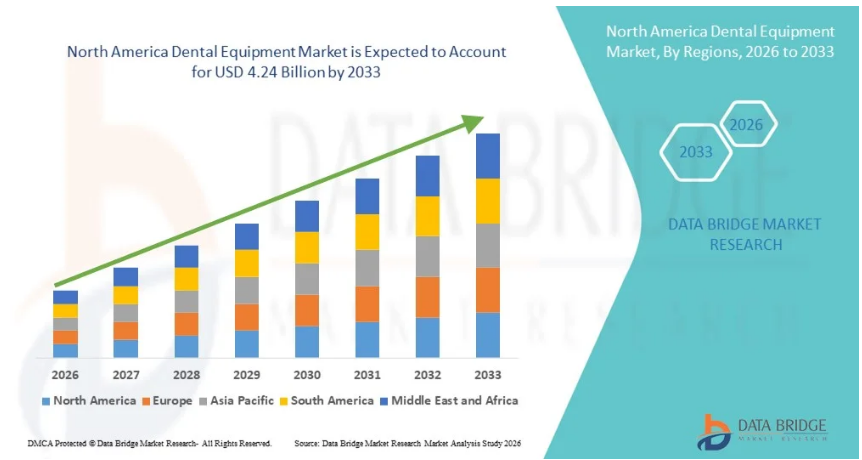

Why Is Advanced Dental Care Infrastructure Driving the North America Dental Equipment Market?

Networking |

2026-03-13 05:47:18

PW Consulting’s latest market study on the Worldwide Inflatable Above Ground Pool Market provides a focused, practitioner-ready view for commercial leaders planning 2026 strategy. The market grew steadily through the early 2020s and reached a global revenue base of approximately USD 1,580 Million in our 2025 base year. Over the 2026–2032 forecast horizon the market is projected to expand at a compound annual growth rate (CAGR) of 6.18%, reaching just over USD 2.4 Billion by 2032. These headline dynamics set the frame for a competitive environment in which product safety, channel sophistication, input-cost management, and selective innovation will determine winners and losers.

Worldwide Inflatable Above Ground Pool Market

Demand drivers remain multi-faceted. Consumer preferences for backyard leisure, short-cycle renovation and rental markets, and continued appetite for accessible, family-oriented water recreation support steady unit demand. Simultaneously, premium adult-oriented and design-led pools are emerging as higher-margin niches. On the supply side, raw-material volatility—particularly in PVC and related polymers—continues to shape manufacturers’ cost bases and negotiation leverage. In late 2025 we observed downward pressure on PVC resin prices, creating a short-term buyer’s market; however, structural volatility persists for PVC, polyethylene and steel inputs, which requires systematic procurement risk management in 2026.

Worldwide Inflatable Above Ground Pool Market

Regulatory attention and product-safety incidents have materially altered competitive calculus. Recent recalls affecting major OEMs have elevated compliance cost expectations and urged fresh investments in product redesign, testing and labeling. The net effect: cost of goods sold (COGS) models must now explicitly factor in higher compliance and warranty provisions, and go-to-market timelines must build in additional certification gates.

Worldwide Inflatable Above Ground Pool Market

The market is moderately concentrated. The top three and top five vendors collectively account for a meaningful portion of global sales, reflecting the presence of scale players with integrated manufacturing, large distribution networks, and established retail partnerships. This concentration favors companies that can leverage scale for raw-material procurement, global logistics and multi-channel distribution, while still permitting differentiated entrants to capture niche, design- or feature-led segments.

Key industry participants include established OEMs and vertically integrated manufacturers as well as brand-driven designers and global retailers. Representative firms examined in the report include firms with long-standing global footprints and those focused on design-led premium offerings. Each of these players has responded differently to 2025–2026 events, from product recalls and catalog refreshes to production ramp-ups.

Regulatory and safety incidents in 2025 prompted recalls that affected multiple major manufacturers. These events amplified consumer safety scrutiny, increased legal and remediation costs, and accelerated retailer and regulator requirements for testing and traceability. For strategic leaders, the immediate implications are clear:

Input-cost management is a central lever for 2026. While PVC resin softened toward the end of 2025—offering temporary margin relief—the broader picture is one of cyclicality and exposure to energy and petrochemical markets. The report offers supply-side playbooks including:

Distribution is evolving. Online retail continues to grow in importance as consumers seek convenience, price comparison and home-delivery installation services. At the same time, mass retailers and specialty stores remain vital for discovery and impulse purchases. The optimal 2026 channel strategy differs by product tier: premium and specialty models benefit from immersive retail experiences and targeted direct-to-consumer channels, while mass-market pools require robust partnerships with national retailers and e-tailers.

Our analysis recommends a channel mix that balances reach with margin capture. Practical initiatives include exclusive model runs for key retail partners, enhanced product pages and kit-bundling strategies on e-commerce platforms, and flexible fulfillment options (ship-from-store, direct ship) to improve service levels during peak seasons.

Innovation is shifting from purely ornamental features to functional enhancements that address safety, longevity and user experience. Areas of highest strategic value include durable materials (drop-stitch and reinforced PVC), integrated filtration and sanitization modules, modular add-ons for lifestyle use (spas, seating), and design-led features for adult consumers. Our product benchmarking identifies which features materially move willingness-to-pay and which are perceived as commoditized by buyers.

Compliance is no longer a checkbox. The intersection of CPSIA, ASTM standards, substance restrictions and heightened regulator vigilance means manufacturers and distributors must embed compliance into product lifecycles—from concept through end-of-life. The report provides a step-by-step compliance playbook: mandatory testing matrices, supplier certification templates, and a prioritized investment plan for testing labs, third-party audits and documentation systems.

To make these recommendations actionable, the PW Consulting report contains an array of decision-grade tools: financial models with scenario filters (input-cost, recall liability, pricing elasticity), a supplier scorecard and risk heat map, SKU-level margin analyses, channel ROI calculators, and a regulatory compliance checklist mapped to jurisdictions. We intentionally withhold certain micro-segmentation data in this briefing to preserve the value of the full dataset—our clients rely on the granular regional, product-type and channel splits to size investments and quantify ROI precisely.

Executives should frame 2026 planning discussions around three themes: protection (mitigating compliance and supply-chain risks), growth (capturing higher-margin segments and channel efficiencies), and optionality (structuring contracts and investments to be reversible if raw-material cycles or regulatory pressure intensify). The report supplies slide-ready executive summaries, one-page action plans for CFOs and supply chain leaders, and a prioritized list of near-term initiatives with expected payback timelines.

The inflatable above-ground pool market is maturing into a market where disciplined operational execution and proactive risk management will outperform simplistic volume plays. With a clear growth trajectory to 2032 and an industry structure that rewards scale and compliance sophistication, 2026 is the year to translate strategic intent into operational commitments. PW Consulting’s comprehensive report delivers the empirical foundation and practical tools leaders need to make those commitments defensible and value-accretive.

For executives and investors preparing 2026 budgets and capital plans, access to the full report is essential to drill into product-level economics, regional strategies, and scenario-modeled outcomes. Contact PW Consulting to obtain the complete dataset, supplier matrices and the customizable decision models referenced in this briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Inflatable Above Ground Pool Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com