that reduce recall risk and improve uptime for fleets.

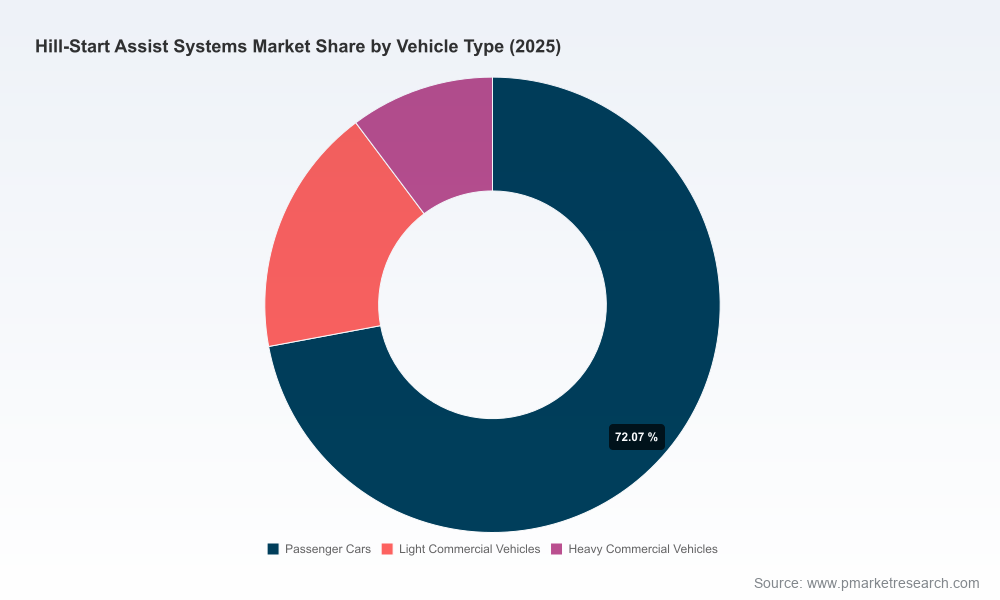

To preserve competitive value and to adhere to our "trailer" approach, this public release intentionally highlights strategic findings without disclosing the granular segmentation tables, regional shares, or application‑level dollar splits contained in the full report—these are available in the full intelligence package.

CEOs and corporate strategy: Use the growth trajectory and concentration metrics to prioritize inorganic versus organic capability builds. Our model helps size the investment to achieve meaningful upside within three product cycles.

Product and R&D heads: Rebase roadmaps around EPB integration, ISO 26262 artifacts, and sensor fusion strategies detailed in the study; schedule validation labs to avoid late-stage compliance gaps.

Procurement and supply chain: Execute tiering strategies that reduce single‑source exposure for critical sensors while negotiating long‑term performance contracts with leading braking systems integrators.

Fleet operators: Prioritize spec items that reduce operational risk—diagnostics, freeze-resistant plumbing, and remote fault telemetry—that lower total cost of ownership in the first five years.

In an industry where a handful of suppliers shape product direction, and where regulation increases the penalty for failure, the strategic choices made in 2026 will determine who captures the highest-margin growth as the market approaches USD 7.9 Billion by 2032. PW Consulting’s full Worldwide Hill‑Start Assist Systems Market report equips leaders with the models, playbooks, and competitive maps required to make those choices with confidence.

For the full dataset, vendor scorecards, and region‑and‑vehicle‑type segmentation tables, access the complete report through PW Consulting’s research portal.

For detailed analysis of this topic, please visit the official page:Worldwide Hill-Start Assist Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com