Worldwide Ultra-low Alpha Metal Market — Strategic Outlook for 2026 | PW Consulting

Executive summary

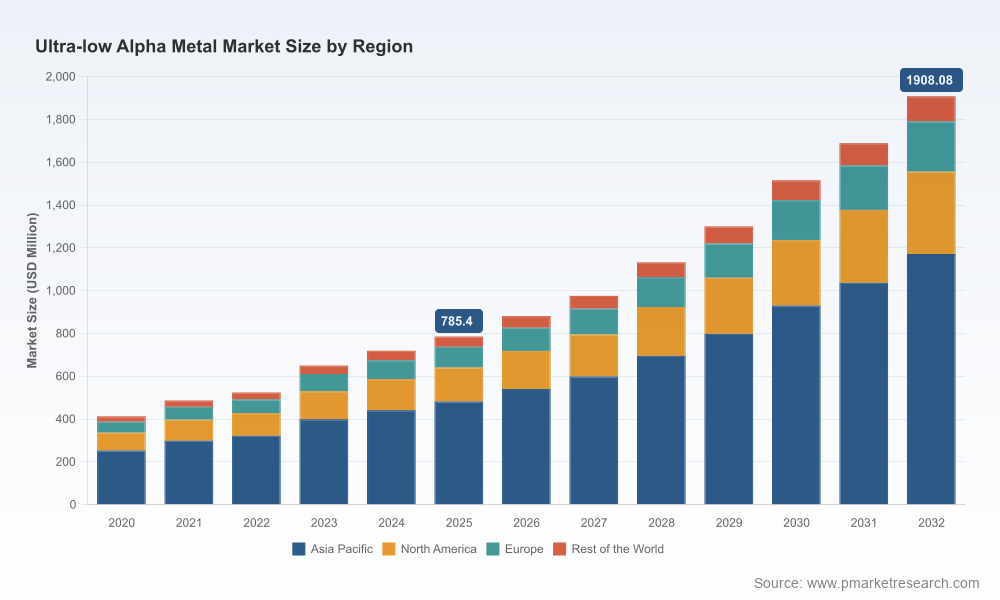

The market for ultra-low alpha metals used in advanced semiconductor packaging and interconnects is transitioning from a niche reliability play into a strategically indispensable supply layer for leading-edge device manufacturers. Our new market model, calibrated to a 2025 base year and validated across the 2020–2025 historical window, shows growth from USD 412.35 Million in 2020 to USD 785.40 Million in 2025, with a firm trajectory into the forecast period (2026–2032). PW Consulting’s forecast conservatively projects a compound annual growth rate (CAGR) of 13.52% for 2026–2032, driving an overall market value to approximately USD 1,908.08 Million by 2032.

Worldwide Ultra-low Alpha Metal Market

This research note previews the practical implications of those dynamics for executive decision-making in 2026. It highlights where companies should allocate capital, how procurement and qualification practices must evolve, and what strategic moves (partnerships, vertical integration, or M&A) will most likely unlock durable competitive advantage. To preserve the commercial value of the report’s proprietary segment-level matrices and regional splits, this piece shares the analytical framework and high-level findings while directing readers to the full report for granular figures and downloadable models.

Worldwide Ultra-low Alpha Metal Market

Why ultra-low alpha metals matter in 2026

- Scaling and packaging densification: As devices move to higher interconnect densities (flip-chip, wafer-level packaging, 3D IC and hybrid bonding), susceptibility to soft errors originating from alpha emissions becomes a binding constraint on yield and field reliability. Buyers and engineers must treat material alpha budgets as a first-order design input.

- Memory and advanced logic sensitivity: High-bandwidth memory (HBM), stacked memory architectures, and next-generation SRAM arrays have tightened allowable alpha emission thresholds—raising willingness to pay for specialty metals that demonstrably reduce soft error rates.

- Qualification lead times and supply visibility: Qualification cycles for new alloys and sources remain lengthy. Firms that secure qualified supply earlier can capture outsized share in short windows of capital-intense ramp-ups.

- Regulatory and sustainability overlay: Materials must meet RoHS and halogen-free standards while delivering ultra-low alpha performance. Increasingly, purchasers will demand traceability and circularity (reclamation/recycling) as part of supplier scorecards.

Technical constraints that create economic value

- Refining precision: Achieving emission targets in the ultra-low alpha band requires tight control of trace impurities—most notably isotopes of lead such as 210Pb—through proprietary refining and clean-handling processes. Purities at or above 99.99% (and in several cases 5N–6N tin) are typical for materials intended for advanced packaging.

- Form-factor and process readiness: Materials are supplied in multiple forms (ingots, evaporation pellets, plating anodes, powders, pastes) and must be process-compatible for plating chemistries, bumping, and evaporation equipment. Suppliers who offer application-ready chemistries shorten customer time-to-qualify.

- Traceability and equilibrium guarantees: Customers increasingly require mine-to-product traceability and guarantees of secular equilibrium (stable emissions over time). These attributes act as quality signals and create higher switching costs.

What the full report provides (practical, action-oriented content)

- Robust market sizing and scenario forecasts (2020–2032) with transparent assumptions—base-year = 2025, with the forecast window 2026–2032—together with downloadable model files to run your own sensitivity tests.

- Supply-chain maps and manufacturing economics: plant-level capability profiles, capital intensity estimates for low-alpha refining, and a roll-up of time-to-qualify by product form and application class.

- Demand-side segmentation narratives and buyer behavior archetypes (OEMs, OSATs, contract manufacturers, memory houses) coupled with three procurement playbooks (cost-minimization, reliability-maximization, supply-security).

- Competitive scorecards and supplier due-diligence templates covering refining technology, forms supplied, alpha guarantees, sustainability credentials, and qualification readiness.

- Go-to-market and commercial models: price premium elasticity, margin stress tests, and an M&A screening matrix identifying likely consolidation targets and value-creation levers.

- Regulatory and sustainability checklist: compliance pathways for RoHS/halogen-free constraints, and recommended circularity programs (recovery, reclamation and closed-loop sourcing) for corporate ESG agendas.

Competitive landscape — what incumbency looks like

The ultra-low alpha metal market displays material concentration: the top three suppliers account for a significant majority of reported revenue and the top five even more so, reflecting high barriers to entry associated with refining know-how and qualification cycles. This concentration creates a supplier market with differentiated pricing power and strategic lock-in opportunities for well-positioned firms.

Worldwide Ultra-low Alpha Metal Market

- Pure Technologies (Tequesta, FL, USA) — strengths: broad portfolio across low-to-super-ultra alpha grades, product forms (ingots, anodes, pellets, powders), and purity guarantees. Reputation for materials guaranteed at secular equilibrium and strong compliance credentials.

- Teck Resources (Vancouver, Canada) — strengths: long-standing low-alpha production infrastructure with dedicated facilities and full mine-to-product traceability; supplies evaporation pellets and anodes for semiconductor markets.

- MacDermid Alpha Electronics Solutions (USA) — strengths: vertically integrated U.S. sourcing and reclamation pathways; recent product launches targeting <0.002 cts/khr-cm² emissions demonstrate rapid commercialization focus for advanced memory and 3D IC applications.

- Mitsubishi Materials (Japan) — strengths: proprietary refining and plating chemistries tailored for flip-chip bump formation and hyper-ultra-low alpha grades for CSP/BGA applications.

- DUKSAN Hi-Metal (South Korea) and JX Advanced Metals (Japan) — strengths: regional supply leadership, precise impurity control, and custom processing into application-ready shapes.

- Honeywell and Indium Corporation (USA) — strengths: enterprise-scale materials portfolios, brand trust, and integrated packaging material solutions that reduce qualification friction for large OEMs.

Recent vendor activity underscores the dynamic nature of supply-side innovation. For example, in March 2025 MacDermid Alpha announced a new low alpha tin portfolio with ultra-low emissions and high-purity specifications targeted at SRAM, DRAM, and 3D IC/hybrid bonding—an example of supplier-driven product development aimed directly at memory and advanced packaging ramps.

Strategic implications for decision-makers in 2026

- For producers and investors: prioritize capital allocation to refining technologies and forms that reduce qualification time (evaporation pellets and plating anodes). Consider JV structures with OSATs and memory houses to underwrite offtake during early ramp phases.

- For semiconductor OEMs and OSATs: expand approved-vendor lists judiciously—balance redundancy against the cost of qualification. Invest in internal material characterization (alpha counting, trace impurity analytics) to speed vendor onboarding and reduce yield variability.

- For procurement and supply security teams: adopt a layered sourcing strategy—primary strategic partners with long-term agreements, regional second-source buffers, and an emergency inventory policy calibrated to your device’s alpha-sensitivity and certification timelines.

- For sustainability and compliance leads: require supplier-level traceability and reclamation metrics as part of the contract. Suppliers already advertising vertically integrated or reclamation-enabled supply chains will be preferred as ESG demands intensify.

- For M&A strategists: evaluate targets that either (a) own differentiated refining IP, (b) control a unique regional supply footprint, or (c) offer complementary product forms/services (plating chemistries, consumables) that shorten customers’ qualification path.

Risk scenarios and mitigations

- Supply disruption: single-site outages or raw-material bottlenecks can cause outsized impacts given qualification lead times. Mitigation: dual-sourcing, vendor inspection programs, and strategic inventories for alpha-critical product lines.

- Commoditization risk: if a breakthrough refining process significantly lowers cost, premium pricing could compress. Mitigation: invest in proprietary downstream services (application chemistries, technical support, qualification co-funding) to retain margin.

- Regulatory shifts: tightening of environmental or isotope-handling regulations could raise capex for some producers. Mitigation: early engagement with regulators and investment in compliant process design reduces retrofit risk.

How PW Consulting’s full report supports 2026 decision-making

The full Worldwide Ultra-low Alpha Metal Market report provides the granular inputs required to operationalize the strategic implications above: downloadable time-series for the 2020–2032 forecast, supplier scorecards, cost and margin models by product form, and tailored playbooks for three buyer archetypes. These assets are built to be inserted into board-level business cases, capital allocation memos, and procurement RFQs.

We deliberately present this executive preview to surface the high-impact strategic themes while preserving the report’s proprietary segment-level matrices and regional allocations—data that many clients will find mission-critical when building internal financial models or negotiating supply agreements.

Conclusion

By 2026, ultra-low alpha metals will be a strategic lever rather than a specialist input. The market’s projected growth—driven by packaging densification, memory scaling, and higher reliability demands—creates distinct opportunities for suppliers that can combine refining excellence with application readiness and traceability. For semiconductor purchasers, the choice is equally strategic: secure qualified, sustainable supply now or accept longer qualification timelines and elevated field-risk later.

PW Consulting’s full report equips decision-makers with the precise data, scenarios, and playbooks needed to act with confidence. Request the complete dataset and model access via our report page to convert the insights above into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Worldwide Ultra-low Alpha Metal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com