How Managed SIEM Providers Strengthen Critical Cybersecurity for U.S. SMEs in the ICT Industry

Cyber Security |

2026-07-06 07:57:00

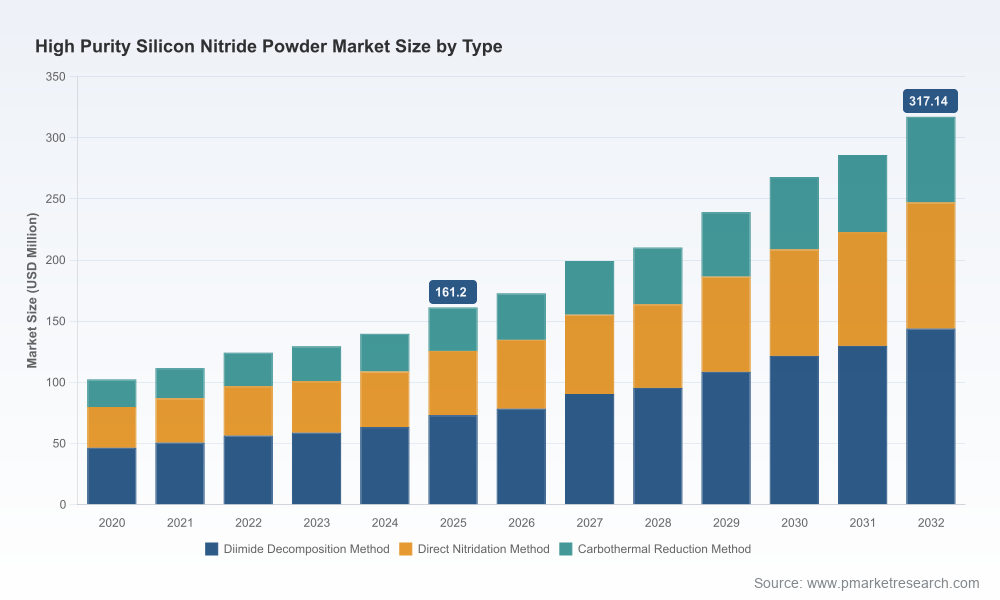

As demand for high-performance ceramics escalates across electrification, advanced electronics, and aerospace systems, high purity silicon nitride (Si3N4) powder has moved from a niche feedstock into a strategic industrial material. PW Consulting’s latest Worldwide High Purity Silicon Nitride Powder Market report (base year 2025, forecast 2026–2032) provides an operationally focused intelligence package designed to inform C-suite and investment decisions in 2026. The market is on a sustained growth trajectory—historical expansion through 2020–2025, and a robust compound annual growth rate (CAGR) of 10.15% underpin projections into 2032—creating both clear opportunities and actionable risks for suppliers, OEMs, and materials investors.

Worldwide High Purity Silicon Nitride Powder Market

Our aggregated market model shows a pronounced expansion phase as Si3N4 transitions from specialty to more mainstream high-performance applications. The market recorded steady year-on-year growth through 2020–2025 and, with a projected CAGR of 10.15% across the 2026–2032 forecast, the total addressable market is expected to roughly double again by the end of the forecast period. For 2026 decision-makers, this trajectory translates into three concrete strategic implications:

Worldwide High Purity Silicon Nitride Powder Market

Si3N4 production remains feedstock-dependent, primarily on high-purity silicon metal and specific nitridation or imide-decomposition routes. In late 2025, we observed easing silicon metal pricing and lower freight pressures that temporarily improved upstream cost structures. However, these transient gains occur alongside rising environmental and energy-efficiency requirements—especially in Asia-Pacific jurisdictions—meaning producers face a dual mandate: secure cost-stable feedstock channels while investing in cleaner, more energy-efficient operations.

Worldwide High Purity Silicon Nitride Powder Market

For 2026 strategies, buyers and producers should not treat raw-material pricing swings as the only lever. Instead, actions that materially reduce unit cost and supply risk include strategic long-term offtakes, near-shoring portions of feedstock procurement, and co-investments in energy-efficiency retrofits at existing plants. Our scenario analyses show that these moves significantly improve resilience against cyclical raw-material volatility and regulatory tightening.

The market remains concentrated: the top three players account for a substantial portion of global supply, and the five largest suppliers represent an even larger share—conditions that favor incumbents with established production know-how and customer relationships. That concentration creates differentiated roles for players across the value chain:

Recent industry moves reinforce this dynamic. A leading Japanese manufacturer announced a material capacity expansion in early 2026—an approximately 500 metric-ton-per-year increase scheduled to come online in 2027—underscoring incumbent intentions to lock in mid-term supply and meet growing demand from electrification and high-reliability segments. Across regions, investments in process refinement, impurity control, and sinter-friendly morphologies are the primary competitive levers.

Governments are increasingly explicit about the strategic importance of advanced ceramic feedstocks. For example, certain national catalogues now list high-purity silicon nitride among technologies encouraged for building-material and advanced-ceramics promotion—an endorsement that can accelerate industrial adoption through government procurement and standards alignment. At the same time, environmental regulations and energy-efficiency standards are tightening production envelopes, particularly in parts of Asia-Pacific, pushing manufacturers toward capex commitments for emissions control and process modernization.

The combination of policy support for application adoption and heightened production compliance expectations creates a bifurcated investing environment: those who can fund process upgrades will benefit from expanding demand and protect margins, while those who cannot will face rising compliance costs and potential loss of market access.

This report is intentionally prescriptive. Beyond market sizing and trend narratives, PW Consulting provides a suite of operational tools designed for immediate use by procurement, product development, and M&A teams:

Many stakeholders will treat 2026 as a continuation of the growth story—but this is a year where strategic choices will crystallize competitive positions for the next five years. The combination of structural demand growth, concentrated supply, and intensifying regulatory requirements means late movers risk being locked out of high-value supply chains. Conversely, tailored investments in production quality, feedstock security, and regulatory compliance can create durable advantages.

Our advisory work extends beyond deliverables. We provide rapid in-market validation, supplier technical audits, structured negotiation support, and transaction due diligence. For clients committing to scale or to secure strategic supply, we offer implementation programs that align capex sequencing, supplier collaboration models, and risk-mitigation frameworks—turning market insight into executable commercial outcomes.

To access the full intelligence suite, including proprietary segment data, supplier scorecards, process-cost curves, and executable playbooks, visit the PW Consulting report page for the Worldwide High Purity Silicon Nitride Powder Market. The report is structured to support board-level decision making and operational implementation across procurement, manufacturing, and product development functions.

For detailed analysis of this topic, please visit the official page:Worldwide High Purity Silicon Nitride Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com