Building a Better Learning Experience with SevenMentor

Other |

2026-07-15 10:38:37

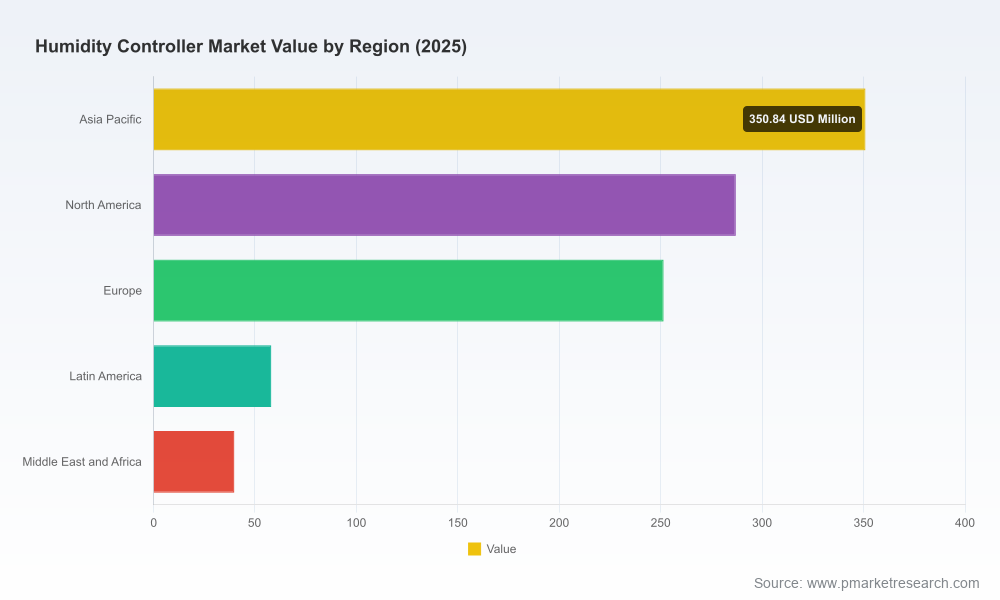

PW Consulting’s latest market research — the Worldwide Humidity Controller Market report (base year 2025, historical 2020–2025, forecast 2026–2032) — delivers the actionable intelligence executive teams need to convert market momentum into profitable, low‑risk strategies in 2026. The global market has expanded steadily through the 2020s, with total industry revenue moving from approximately USD 712.5 Million in 2020 to USD 987.0 Million in 2025. Our forecast models, trained on multi‑scenario inputs, project continued growth at a compound annual growth rate (CAGR) of 6.82% through 2032, with the market approaching an estimated USD 1,566.4 Million by 2032.

Worldwide Humidity Controller Market

Timing: 2026 is the inflection window in which technology adoption, regulatory pressure, and capital cycles intersect — creating tangible opportunities for product repositioning, channel expansion, and M&A.

Worldwide Humidity Controller Market

Decision relevance: Our analysis transforms macro growth numbers into C-suite actions — investment prioritization, supply‑chain hedges, new revenue streams, and go‑to‑market playbooks designed for FY2026 planning.

Worldwide Humidity Controller Market

Practical focus: The report is a toolbox, not an academic exercise. It contains procurement checklists, ROI templates, integration roadmaps for IoT and building automation platforms, and M&A screening filters tailored to humidity controller economics.

Market sizing and forecast (2026–2032) with base‑case and alternative scenarios calibrated to energy policy and supply‑chain shocks.

Competitive positioning matrix and qualitative profiles of leading vendors across OEM, sensor, systems integrator and test‑chamber segments.

Commercial playbooks: channel strategies, pricing elasticity estimates, and field deployment cost models for retrofit vs. new construction.

Technology roadmap: digital controllers, wireless/IoT enablement, sensor accuracy tradeoffs, and integration patterns with BMS and cloud platforms.

Supply‑chain risk register: critical materials analysis (including specialty polymers used in capacitive sensing dielectrics), single‑sourcing vulnerabilities and mitigation levers.

Regulatory compliance matrix and operational controls for ASHRAE, GMP Annex 1 (pharma), and data center humidity guidance — directly tied to product spec and service level requirements.

M&A playbook and target shortlists with integration scenarios and expected synergies for rollups in test‑chamber and precision measurement verticals.

Executive dashboards and KPI targets for product managers and commercial leaders (revenue per channel, installed base health, aftermarket attach rates).

Technology adoption: Digital controllers and IoT‑enabled devices are accelerating value capture through remote monitoring, predictive maintenance, and service monetization. These capabilities are increasingly a prerequisite in higher‑value end uses such as data centers, pharmaceutical environments, and advanced manufacturing.

Regulatory and standards tailwinds: Building performance standards and energy efficiency mandates are raising the bar for precise humidity control in HVAC systems. Concurrently, pharmaceutical GMP guidance continues to make tightly controlled humidity an operational must in critical cleanroom processes. These forces are translating into procurement requirements and longer‑term replacement cycles.

End‑use concentration: Certain verticals — industrial process control, critical infrastructure, and climate‑sensitive manufacturing — are driving demand for higher‑accuracy solutions and service contracts. Residential and basic commercial markets remain sizeable but less differentiated on technical requirements.

Supply chain sensitivity: Capacitive humidity sensors rely on polymer‑based dielectrics whose performance and cost are impacted by specialty chemical supply chains. Manufacturers that lock in diversified suppliers or invest in alternative sensing technologies will enjoy lower disruption risk and margin resilience.

Competitive consolidation and product innovation: The market is witnessing both product launches with improved sensor robustness and vendor consolidation in precision chamber and controller businesses — signals that create pockets of opportunity for both incumbents and new entrants.

Product innovation: Sensirion’s launches of new digital humidity and temperature sensor families in 2025 indicate continued upstream pressure toward higher precision, smaller form factor, and protective packaging for harsher environments — features that matter in industrial and cleanroom deployments.

M&A and portfolio realignment: The acquisition of Parameter Generation & Control by a larger instrumentation player in 2025 underscores buyer appetite for vertical integration in temperature‑and‑humidity chamber portfolios and fast‑to‑market standard solutions for laboratories.

Market engagement: Trade show activity in 2025–2026 demonstrates renewed commercial energy across HVAC, corrosion control and industrial protection segments — an opportunity window to accelerate channel engagement and thought leadership programs.

The market remains moderately concentrated: the top three firms account for just under forty percent of the market, and the top five capture slightly more than half. This structure creates a dual dynamic: scale players control platform integration and enterprise channels, while mid‑market specialists compete on precision, application expertise and aftermarket services.

Platform incumbents (e.g., multinational automation and BMS suppliers): leverage broad channel reach, cross‑sell opportunities into building and industrial automation, and enterprise procurement relationships. Expect continued investments in integrated humidity modules and BMS interoperability.

Sensor specialists and precision instrument makers: focus on sensor performance, miniaturization and reliability for high‑value applications (pharma, labs, test‑chambers). Their advantage is product differentiation and higher margins in niche segments.

Vertical leaders in test‑chambers and environmental simulation: benefit from long replacement cycles but face pressure to add connectivity and service offerings to capture recurring revenue.

Prioritize product‑led differentiation for higher‑value customers: OEMs and system integrators should accelerate development of controllers with guaranteed lifecycle accuracy, remote calibration, and service contracts — these features command premium pricing in regulated and mission‑critical segments.

Invest selectively in IoT and analytics: For many vendors the fastest path to defensibility is bundled hardware + cloud services that enable predictive humidity management and SLA‑backed uptime guarantees.

Hedge raw material exposure: Immediate supplier diversification or hedging programs for specialty polymers used in capacitive sensors reduce the probability of margin erosion from input shocks.

Pursue bolt‑on acquisitions to fill capability gaps: Target companies that add precision sensing, chamber solutions, or regional aftermarket networks; integration playbooks must prioritize serviceability and cross‑sell motions.

Align go‑to‑market with regulatory inflection points: Build commercial campaigns and technical certifications aligned with ASHRAE, GMP and data‑center guidance to shorten procurement cycles with large buyers.

Adopt scenario KPIs: Model revenue against three scenarios — policy‑driven upside, baseline CAGR, and supply‑shock downside — and define trigger thresholds for capex acceleration or conservation.

Our forecast uses a base‑case CAGR of 6.82% to 2032, but sensitivity analysis shows material variance under two key levers: (1) the pace of IoT retrofit adoption in commercial and industrial buildings, and (2) the frequency and severity of specialty chemical supply disruptions affecting sensor inputs. Firms that incorporate leading indicators for these levers into monthly management reporting will gain a competitive edge by timing investments and pricing actions more accurately.

Custom workshops that convert the report’s insights into a 90‑day action plan for product, supply chain and commercial leaders.

M&A due diligence and target valuation models tailored to humidity‑controller economics and aftermarket potential.

Implementation support for sensor sourcing strategies, IoT architecture selection, and pilot deployments in critical verticals.

Executive briefings and board materials that translate market scenarios into capital allocation guidance for FY2026.

Our full report contains the detailed segment-level modelling, vendor scorecards, financial templates and deployment case studies that underpin the strategic recommendations above. To preserve the value of proprietary segment evidence and to enable a targeted consultative follow‑up, we have intentionally withheld granular subsegment figures from this briefing. For organizations that require the complete dataset, model access, or a tailored executive workshop to accelerate 2026 planning, PW Consulting offers direct briefings and subscription access to the underlying datasets.

Contact PW Consulting to schedule a strategic briefing and obtain the complete Worldwide Humidity Controller Market report and supporting tools to inform your 2026 investment and operational decisions.

For detailed analysis of this topic, please visit the official page:Worldwide Humidity Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com