Artificial Cochlea Market Size and Forecast Driven by Rising Prevalence of Hearing Disorders

Other |

2026-06-16 13:25:08

PW Consulting’s latest market study, "Worldwide High-performance IMU Market" (base year 2025), synthesizes seven years of historical performance with a seven-year forecast to 2032. At a macro level the market is projected to expand from an estimated USD 3,750 Million in 2025 to roughly USD 5,532 Million by 2032, reflecting a compound annual growth rate (CAGR) of approximately 5.72% over the forecast period. This briefing explains why that trajectory matters to corporate leaders, program managers, and investors making strategic choices in 2026 — and how our full report supplies the operational intelligence required to act with confidence.

Worldwide High-performance IMU Market

Timing of investment: the market’s steady mid-single-digit CAGR indicates a maturing but expanding opportunity where R&D, certification, and supply chain moves made in 2026 will determine competitive positions through the next procurement cycles.

Worldwide High-performance IMU Market

Risk allocation: regulatory constraints and export controls materially affect addressable markets; early compliance planning reduces go-to-market friction for high-value contracts.

Worldwide High-performance IMU Market

Technology selection: trade-offs between cost, size, power, and inertial performance (bias instability, scale-factor stability) are now decisive across defense, autonomy, and space applications.

M&A and partnership timing: consolidation is selective — the market shows meaningful share concentration among incumbents while leaving niches open for targeted acquisitions and specialized entrants.

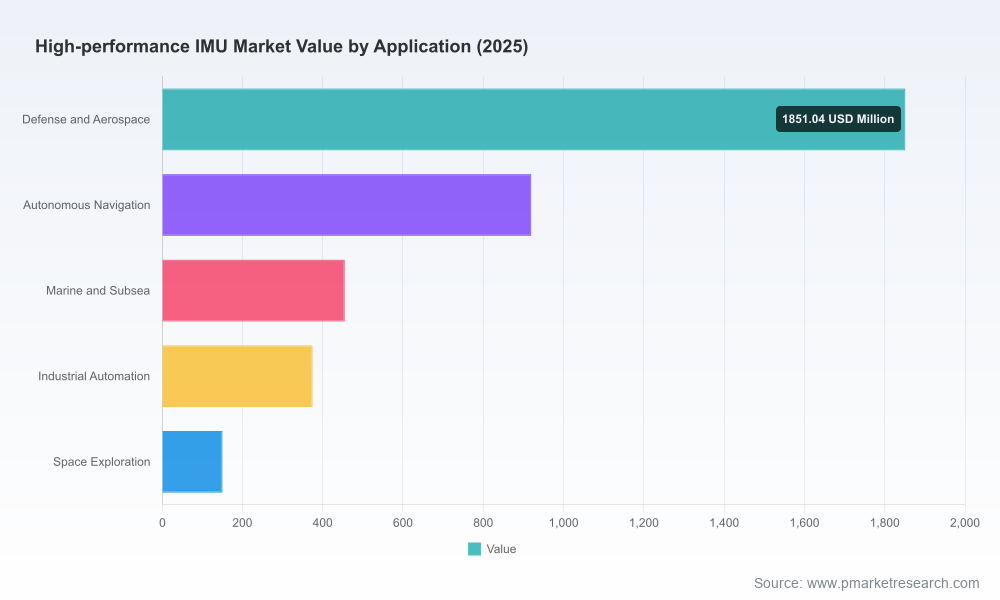

Demand drivers are multi-dimensional. Growth is being sustained by expanding autonomy programs (land, air, and maritime), continued defense modernization and space missions, and increased industrial use where high-accuracy motion sensing improves productivity and reliability.

Technological trajectories: MEMS performance improvements are closing the gap with legacy optical gyros in many tactical and industrial use cases. At the same time, fiber-optic and resonator-based solutions retain advantages in long-term stability for space and strategic applications. The result is a layered market in which performance per dollar is improving but absolute performance ceilings remain governed by fundamental sensor physics and packaging constraints.

Regulatory and standards pressure: export controls and munitions-list classifications (ITAR/USML; EAR/BIS controls) continue to shape supplier-customer pairings and procurement timelines. Parallel pressures to meet MIL-STD and rigorous environmental qualifications increase time-to-deploy and favor suppliers with established qualification pipelines.

Supply-chain economics: scale and production maturity matter. Manufacturers who have invested in high-volume, high-yield production can compete aggressively on cost while maintaining higher margins through value-added services (calibration, sensor fusion software, lifecycle support).

Performance envelope constraints: the dominant engineering challenge remains achieving low bias instability and stable scale factors in compact, low-SWaP packages that must withstand vibration, shock, and wide temperature ranges. These are not merely component issues: system-level calibration, thermal control, and algorithmic compensation are equally determinative.

Integration complexity: high-performance IMUs are increasingly packaged as part of broader navigation stacks; sensor fusion, GNSS denial resilience, and cybersecurity hardening are now essential disciplines, not afterthoughts.

Compliance and exportability: a bifurcated market exists between ITAR-restricted military-grade variants and ITAR-free commercial/industrial product lines. Buyers and suppliers must architect product portfolios and contractual controls that match intended markets and export strategies.

The market exhibits moderate concentration: the largest three suppliers capture a meaningful portion of market revenues while the five-leading group consolidates a majority share. This combination of incumbent scale and specialist challengers creates predictable — but still exploitable — windows for entrants and consolidators.

Established primes: companies with deep aerospace and defense pedigree continue to leverage brand, qualification track records, and integrated-system expertise. Their product launches and defense relationships make them preferred suppliers for mission-critical programs.

High-performance MEMS challengers: semiconductor-driven vendors and MEMS specialists are converting volume and R&D into tactical-grade products that threaten traditional optical solutions in many commercial and some defense segments.

Specialists and niche innovators: firms focused on gyrocompassing, ITAR-free designs, or unique form-factor devices are winning pockets of demand where conventional vendors are slow to adapt.

Notable, recent strategic moves in the ecosystem illustrate these dynamics: major product launches that compress SWaP while improving accuracy; production scale milestones that lower unit costs; and strategic acquisitions that broaden product portfolios and route-to-market. Together these items signal both increasing competition and ongoing technological differentiation.

Integrated market model: a consolidated top-line sizing and scenario-capable forecast from 2020 through 2032, with sensitivity analytics for price, adoption rates, and regulation shocks.

Technology readiness and trade-off matrices that map sensor architectures against performance attributes, qualification pathways, and unit-cost drivers.

Regulatory and compliance playbook: a country-by-country export control overview, licensing timelines, and mitigation strategies for common procurement scenarios.

Supplier assessment framework: multi-criteria scorecards for OEM selection, including qualification status, production maturity, IP position, and post-sale support capabilities.

Commercial and procurement tools: template RFP language tailored for different performance tiers, example total cost of ownership (TCO) models, and contract clauses addressing export controls and obsolescence.

M&A and partnership maps: identification of target archetypes, valuation benchmarks, and integration risk diagnostics aimed at buyers and financial sponsors.

Executive decision calendars and investment case outlines designed to convert strategic intent into funded programs within 12–18 months.

Prioritize certification roadmaps now. Organizations bidding for defense and space work should move from proof-of-concept to formal qualification timelines this year. Certification lead times materially affect contract eligibility across the forecast horizon.

Adopt a modular sourcing strategy. Combine a primary supplier with at least one ITAR-free or regional alternative to preserve export flexibility and to mitigate single-source risks.

Invest selectively in MEMS performance and algorithms. Where SWaP constraints dominate, channel R&D toward bias stability, thermal compensation, and superior sensor fusion rather than only raw sensor improvement.

Pursue partnerships for calibration and lifecycle services. After-sale support, field calibration, and software updates represent recurring revenue pools that also lock-in platform customers.

Use targeted M&A to fill capability gaps. Acquiring firms with unique gyrocompassing, FOG expertise, or field-proven ITAR-free portfolios can accelerate market entry more effectively than greenfield builds.

Make compliance a board-level agenda item. Export control changes and classification shifts can suddenly constrain addressable markets; proactive legal and trade teams reduce transactional friction.

Create a three-track investment plan: (1) certify and qualify for targeted contracts, (2) secure second-source suppliers and supply-chain buffers, (3) fast-track integration of sensor fusion software to differentiate systems-level performance.

Run a two-week supplier audit using the report’s scorecards to validate your existing vendors and shortlist alternatives where capability or compliance gaps exist.

Develop an M&A shortlist and due-diligence checklist focused on IP maturity, customer contracts, and export-control posture; use our scenario models to size potential accretive impact.

For leaders whose 2026 budgets will fund product roadmaps, procurement decisions, or acquisition strategies, PW Consulting’s Worldwide High-performance IMU Market study turns market hypotheses into executable plans. The headline numbers — a market base of approximately USD 3.75 billion in 2025 expanding to over USD 5.5 billion by 2032 at a ~5.72% CAGR — frame the opportunity. The granular models, regulatory playbooks, supplier assessments, and go-to-market playbooks in the full report provide the operational ammunition teams need to capture it.

To access the complete datasets, interactive models, and supplier-level analyses that we intentionally omit from this public briefing, visit the report page on our website. The full deliverable contains the segmentation-level forecasts, detailed supplier profiles and scorecards, and scenario models required for transaction diligence and program planning.

For detailed analysis of this topic, please visit the official page:Worldwide High-performance IMU Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com