Sunroof Glazing Market Growth Trends

Other |

2026-06-04 14:09:52

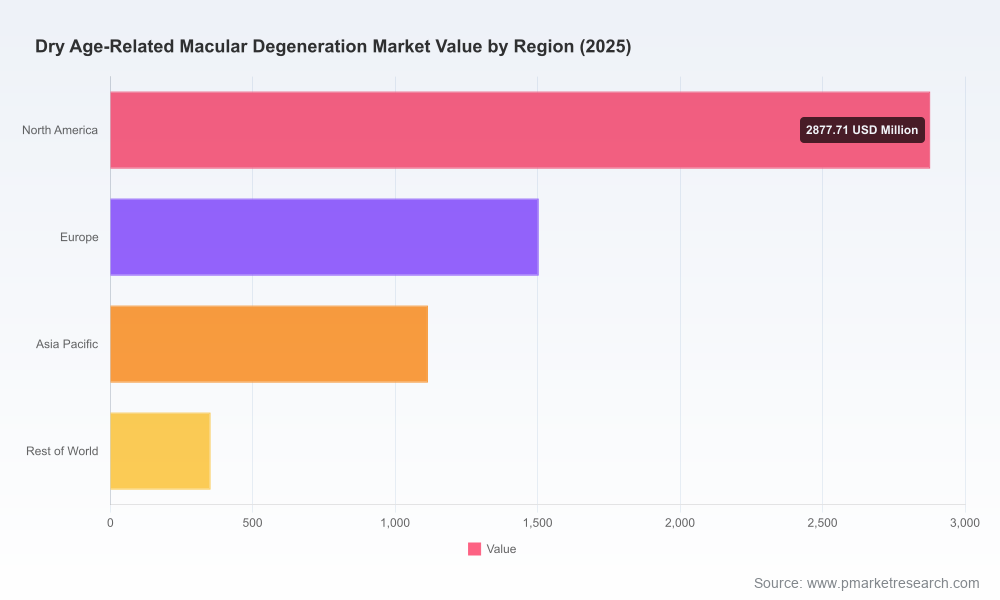

PW Consulting today publishes an executive briefing that accompanies our full market study, Worldwide Dry Age-Related Macular Degeneration (AMD) Market (base year 2025). The briefing distills the analytical backbone and strategic implications senior leaders need to act in 2026. Our model shows the market expanding from USD 3,850.4 Million in 2020 to USD 5,850.0 Million in 2025, with a 2026 opening-year projection of approximately USD 6,262.8 Million and a compound annual growth rate (CAGR) of 10.25% through 2032, at which point our base forecast reaches about USD 11,582.2 Million (USD Million figures, nominal).

Worldwide Dry Age-Related Macular Degeneration Market

Therapeutic innovation has moved from theory to commercial reality. Regulatory milestones in recent years introduced the first disease-modifying treatments for geographic atrophy (GA), and 2024–2025 brought additional label and device approvals that materially change the treatment mix available to clinicians and payers.

Worldwide Dry Age-Related Macular Degeneration Market

Modalities now span complement inhibition, oral small molecules, mitochondrial peptides, gene therapies, RPE cell therapies, and non-invasive photobiomodulation — a breadth that transforms commercial and clinical pathways and accelerates market growth drivers while complicating go-to-market decisions.

Worldwide Dry Age-Related Macular Degeneration Market

Market structure is moderately consolidated: the top three players account for a majority share (CR3 ≈ 58.4%), and the top five represent over 70% (CR5 ≈ 72.1%). This concentration creates both competitive barriers and attractive M&A pickings for agile entrants and strategic acquirers.

Payer and patient dynamics remain pivotal. Currently approved complement inhibitors require recurrent intravitreal injections, which introduces adherence and reimbursement friction; clinical effect sizes to date reduce lesion growth by roughly 20–36% and do not restore lost vision. These realities shape coverage, pricing negotiations, and real-world uptake assumptions.

Proprietary market model (2020–2032) with scenario engines: base, conservative, and accelerated adoption curves designed for rapid sensitivity testing by revenue, patient flow, and uptake levers.

Patient-pathway mapping and diagnosis funnel mechanics: incidence / prevalence baselines, diagnostic rates, referral patterns, and expected shifts as new modalities enter clinics and outpatient settings.

Commercial playbooks by modality and development stage: launch sequencing, KOL engagement templates, field force sizing, and channel strategies for clinic-administered vs. home-based therapies.

Payer and HTA assessment toolkit: reimbursement case templates, economic modelling inputs (QALY, budget impact), and sample contracting structures including outcomes-based constructs grounded in lesion-slowing endpoints.

Pipeline and competitive benchmark dossiers: risk-adjusted valuations, likely timelines to approval, and strategic options (partner, license, bolt-on acquisition) for over a dozen active programs.

Manufacturing and supply-chain readiness checklist: capacity bottlenecks for biologics and gene/cell therapies, device manufacturing considerations, and mitigation playbooks for raw-material and CMC risk.

Field evidence blueprints: real-world evidence study designs and digital monitoring concepts to bridge RCT-to-practice value gaps that payers will require.

Apellis Pharmaceuticals (US) — commercializing a complement C3 inhibitor — faces the classic incumbent dilemma: defend dosing-based revenue while reducing real-world friction. Our analysis recommends dual investments in adherence-enabling services and payer evidence generation to protect product economics.

Astellas Pharma (Japan) — with a C5 inhibitor that recently secured label expansion — will need to translate broader labeling into access gains. We identify targeted HTA dossiers and country-specific budget-impact models as high-priority actions for 2026 launches and contracting.

LumiThera (US) — now marketing a photobiomodulation device — introduces a non-invasive care pathway that will change provider workflows and create novel reimbursement categories. Commercial strategies must focus on outpatient adoption, reimbursement codes, and device-as-a-service offerings for clinics.

Late-stage oral developers (Alkeus, Belite) and peptide/gene contenders (Stealth, Annexon, Ocugen, Aviceda) present asymmetric upside: oral or systemic treatments can materially reduce clinic visits and payer costs, but will require differentiated payer economics and strong real-world durability data.

Cell and gene plays (Lineage/Roche collaboration, Boehringer Ingelheim programs, others) complicate launch readiness due to manufacturing complexity and one-time pricing dynamics; we recommend early investment in supply strategies and outcomes contract designs.

Big-cap pharma and large biotech (Roche, Novartis, Regeneron, Johnson & Johnson) maintain optionality via partnerships and M&A; our strategic matrix evaluates when to compete, co-develop, or acquire based on pipeline synergies and manufacturing footprints.

Re-frame portfolio prioritization around patient burden and delivery modality: prioritize assets that materially reduce clinic visit frequency or provide differentiated functional outcomes.

Accelerate payer engagement early: build HTA-grade evidence packages that model long-term societal benefits of lesion-slowing therapies and provide pragmatic real-world study designs to de-risk coverage decisions.

Design commercial models that solve adherence: bundled services, mobile injection teams, home-based administration pilots, and patient-support platforms will be key levers to maximize real-world efficacy and revenue retention.

Secure manufacturing and CMC partners now: biologics, gene, and cell therapies require lead times that can dictate launch economics. Consider contract manufacturing expansions, geographic redundancy, and tolling agreements to protect launch windows.

Evaluate M&A and licensing targets using a concentration-aware lens: with CR3/CR5 indicating moderate concentration, bolt-on acquisitions or licensing deals can be accretive if they extend clinic reach, delivery technology, or durable data assets.

Prepare for device and digital entrants: non-invasive devices and monitoring tools will create new clinical protocols and reimbursement pathways — incumbents should pursue partnerships or white-label strategies.

Payer pushback if real-world effectiveness diverges from trial lesion-slowing metrics.

Regulatory surprises in gene and cell-therapy safety or manufacturing inspections that delay approvals.

Supply-chain or raw-material constraints for biologics and specialty APIs that compress launch timing.

Rapid adoption of non-invasive therapies in early/intermediate populations that reshapes clinic referral patterns and compresses addressable market for injectables.

Scenario planning: plug our base-case and sensitivity outputs into your internal financial model to test pricing, uptake, and contracting permutations for 2026 budget cycles.

Commercial readiness: use our launch playbooks and field-sizing templates to finalize hiring, training, and KOL engagement plans in Q1–Q2 2026.

M&A and partnering: leverage our target-screening filters and risk-adjusted valuations to prioritize licensing or acquisition targets aligned to your modality gaps.

Payer negotiations: adapt our HTA and budget-impact decks to local markets and use the recommended outcomes-focused contracting templates to improve acceptance rates.

PW Consulting’s full report contains the detailed tables, downloadable model, and confidential appendices that senior management and transaction teams require. The briefing here is intentionally selective — it surfaces critical directional insight but omits the granular regional, product-type and disease-stage splits that are included only in the full report to preserve the integrity of our subscription-grade IP.

Contact PW Consulting or visit our report page to access the complete Worldwide Dry Age-Related Macular Degeneration Market study, the downloadable financial model, and tailored advisory options for 2026 strategic planning, M&A diligence, or payer-access programs. For teams preparing 2026 budgets and launch plans, the window to lock supply chains, finalize HTA evidence packages, and secure payer agreements is now — the market momentum and modality shifts we document will define winners and laggards over the next three years.

For detailed analysis of this topic, please visit the official page:Worldwide Dry Age-Related Macular Degeneration Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com