Top 07 Best Sites to Buy Naver Accounts with Full Access

Fitness |

2026-05-26 00:03:52

PW Consulting today announces the release of our authoritative market research brief, "Worldwide Semiconductor Memory IP Market — 2026 Outlook & Strategic Playbook." Built on a detailed historic review (2020–2025) and a forward-looking forecast through 2032, this report is designed to equip C-suite leaders, IP licensing teams, system architects, and procurement organizations with the frameworks and scenario-tested guidance they need to make high-consequence decisions in 2026.

Worldwide Semiconductor Memory IP Market

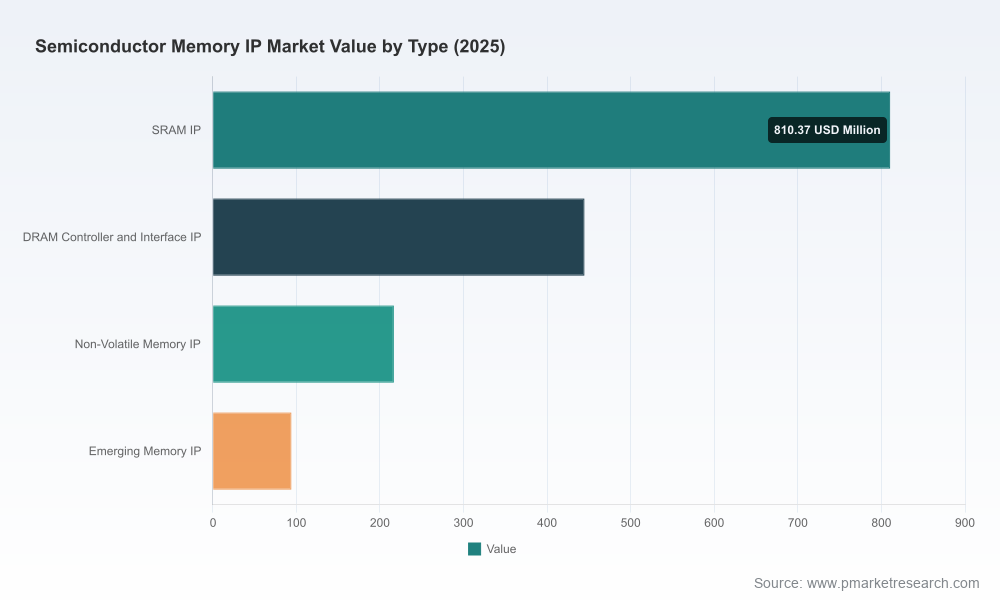

Market momentum: The memory IP market reached an aggregate size of approximately USD 1.57 billion in our base year (2025) and PW Consulting’s model points to sustained growth at a compound annual growth rate (CAGR) of 14.0% during the forecast horizon. These macro dynamics are reshaping how semiconductor companies prioritize memory IP investments versus full-chip design in-house.

Worldwide Semiconductor Memory IP Market

Concentration dynamics: The market displays significant supplier concentration (top-three players account for a substantial portion of the market, with a CR3 of approximately 68.5% and CR5 near 82.3%), which directly affects pricing power, roadmap pacing, and licensing leverage for buyers and ecosystem partners.

Worldwide Semiconductor Memory IP Market

Strategic inflection in 2026: A confluence of technology (HBM3/4, DDR7, advanced embedded SRAM/Non-Volatile solutions), supply-chain shocks, and new regulatory pressures will make 2026 the year when procurement strategy, IP partner selection, and architectural decisions lock in multi-year cost and performance outcomes.

Proprietary market model: Dynamic, scenario-capable market-sizing with upside/downside paths tuned to demand elasticity from AI cycles, memory-price shock events, and regional procurement policy shifts.

Risk matrix and mitigation playbooks: Actionable steps to hedge raw-material and manufacturing exposure, supplier concentration risk, and regulatory disruption scenarios.

Technology roadmap and node migration playbook: Guidance on migrating embedded memory IP across advanced process nodes while balancing area, power, and performance (PPA) trade-offs; verification and silicon-proven readiness criteria to de-risk tapeouts.

Vendor selection framework: A multi-criteria scoring model that translates fit-for-purpose attributes (PPA, multi-foundry portability, documentation and support, security IP integration, licensing T&Cs) into procurement-ready supplier shortlists.

Commercial templates: Negotiation playbooks and licensing constructs designed for OEMs, fabless designers, and IDMs—covering perpetual vs. time-limited licenses, royalty structuring, and bundling strategies for foundation IP.

Integration and verification checklist: Practical milestones and test vectors for embedding third-party memory IP, including recommended metrics, silicon bring-up sequencing, and cross-team governance models.

AI-driven memory demand: The rapid adoption of high-bandwidth memory (HBM family) and next-generation DDR (DDR7) in AI and data-center accelerators is reallocating supply and pushing premium pricing in adjacent consumer memory tiers. Expect cascading impacts on design cycles, BOM forecasting, and memory-subsystem architecture choices.

Raw-material and geopolitical supply risk: Recent global developments have concentrated certain critical raw materials and introduced export controls that affect upstream semiconductor manufacturing supplies. These developments require memory IP consumers to layer supply-chain contingency into both supplier selection and technology roadmaps.

Regulatory headwinds: New procurement rules and export-control proposals in major markets are increasing the compliance burden for SoC suppliers and OEMs. IP licensing teams must now assess geopolitical eligibility, audit clauses, and stipulations that may constrain who can supply or integrate certain memory IP elements.

Consolidation and vertical integration: Industry M&A and strategic acquisitions have accelerated, altering bargaining positions between IP providers, EDA players, and foundries. This dynamic is reshaping partnership models—partners that once complemented each other may now compete, affecting roadmaps and interoperability commitments.

Synopsys: Positioned as a leading provider of silicon-proven embedded memory IP, Synopsys emphasizes PPA optimization for advanced nodes and close integration with leading foundry toolchains. Their strength lies in mature compilers, broad node coverage, and deep verification suites—making them the safe, low-risk choice for high-volume SoCs.

Cadence: With its recent acquisition of the Artisan Foundation IP assets, Cadence has reinforced its embedded-memory portfolio and foundation IP play. The transaction signals intensified competition in embedded compilers and suggests a stronger offering for customers seeking bundled EDA-to-IP workflows and tighter performance interpolation across physical design flows.

Arm: Arm continues to supply memory IP as part of its broader SoC IP platform, with emphasis on power-efficient, processor-aligned memory configurations. Arm’s ecosystem reach and architecture-level integration remain compelling for partners prioritizing low-power mobile and edge segments.

Rambus: Focused on high-speed memory interface IP (DDR5/LPDDR5/HBM/GDDR) and related subsystems, Rambus is a strategic vendor for high-performance compute stacks where interface robustness and throughput are mission-critical.

Regional and specialist players: A cohort of foundry-partnered and regionally focused IP vendors (from Taiwan, Europe, and China) deliver differentiated embedded NVM, MRAM, and low-power SRAM offerings. These vendors are gaining recognition through foundry ecosystem programs and awards—often serving customers with specialized node or regional compliance needs.

Implication: Buyers must align supplier selection with three vectors—technology fit (memory type and node), commercial flexibility (licensing and bundling), and geopolitical-compliance posture—to avoid costly replacement or compliance rework post-tapeout.

Strategic acquisitions: Market-shaping M&A that consolidates foundation IP assets creates both risk (less supplier diversity) and opportunity (simplified tool/IP co-optimization).

Foundry awards and recognitions: Vendors accepted into major foundry programs gain route-to-market and validation advantages that accelerate adoption for advanced embedded memory IP.

Cross-industry licensing and partnerships: IP licensing agreements in high-reliability and automotive platforms are expanding the addressable market for certain memory IP types—while also driving stricter QA/process flow requirements.

Immediate (0–6 months): Conduct a supplier-risk heatmap that overlays technical fit with geopolitical exposure and raw-material sensitivity. Lock in flexible licensing pilots for compute-critical projects to preserve switching optionality.

Medium term (6–18 months): Implement cross-functional IP governance (procurement, design, legal, security) and adopt the report’s vendor selection scorecard to inform multi-project sourcing. Prioritize silicon-proven IP for mission-critical designs and require multi-foundry porting commitments for medium-to-long-term products.

Longer horizon (18+ months): Revisit architecture choices to factor in evolving memory stacks (HBM/DDR7 impacts), and contractually secure capacity and roadmap alignment with strategic IP vendors. Consider selective co-development or equity partnerships with specialized IP firms to obtain priority access to advanced memory IP innovations.

Chief Product Officers and VP Engineering — for roadmap alignment and risk budgeting across multi-year SoC programs.

Procurement and Legal teams — for playbooks on licensing negotiation, compliance screening, and supply-chain contingency clauses.

IP and SoC architects — for node migration playbooks, silicon-proven readiness criteria, and integration checklists.

Investment and corporate strategy teams — for a scenario-based view of market growth, concentration, and potential M&A or partnership targets.

To preserve the value and actionability of the research for subscribers and industry practitioners, this press summary highlights macro trends, supplier dynamics, and strategic guidance while intentionally omitting detailed segment-level tables and regional/application-specific revenue breakdowns. The granular segmentation, proprietary forecasts by application and geography, and downloadable modeling workbooks are available exclusively through the PW Consulting report portal. This approach follows our “trailer” principle: provide enough insight to enable informed, early-stage decision-making while routing stakeholders who need execution-ready numbers and vendor-level scorecards to the full report.

For organizations preparing to finalize 2026 budgets, renegotiate IP licenses, or select partners for next-generation SoC designs, the tactical frameworks and scenario models in PW Consulting’s "Worldwide Semiconductor Memory IP Market — 2026 Outlook & Strategic Playbook" offer a practical advantage. Visit PW Consulting’s reports page to access the full report, purchase the dataset, or schedule a briefing with our lead analysts to walk through the model and supplier shortlists tailored to your business priorities.

PW Consulting’s lead analysts remain available for executive briefings and bespoke consultancy engagements to translate the report’s insights into executable procurement, engineering, and M&A plays—helping you lock in resilient, high-performance memory subsystems that support your strategic objectives in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Semiconductor Memory IP Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com