Alcoholic Drinks Industry Witnesses Growth as Consumer Preferences Continue to Evolve

Food |

2026-05-30 12:01:50

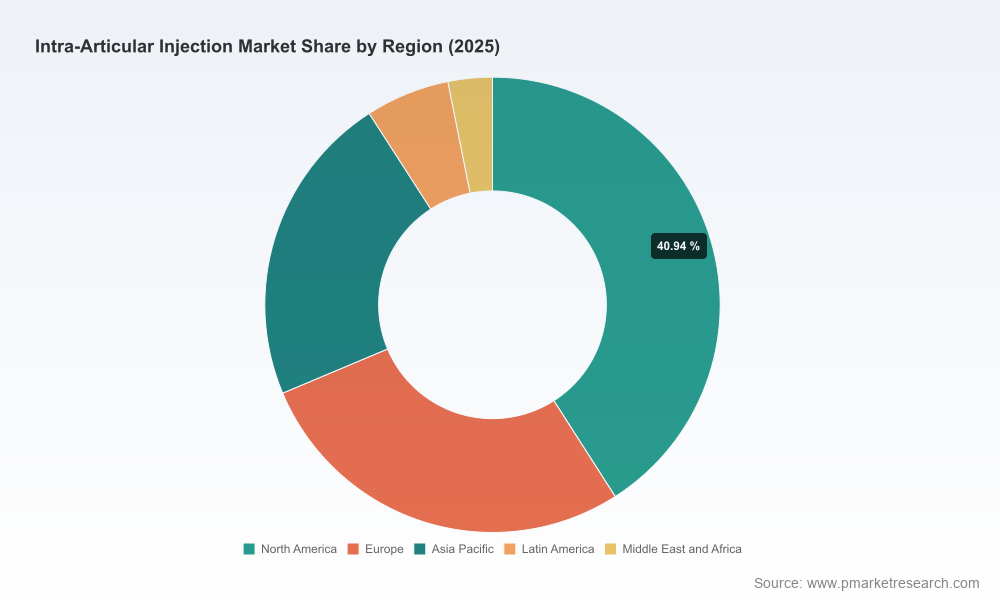

The intra‑articular injection market is entering a decisive phase. After steady expansion through the early 2020s, the market reached an estimated USD 6,660.0 Million in our base year (2025) and is now projected to more than double by 2032, reaching approximately USD 12,080.5 Million. Our forecast period (2026–2032) embeds a compound annual growth rate (CAGR) of 8.87% — a pace that both underscores robust demand for joint pain management and signals imminent disruption from new therapeutic modalities, regulatory actions, and commercial maneuvers. This PW Consulting report is designed as an operational roadmap for executives and investors who must convert that growth into profitable, defensible positions in 2026 and beyond.

Worldwide Intra-Articular Injection Market

Two converging forces define the near term: (1) sustained commercial momentum for established intra‑articular products (viscosupplements, corticosteroids, PRP and related biologics), and (2) accelerating clinical and regulatory advances — from extended‑release corticosteroids to regenerative and gene‑based single‑injection candidates — that are likely to reshape clinical pathways. Our historical review shows consistent expansion from 2020 to 2025, reflecting increasing adoption across care settings and an expanding addressable patient population. The forecasted near‑9% CAGR reflects not only baseline demand but also multiple upgrade pathways — product innovation, improved reimbursement coding, and channel optimization.

Worldwide Intra-Articular Injection Market

Prioritize optionality in product portfolios. Leading players should preserve investment capacity for late‑stage clinical opportunities (e.g., long‑acting analgesics and gene therapy approaches) while optimizing legacy hyaluronic acid and corticosteroid franchises for margin recovery and lifecycle management.

Worldwide Intra-Articular Injection Market

Accelerate payer‑engagement strategies. Reimbursement nuance matters: in key markets, procedure coding and modifier use affect unit economics and access. A proactive payer evidence strategy — real‑world evidence (RWE) demonstrating procedure outcomes, cost offsets, and site‑of‑care differentials — will materially influence uptake in 2026.

Adopt a modular commercialization playbook. Market growth will be heterogeneous by channel and indication; commercial investments should be modular, enabling targeted scaling in higher‑ROI geographies and care pathways without committing to full global launches prematurely.

Use partnerships to de‑risk innovation. Licensing and co‑development remain the most efficient routes to access novel mechanisms (e.g., extended‑release non‑opioid analgesics, intra‑articular gene therapies). Our analysis highlights late‑cycle licensing activity as a pragmatic way to accelerate time‑to‑market while preserving balance‑sheet flexibility.

Mitigate manufacturing and supply risk. Recent regulatory approvals related to manufacturing suites emphasize the importance of validated, scalable production. Contingency planning for single‑source APIs and finished product sites must be routine.

Robust market sizing and trend analysis: historical performance (2020–2025), base‑year benchmarking (2025), and modeled scenarios through 2032 that reflect varying adoption curves and pricing pressures.

Segment and channel playbooks: granular go‑to‑market strategies for product classes, clinical indications and care settings, with resource allocation templates tuned to different regional reimbursement environments. (Note: detailed segment tables and revenue splits are available exclusively in the full report.)

Regulatory and reimbursement intelligence: pathway mapping for new entrants (including fast‑track and RMAT implications), payer coding and billing mechanics, and negotiation levers tailored to national health systems and commercial payers.

Competitive and M&A heat‑maps: company scorecards, capabilities matrices, and acquisition target archetypes designed to accelerate due diligence and post‑merger integration planning.

Pipeline and clinical landscape: assessment of late‑stage and disruptive candidates, likely timelines to market, and impact scenarios on incumbent product lines.

Commercial modeling tools: pricing ladders, payer budget‑impact simulations, and sensitivity analyses to guide negotiation posture and launch sequencing.

The market exhibits moderate concentration — our concentration analysis indicates the top three firms account for a meaningful share, and the top five approach majority control — a structure that creates both barriers and acquisition opportunities. Incumbents with strong hyaluronic acid portfolios and established clinical distribution networks remain advantaged for near‑term cash generation, but strategic vulnerability varies by capability.

Sanofi (Paris) maintains durable brand equity via established viscosupplement products and should focus on maximizing lifecycle value through real‑world effectiveness campaigns and site‑of‑care optimization.

Zimmer Biomet (Warsaw, IN) and other large orthopedics players benefit from integrated relationships with surgeons and outpatient centers; their strategic play is to bundle procedural consumables and services to entrench reimbursement pathways.

Specialists such as Anika Therapeutics (Bedford, MA) and Bioventus (Durham, NC) that offer differentiated high‑molecular‑weight products can pursue targeted premium pricing but must defend against commoditization and generics pressure.

Regionally strong manufacturers — for example Ferring, Fidia, and Seikagaku — can leverage localized regulatory approvals and distribution relationships to punch above their global weight, particularly in markets where national formularies favor trusted domestic suppliers.

Large pharma and generics players (e.g., Pfizer, Teva, Johnson & Johnson via DePuy Synthes) hold an advantage in scale and payer contracting; their decisions to prioritize or deprioritize intra‑articular products will reverberate across pricing and access dynamics.

Innovators such as Pacira are reshaping the value proposition with extended‑release corticosteroid formulations and strategic licensing transactions, illustrating why non‑traditional entrants must be part of competitive monitoring.

Regulatory actions and reimbursement mechanics will determine access at the margins. Recent developments highlight two critical trends: (1) regulatory corridors enabling faster access for promising single‑injection and long‑acting therapies (e.g., Fast Track/FDA designations and RMAT), and (2) payer coding and billing particulars that materially affect adoption economics.

Regulatory acceleration: Fast Track and RMAT designations granted in the space signal that novel intra‑articular candidates can compress development timelines if clinical evidence supports durable benefit. This elevates both the upside for innovators and the competitive threat to incumbents’ repeat‑use products.

Manufacturing validation: recent approvals tied to manufacturing suites for extended‑release products underscore the growing importance of validated production capacity and supply reliability in contracting conversations.

Reimbursement posture: in major markets, procedure coding (for example, commonly used CPT codes for knee injections and site modifiers for unilateral/bilateral services) determines billing granularity and reimbursement flows. A payer‑aware clinical development plan is now table stakes for commercialization.

Portfolio triage: identify “harvest,” “invest,” and “partner” buckets. Harvest mature, low‑growth SKUs for cash; invest selectively in high‑ROI lifecycle extensions; and partner for high‑risk, high‑reward innovations.

Commercial efficiency: reallocate field resources toward high‑value clinician segments and expand digital support for remote patient engagement and outcomes monitoring to build payer‑grade RWE.

Evidence generation: prioritize comparative effectiveness studies that demonstrate durable symptom relief, reduced downstream costs (e.g., delayed joint replacement), and site‑of‑care savings.

M&A and licensing discipline: target bolt‑on acquisitions that fill manufacturing gaps, broaden clinic access, or add differentiated mechanisms of action. Licensing remains the fastest route to access late‑stage innovation while conserving capital.

The intra‑articular injection market offers compelling growth, but winning in 2026 requires more than a financial bet on a rising tide. It demands an integrated strategy that marries clinical differentiation, payer intelligence, manufacturing rigor, and targeted commercial execution. Our full Worldwide Intra‑Articular Injection Market report provides the granular segmentation, company share tables, and executable playbooks that senior leaders and deal teams need to convert growth projections into durable competitive advantage.

For organizations preparing budgets, negotiations, or M&A roadmaps in 2026, this report is an essential tool: it synthesizes market sizing (base‑year and forecast through 2032), competitive benchmarking, regulatory trackers, and bespoke commercial models designed to be operationally implemented. Detailed regional, product, and application revenue splits — together with downloadable financial models and scenario planners — are available in the full report.

Contact PW Consulting to access the complete dataset, company scorecards, and the step‑by‑step 2026 playbook that will position your organization to capture disproportionate value from a market growing at an 8.87% CAGR over the forecast period.

For detailed analysis of this topic, please visit the official page:Worldwide Intra-Articular Injection Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com