Worldwide Signature Verification Market: Strategic Imperatives for 2026

PW Consulting's latest Worldwide Signature Verification Market report (base year 2025) delivers a tactical playbook for executives who must make confident, compliance-aware decisions in 2026. Built for C-suite strategists, product leaders, and M&A teams, the report synthesizes market trajectory, regulatory dynamics, vendor positioning, and actionable go‑to‑market frameworks — while preserving the detailed segment-level intelligence behind a gated analysis.

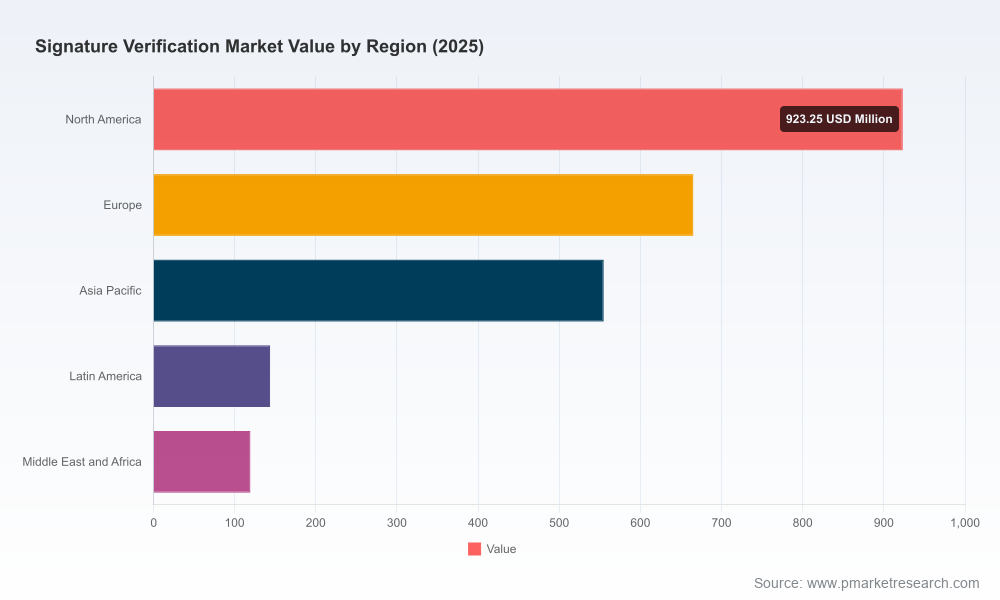

Worldwide Signature Verification Market

Data-driven market trajectory: the macro picture that should shape 2026 roadmaps

Adoption of signature verification technologies has entered a structurally high-growth phase. The market expanded from roughly USD 890.15 Million in 2020 to USD 2,405.96 Million in 2025. With compound annual growth of 22.01% from the base year, the market is projected to surpass USD 3,059.49 Million in 2026 and approach USD 9,684.03 Million by 2032 under our central scenario. That pace creates both scale opportunities and a narrowing window to build defensible capabilities before second‑wave entrants and incumbents intensify competition.

Worldwide Signature Verification Market

- Why the trajectory matters: a sustained >20% CAGR mandates that enterprise buyers embed signature verification into strategic architectures (identity, contract management, and fraud prevention) rather than treating it as an ancillary control.

- What it signals for vendors: sustained growth invites platform consolidation, accelerated product roadmaps for AI-driven verification, and vertical specialization for regulated industries.

Regulatory inflection points: compliance as the primary accelerant

Regulation is no longer a compliance footnote — it is the mechanical driver of procurement cycles. Europe’s eIDAS 2.0 regime and updated regulatory guidance in North America are increasing the technical and audit requirements for electronic signatures and identity verification. Similarly, finalized guidance around electronic records and signatures in clinical contexts tightens validation and audit trail expectations for life sciences and healthcare providers.

Worldwide Signature Verification Market

- Strategic implication for enterprises: procurement decisions must prioritize solutions that support qualified trust services, interoperable digital identity wallets, and auditable cryptographic bindings.

- Strategic implication for vendors: compliance-ready architectures (including PKI, tamper-evident audit trails, and identity wallet interoperability) are table stakes for large contracts and cross‑border deployments.

Technology landscape: AI, biometrics and software-first deployments

AI/ML-based pattern recognition and biometric analysis are reshaping verification accuracy and operational efficiency. Market adoption favours dynamic verification approaches — those that analyze biometric dynamics such as pressure, speed, and stroke order — combined with cloud-native, software-first delivery. Software-based verification models unlock scalability and continuous model improvement while hardware capture (signature pads and secure tokens) continues to persist where offline or transaction-level guarantees are required.

- Enterprise takeaway: adopt hybrid architectures that combine cloud verification services with on-premise capture and cryptographic signing for regulated or high-risk flows.

- Vendor takeaway: invest in model explainability, adversarial testing, and longitudinal model training to maintain detection performance as fraudsters adapt.

Competitive landscape: consolidation, portfolio expansion and new entrants

The competitive arena is a mix of global software platforms, specialized AI/biometrics vendors, legacy hardware providers, and fast-scaling identity incumbents. Recent industry moves underscore two concurrent trends: large platform players expanding vertically into identity and verification, and niche AI specialists raising capital to scale.

- Major cloud platforms and agreement specialists (e.g., DocuSign and Adobe) are deepening verification and identity services within broader agreement ecosystems to lock in enterprise workflows and capture higher wallet share.

- Identity-first firms and acquisition strategies (as seen with Entrust’s positioning and linked identity plays) are aligning multimodal identity proofs with signature verification to reduce account opening and transaction risk.

- AI-native companies (including Parascript, Mitek, Jumio, and specialist biometric providers) are pushing the frontier on realtime analytics, check/process automation, and mobile-first capture.

- Hardware and embedded vendors (for example, signature capture manufacturers and PKI specialists) remain strategically important where regulatory or forensic requirements mandate trusted capture devices.

Market concentration metrics suggest a competitive but not opaque landscape: the top three vendors control a meaningful minority share while the top five extend that position — a structure that favors both continued consolidation and differentiated specialization by vertical or technology approach.

Recent industry developments that matter for 2026 planning

- Portfolio expansions by leading digital signature and identity firms have accelerated the bundling of verification, identity, and agreement workflows — increasing the importance of API-first integration strategies for buyers.

- Significant private investment into AI-first identity platforms is catalyzing improved image and signature analytics capability, which will be a differentiator for mobile and remote-first use cases.

- Product launches that embed real‑time analytics into check and signature processing platforms indicate a near-term capability cycle focused on fraud prevention and straight‑through processing in financial services.

- Regulatory clarifications (e.g., clinical investigation guidance) are producing immediate procurement cycles in life sciences and healthcare, boosting demand for auditable, validated signature workflows.

What our report delivers — practical, board-ready assets

PW Consulting’s report is crafted as a decision-ready dossier rather than an academic exercise. It includes:

- Macro and scenario-based forecasts (2026–2032) with sensitivity testing for regulatory, economic, and technology adoption variables.

- A buyer’s guide and RFP template that translates compliance and functional requirements into weighted evaluation criteria for procurement teams.

- Vendor scorecards and strategic positioning maps that score vendors across technology maturity, deployment versatility, compliance readiness, and partnership ecosystems.

- Use-case playbooks with implementation blueprints for BFSI, healthcare, government, and high-volume transaction workflows, including integration patterns for identity wallets and document management platforms.

- ROI calculators and total cost of ownership templates that model on-premise vs. cloud deployment, capture hardware needs, and fraud reduction benefits.

- An M&A and partnership playbook highlighting acquisition targets, technology gaps, and integration risk mitigations for potential consolidators.

- Technical annexes including data collection standards, model validation checklists, and compliance mapping (e.g., eIDAS 2.0 and FDA guidance) to operationalize procurement requirements.

Strategic recommendations for 2026

- For enterprise buyers: prioritize solutions that combine strong identity binding, auditable signature metadata, and modular APIs. Shortlist vendors capable of delivering both regulatory attestations and continuous‑learning AI models.

- For vendors: pursue bundling strategies that align verification with agreement lifecycles while protecting interoperability. Invest in data partnerships to improve model robustness and in certified compliance artifacts to accelerate enterprise sales cycles.

- For investors and M&A teams: target mid‑market AI specialists and identity orchestration platforms that can be integrated into larger agreement ecosystems; the market structure rewards both scale and specialized vertical expertise.

- For regulators and standards bodies: provide clear technical profiles for qualified trust services and interoperability tests to reduce procurement friction and encourage cross-border adoption.

Why PW Consulting’s report is uniquely actionable

We combine rigorous market modeling with operation-focused deliverables. Rather than merely projecting growth, our work prescribes implementation pathways that align vendor capabilities, compliance constraints, and the pragmatic needs of enterprise IT and legal teams. The report’s original contributions include scenario-tested integration patterns, a validated vendor scoring methodology, and a prioritized set of investment opportunities mapped to near-term revenue pools.

Next steps — access core insights

This release is intentionally a strategic preview: it highlights the macro trajectory, competitive dynamics, and operational playbooks that should shape boardroom decisions in 2026, while the full report contains the granular segmentation, vendor-by-vendor benchmarks, and downloadable assessment tools required to act immediately. For teams that need to convert market momentum into measurable programs — procurement shortlists, pilot designs, or acquisition targets — the full PW Consulting report is the pragmatic next step.

Contact PW Consulting to request the full Worldwide Signature Verification Market report and obtain the proprietary templates, vendor scorecards, and scenario models that will inform your 2026 strategic plan.

For detailed analysis of this topic, please visit the official page:Worldwide Signature Verification Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com