Can Fat Melting Injections improve facial contour sharpness?

Health |

2026-05-05 04:42:33

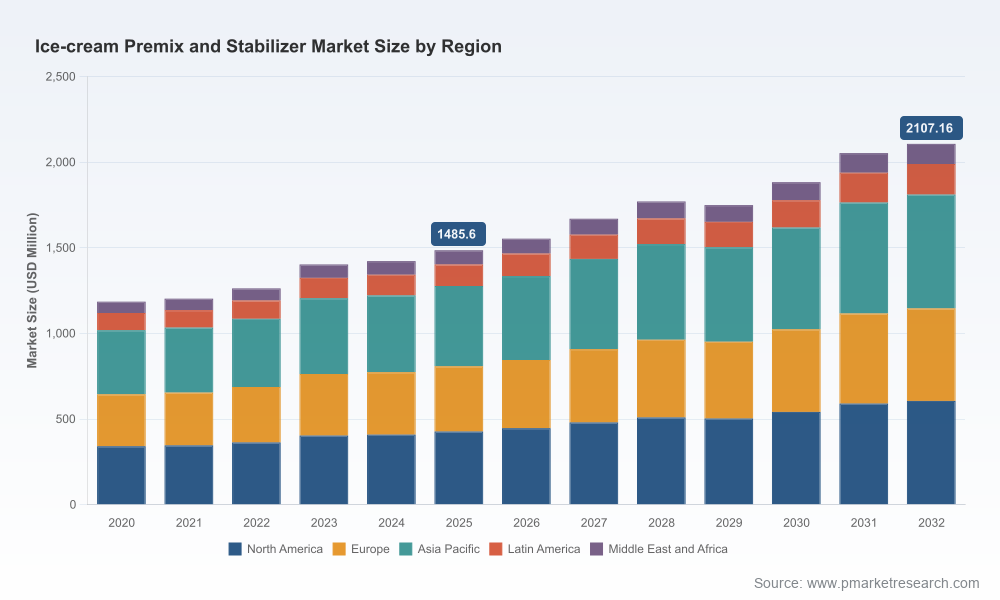

PW Consulting’s latest market study on the Worldwide Ice‑cream Premix and Stabilizer Market is designed as a decision‑grade briefing for executive teams planning 2026 strategies. The market, having expanded into the mid‑billion USD range by 2025 and projected to grow at a steady compound annual rate (CAGR) of approximately 5.12% through 2032, is transitioning from a predominantly ingredient‑driven supply chain to a more integrated, sustainability‑and‑regulation‑sensitive commercial ecosystem. This release highlights the report’s strategic value and actionable takeaways while deliberately withholding detailed segment‑level tables and proprietary price curves — available in the full report for subscribers and clients.

Worldwide Ice-cream Premix and Stabilizer Market

After a period of resilient recovery and premiumization, the global premix and stabilizer market crossed an important scale threshold in 2025 and is forecast to continue expanding through the end of the decade. Growth is supported by intensifying R&D into clean‑label and plant‑based stabilizers, rising industrialization of frozen‑dessert production in developing markets, and product mix shifts toward premium and functional formulations.

Worldwide Ice-cream Premix and Stabilizer Market

Market structure remains moderately concentrated: the top three suppliers account for roughly two‑fifths of market share while the top five approach a majority position. That concentration profile creates a dual dynamic — clear incumbent advantages for scale players, but meaningful white‑space for specialist formulators and regional champions to capture premium niches or supply chain roles that scale players cede.

Worldwide Ice-cream Premix and Stabilizer Market

Regulatory acceleration: New EU regulations introduced in early 2026 revise maximum levels, purity standards, and microbiological criteria for food additives, with compliance timelines stretching from mid‑2026 into 2028. In parallel, the EU Packaging and Packaging Waste Regulation (PPWR) tightens labeling and recyclability requirements for ingredient packaging. These rules will force reformulation, documentation upgrades, and packaging redesign projects with material lead times.

Raw‑material volatility and sourcing: Skimmed milk powder (SMP) remains a foundational input in many dairy‑based premixes; its prominence in the dairy ingredient complex makes it a key lever for cost and quality. Price signals in 2026 (including USDA forecasts) indicate pressure points that procurement teams must hedge against or mitigate via alternative protein and fat systems.

Innovation vectors: R&D is focused on delivering LBG‑free and plant‑based hydrocolloid systems, improved heat‑shock stability, and clean‑label emulsifier combinations that support melt control without compromising creaminess. Meanwhile, rapid prototyping of premixes for regional flavor profiles and ready‑to‑market powders remains a growth engine for agile suppliers.

Sustainability and packaging compliance: With PPWR coming into force and corporate sustainability targets tightening, ingredient suppliers and premix manufacturers must demonstrate packaging recyclability and material provenance. This is already influencing procurement, logistics and shelf‑life decisions.

The competitive map comprises three broad archetypes: global ingredient giants, specialist hydrocolloid and emulsifier innovators, and regional/full‑service premix manufacturers. Each group competes on different vectors — scale and distribution, formulation IP, or speed‑to‑market and local service.

Global ingredients and formulators (e.g., Cargill, Kerry Group, Tate & Lyle, IFF/Danisco Cremodan). These players bring scale, broad application R&D and global supply chains. Strategic moves in 2025–2026 include targeted showcases of functional blends and tailored offerings for fast‑growing B2B segments in markets such as India. Their strengths are formulation depth, regulatory dossiers, and co‑development with large OEMs.

Hydrocolloid and stabilizer specialists (e.g., Palsgaard, CP Kelco, TIC Gums, Jungbunzlauer, Gino Biotech, Hindustan Gum). These firms differentiate on technical capability — proprietary blends that improve melt resistance, texture and clean‑label claims. Recent M&A and footprint investments by one specialist signal increased competition for North American supply and faster customer response times.

Premix and application specialists (e.g., PreGel, Rubicone, Tropilite Foods, Matrix Flavours, Scott Brothers Dairy, Oleo‑Fats, Nitin’s). These manufacturers excel at turning ingredient systems into ready‑to‑market powder or liquid premixes, private‑label services and co‑packing. Many have deep export networks, regional flavor expertise and quick customization capabilities required by artisan and industrial customers alike.

Notable recent developments validate these themes: a specialist stabilizer producer announced a strategic production‑site acquisition in the U.S. to build domestic manufacturing capacity; a global ingredient supplier highlighted indulgent yet health‑conscious blends for a key emerging market; and competitors continue to use trade shows as platforms to introduce new stabilizing systems. These activities underscore the arms race between scale, formulation IP and local manufacturing agility.

The study is built as an operational playbook for commercial, R&D, procurement and M&A teams. Key modules include:

Proprietary forecasting model: market size trajectories (2020–2032), scenario runs for raw‑material shocks and regulatory impact pathways.

Supplier and capability scorecards: technical capabilities, certifications, footprint maps, and partner fit for co‑development and co‑packing.

Formulation and substitution matrix: technical recipes for cost mitigation, plant‑based swaps, and clean‑label reformulations, plus sensory tradeoffs and production constraints.

Regulatory compliance toolkit: mapping of new EU additive and packaging rules against commercial timelines, required documentation templates and audit checklists.

Price and margin sensitivity dashboards: raw‑material exposure analysis with hedging scenarios and alternative input sourcing strategies.

Go‑to‑market playbooks: channel segmentation, private label vs. branded strategies, and quick‑start recipes for industrial and artisan customers.

M&A and partnership radar: valuation heuristics for niche stabilizer assets and integration checklists for bolt‑on acquisitions.

Prioritize regulatory readiness: establish a cross‑functional compliance sprint to align formulations, labels and packaging with the new EU additive rules and PPWR timelines. Early remediation reduces rework and market access risk.

Hedge raw‑material exposure: incorporate SMP and all‑milk price scenarios into procurement KPIs; consider long‑term supply contracts, partial substitution pathways and use of functional starches or protein concentrates where feasible.

Invest in formulation IP for clean‑label and plant‑based demands: allocate R&D capacity to LBG‑free systems and sensory optimization that preserve melt control.

Reassess packaging strategies now: implement a PPWR compliance roadmap that balances recyclability, shelf‑life and cost — and capture shelf‑edge sustainability claims where performance allows.

Pursue selective supply chain localization: assess co‑manufacturing or acquisition options to reduce lead times and tariff exposure in priority markets, taking into account footprint moves by competitors.

Use the market concentration profile to craft competitive playbooks: negotiate long‑term partnerships with scale suppliers for commodity components, while cultivating specialist formulators for innovation and differentiation.

Embed sustainability metrics in product design: quantify lifecycle impacts of stabilizer choices and packaging constructs to support customer procurement requirements and retailer scorecards.

Boards and executive teams will find the report valuable as the foundation for several immediate processes: 90‑to‑120 day compliance and procurement plans, R&D prioritization workshops, M&A target screening and private‑label pricing strategies. While this article surfaces the strategic imperatives and regulatory timing that must inform 2026 decisions, the full report provides the granular segmentation, supplier benchmarking, and price‑curve detail needed to operationalize those priorities.

If your 2026 plan depends on production continuity, regulatory certainty, or premium portfolio growth in frozen desserts, the intelligence in this study will materially change program priorities and resource allocation. To access the full set of models, supplier scorecards and the regulatory compliance matrix, please consult the complete report page or contact PW Consulting for a tailored briefing and scenario workshop.

For detailed analysis of this topic, please visit the official page:Worldwide Ice-cream Premix and Stabilizer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com