Why Is Smart Water Bottle Market Gaining Popularity Among Fitness Consumers?

Networking |

2026-05-11 09:02:01

As organizations plan capital allocations, product roadmaps, and supply-chain hedges for 2026, the portable single phase generator market is presenting a rare combination of steady demand growth and accelerating structural change. PW Consulting’s latest market study uses an integrated, data-driven lens to translate market trajectories, regulatory inflection points, and competitive moves into actionable decision pathways. This press preview highlights the strategic value of the full report for senior executives, private equity investors, OEMs, and industrial purchasers — while reserving the detailed segmentation tables and proprietary scorecards for report subscribers.

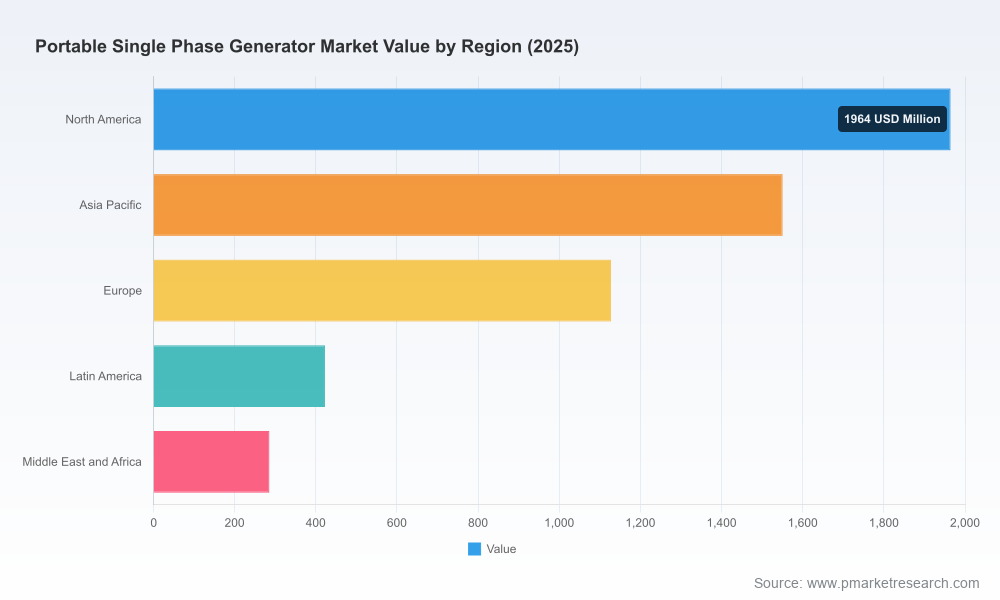

Worldwide Portable Single Phase Generator Market

Our analysis positions the global portable single phase generator market on a multi-year expansion path. After a recovery phase through the early 2020s, the market size reached a meaningful milestone in the 2025 base year. PW Consulting’s forecast projects continued growth over the 2026–2032 horizon at a compound annual growth rate (CAGR) consistent with mid-single digits, reflecting resilient demand across backup power, construction, rental fleets, and outdoor events. Importantly, growth is being supported by a combination of recurring replacement cycles, increased household preparedness, and the professionalization of rental and jobsite fleets in both developed and emerging markets.

Worldwide Portable Single Phase Generator Market

These headline metrics mask divergent microtrends: pockets of rapid adoption (driven by climate-driven outages and large infrastructure projects), regulatory-driven product churn (emissions and noise standards), and technology-driven product differentiation (inverter electronics, hybridization, and silent-pack engineering). For decision-makers in 2026, the question is no longer whether the market grows, but which business model and product investment will capture the premium segments of that growth.

Worldwide Portable Single Phase Generator Market

Regulatory squeeze and temporary relief: Recent regulatory actions have compressed product windows and accelerated compliance costs. Notably, emergency regulatory adjustments in 2025 provided temporary sales relief in a crucial market to meet wildfire-driven demand. At the same time, medium-term transitions toward stricter state-level emissions objectives and targeted timelines for small off-road spark-ignition engines are reshaping product roadmaps.

Input-cost and supply-chain pressure: Raw material classifications and price volatility — particularly the designation of copper as a critical mineral — are raising the cost of alternator and wiring assemblies. Procurement strategies and engineering choices will materially affect margins.

Product & channel innovation: Leading OEMs are launching California-compliant inverter and dual-fuel platforms, and new silent-pack certifications are opening rental and residential channels that prioritize low acoustic signatures. These advances change buyer expectations and create differentiation opportunities for incumbents and entrants alike.

Strategic forecast and scenarios: Base and alternative scenarios to 2032, stress-tested for regulatory shifts, raw-material shocks, and demand surges tied to climate events.

Commercial playbooks: Segment-specific go-to-market strategies for OEMs, rental companies, and distributors, including pricing architectures, product-pack configuration recommendations, and aftermarket service models.

Product roadmaps and technology windows: Comparative evaluation of inverter vs. conventional topologies, noise mitigation investments, and hybridization options — aligned with cost-to-benefit crossovers and time-to-market constraints.

Supply-chain heat maps: Critical component concentration analysis, alternative sourcing scenarios for copper and electronic controls, and mitigations for logistics disruptions.

Regulatory impact matrix: Jurisdiction-by-jurisdiction compliance milestones, risk scores for market access, and recommended compliance investment timelines to minimize business interruption.

Competitive diagnostics: A qualitative and quantitative assessment of leading manufacturers’ go-to-market strengths, product portfolios, channel footprints, and M&A propensity — with prioritised target lists for partnerships, distribution agreements, and acquisition candidates.

Commercial diligence toolkit: Vendor scorecards, benchmarking templates, and a valuation primer designed for private equity and corporate development teams evaluating acquisitions in the space.

The sector remains led by a mix of global consumer-engine specialists, industrial engine houses, and equipment manufacturers focused on construction and rental markets. Market concentration metrics indicate a moderate-to-high aggregation at the top, underscoring the strategic advantage enjoyed by established brands with deep channel and service networks. However, fragmentation below the leading cohort leaves room for disciplined consolidation and niche-focused entrants.

Notable companies covered in our analysis include multinational engine and equipment leaders, specialist portable-power players, and a cohort of high-volume exporters from Asia and Europe. These firms differ in strategic posture — from consumer-oriented, low-noise inverter models to heavy-duty diesel solutions for industrial applications — and each has a distinct exposure to regulatory and supply-chain risk.

Global OEMs and consumer brands: Companies with legacy small-engine expertise continue to command consumer trust for residential and recreational use, leveraging fuel-efficiency and acoustic performance as primary differentiators.

Industrial and rental-focused players: Manufacturers targeting construction and rental channels emphasize durability, serviceability, and total-cost-of-ownership metrics over upfront price.

OEMs driving compliance-led product introductions: In 2025 and early 2026, several leaders launched or certified new models that address tightened emissions rules, enabling immediate market access in regulated jurisdictions while reshaping competitive positioning.

Product launches and certification moves: Several large manufacturers refreshed portable inverter and compliant product lines in 2025, targeting both consumer and jobsite buyers. These product introductions shorten incumbents’ lead time for compliance and raise entry barriers for smaller manufacturers without similar engineering resources.

Regulatory adjustments with strategic ripple effects: Emergency regulatory relief in 2025 that temporarily broadened saleability of certain EPA-certified units in a major state highlighted how episodic public-safety needs can rewrite near-term demand curves. However, medium-term trajectories toward zero-emission policies remain in place, compressing the window for gasoline- and diesel-centric product strategies.

Input-cost & raw-material alerts: The critical-mineral status of copper elevates procurement risk for alternators and wiring harnesses. Organizations that implement hedging mechanisms or design for copper reduction can gain a durable cost advantage.

Operational guidance from regulators: Enforcement clarifications for non-road diesel engine standards provide short-term operational relief in some respects, but the combination of emissions enforcement and evolving warranty and telematics expectations increases lifecycle product complexity.

Prioritize modular, upgradeable architectures: Design platforms to accept emissions-upgrade kits, inverter modules, or acoustic packages. This reduces the risk of stranded inventory if local standards tighten or carve-outs close.

Recalibrate sourcing and total-cost models: Incorporate copper-price sensitivity into scenario planning and qualify alternative materials and suppliers. Consider long-term purchase agreements for critical components to stabilize margins.

Expand service and aftermarket offerings: Rental and fleet operators are increasingly monetizing uptime guarantees and preventive maintenance — an attractive margin pool compared with hardware alone.

Accelerate compliance-ready product launches: For firms with global ambitions, timing product introductions around upcoming jurisdictional standards can win early shelf space and reduce retrofit exposure.

Assess M&A and partnership targets: Consolidation opportunities remain in manufacturing scale, component sourcing, and software/telemetry capabilities. Target selection should prioritize complementary distribution reach and service capability rather than pure capacity.

Executives who need to make high-stakes decisions this year will benefit from the full report’s combination of forward-looking market sizing, proprietary competitive scoring, and hands-on implementation tools. The study goes beyond descriptive market metrics to model the financial and operational outcomes of alternative strategic choices — for example, the revenue and margin impact of converting a core product line to inverter architecture versus pursuing a lower-cost diesel-centric strategy for rental fleets.

We deliberately designed the deliverables to be practical: executive summaries with clear strategic recommendations, board-ready slide decks, and downloadable decision-support spreadsheets that map product investments to P&L scenarios and inventory risk. Our M&A diligence appendices provide transaction-ready checklists and a shortlist of potential targets validated against our competitive diagnostics.

This preview is intentionally structured to reveal the factors shaping the market without disclosing the full segmentation tables and proprietary scoring that underlie our recommendations. For firms preparing budgets and investment roadmaps in 2026, timely access to that level of detail materially alters negotiation positions, procurement choices, and go-to-market timing.

To obtain the complete Worldwide Portable Single Phase Generator Market report — including regional and application-level segmentation, detailed competitive share matrices, supplier directories, and the full set of playbooks and financial models — please visit our report landing page or contact a PW Consulting representative. The full report provides the raw data and executable templates necessary to translate the strategic imperatives outlined above into measurable outcomes for 2026 and beyond.

PW Consulting — translating market complexity into decisive, actionable strategies.

For detailed analysis of this topic, please visit the official page:Worldwide Portable Single Phase Generator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com