Worldwide Non-GMO Textured Soybean Protein Market: Strategic Imperatives for 2026 — A PW Consulting Preview

Executive Snapshot

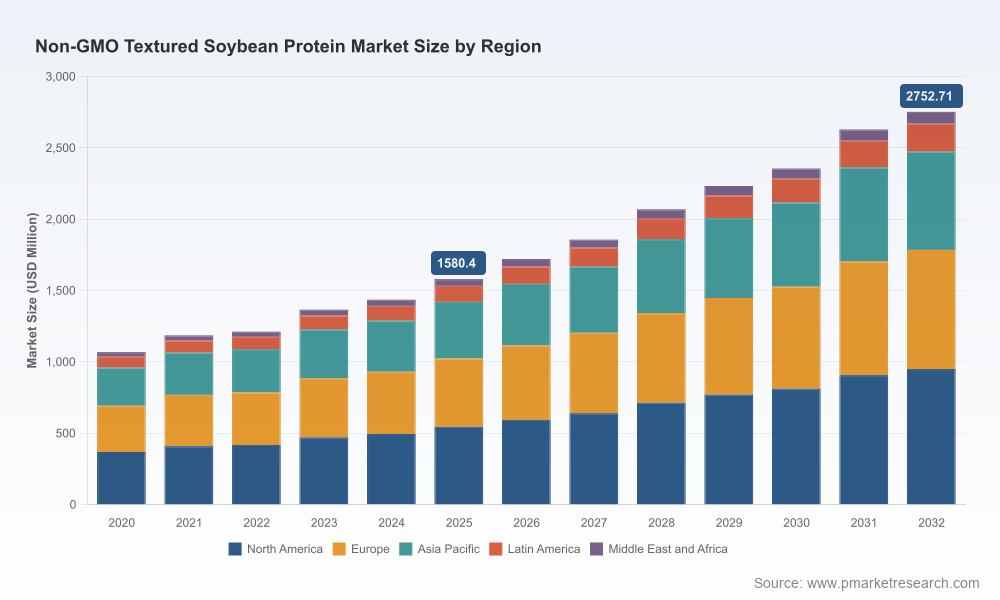

As food manufacturers, ingredient suppliers, and investors chart roadmaps for 2026, the non-GMO textured soybean protein (TSP/TVP) market is transitioning from niche sustainability play to an operationally strategic ingredient class. Our forthcoming Worldwide Non-GMO Textured Soybean Protein Market report—anchored on a 2025 base year and projecting through 2032—shows a robust compound annual growth rate of 8.24% and an enlarging market footprint year-on-year. This preview outlines the strategic value the full report delivers to decision-makers while intentionally withholding granular segment-level figures to encourage engagement with the primary report for executable detail.

Worldwide Non-GMO Textured Soybean Protein Market

Why 2026 Is a Pivotal Year

- The market is entering a phase where steady demand growth converges with supply-side restructuring. The 2025 market base and 2026 forecast indicate both momentum and a window for strategic positioning before competitive consolidation accelerates.

- Regulation, identity-preserved sourcing, and certification expectations are elevating procurement complexity. Firms that act in 2026 to secure traceable supply chains and certification-ready SKUs will materially reduce time-to-market for clean-label product launches.

- Recent capacity additions and upgraded processing footprints are changing regional supply dynamics and margin profiles. The industry is moving from spot buys to longer-term commercial sourcing strategies focused on reliability and provenance.

Market Trajectory: Macro View

PW Consulting’s topline model shows the global non-GMO textured soybean protein market expanding meaningfully from the 2025 base into 2026 and beyond. The forecast period (2026–2032) captures both near-term cyclical factors and structural tailwinds—plant-based protein adoption, reformulation of processed foods, and growing clean-label preferences in mature markets. These drivers underpin the mid-single-digit to low-double-digit annual growth implied by the 8.24% CAGR embedded in our model and support continued investment logic for ingredient processors and downstream formulators alike.

Worldwide Non-GMO Textured Soybean Protein Market

Key Demand Drivers

- Plant-based protein innovation: TSP/TVP remains a cost-effective, versatile platform for meat and dairy alternatives, offering formulators texture, bite, and protein density at scale.

- Clean-label and provenance expectations: Retailers and consumers increasingly demand third-party verification and identity-preserved (IP) sourcing, lending a competitive edge to suppliers who can demonstrate traceability.

- Rising application diversity: Beyond traditional meat analogues, formulators are integrating textured soy proteins into snacks, bakery, and pet food segments—broadening overall addressable demand.

Supply-Side Dynamics and Raw Material Constraints

Supply dynamics in 2025–2026 are characterized by constrained non-GMO soybean acreage relative to commodity production, requiring suppliers to manage identity-preserved supply lines and working capital differently than in traditional soy markets. Farm-level premiums and contract volumes for non-GMO food-grade soy introduce an additional procurement layer that impacts cost curves for textured protein producers. For firms that can align contracting, processing, and certification timelines, the result is enhanced margin predictability and reduced formulation risk.

Worldwide Non-GMO Textured Soybean Protein Market

Regulatory & Certification Landscape

Non-GMO textured soybean protein’s commercial acceptance increasingly depends on IP programs and third-party certifications. Recognition of certification schemes and the operational burden of maintaining IP status vary across geographies, but the commercial imperative is clear: buyers are paying for verified provenance. Navigating the mosaic of Non-GMO Project, ProTerra, and other standards requires procurement, quality, and regulatory teams to collaborate closely; those that do will unlock premium channels and mitigate recall/regulatory exposure.

Competitive Landscape: Who Matters and Why

The market concentration profile shows a moderately consolidated industry: the top three and five suppliers occupy a meaningful, but not overwhelming, share of global supply. This structure creates space for both global integrators and regional specialists to compete on different value propositions—scale, IP sourcing, certification, specialty formulations, and service.

- Archer Daniels Midland Company (ADM): ADM’s decades-long investment in textured soy protein technology, combined with strategic acquisitions geared at non-GMO supply in Europe, positions it as a global anchor supplier. Its breadth of conventional, IP non-GMO, and organic offerings enables cross-regional customer programs, especially for global CPG customers requiring consistency.

- Bunge Global SA: Recent commissioning of an integrated facility in the U.S. adds both volume and non-GMO capability. New mid-to-high-protein product lines and upgraded scale shift Bunge from regional supplier to a more direct competitor for food processors seeking U.S.-sourced non-GMO concentrates and textured variants.

- Cargill: With a portfolio that emphasizes application-ready shaped TVP and partnerships for IP sourcing, Cargill is focused on application engineering—helping formulators transition prototypes into scalable SKUs for patties, meatballs, and snack inclusions.

- International Flavors & Fragrances (IFF): IFF’s premium positioning through Farmer-to-Customer IP programs and certified sourcing from Brazil addresses the upper end of the market—customers seeking differentiated taste and traceability credits in their branding.

- Regional and specialty producers (Foodchem, Gushen, Shandong Yuxin, MT Royal, Groupe Berkem, Soya Food): These companies supply flexibility, local compliance, and certification variants (Halal/Kosher/organic). They play a critical role in regional supply continuity and niche formulations.

Collectively, these suppliers are shaping a competitive environment where technical service, certification infrastructure, and supply-chain transparency are as important as price per protein unit.

Recent Developments Shaping 2026 Planning

- Capacity expansions and greenfield processing (notably a new integrated U.S. facility commissioned in 2025) are altering inbound logistics and reducing lead times for North American supply chains.

- Shifts in farm-gate behavior and contracted acreage for non-GMO food-grade soy introduce planning complexity. Buyers need to model procurement scenarios that reflect seasonal variability and contract leakage risk.

- The rising prominence of IP and third-party certification programs has increased compliance costs but also created a value ladder where certified origin stories secure premium shelf positioning.

Strategic Imperatives for 2026 Decision-Makers

For executives responsible for supply, innovation, and M&A, 2026 offers distinct actions with asymmetric upside:

- Secure identity-preserved supply chains now. Locking in multi-year contracts with performance clauses and cooperative agronomy programs will de-risk product roadmaps and protect margin against spot volatility.

- Invest in application engineering capabilities. Differentiated textured formats and co-innovation with ingredient customers shorten product development cycles and increase switching costs for buyers.

- Prioritize certification and traceability systems. Implementing scalable IP tracking and aligning with recognized third-party schemes accelerates market entry in premium channels and reduces commercial friction with retail customers.

- Evaluate strategic bets across the value chain. Consider targeted capacity additions, joint ventures with regional processors, or bolt-on acquisitions to gain faster access to certified non-GMO throughput and to lock geographic supply.

- Embed scenario planning into sourcing functions. Model implications of acreage shifts, premium volatility, and logistics disruptions to ensure continuity for key customers.

What the Full PW Consulting Report Delivers

The complete report translates market dynamics into operational playbooks and executable commercial insights. Highlights include:

- Topline market sizing and forward-looking scenarios through 2032, reflecting different adoption and supply assumptions.

- A practical procurement guide for establishing identity-preserved contracts, including contracting structures, quality control checkpoints, and audit-ready documentation templates.

- Detailed supplier profiles and competitive benchmarking across capability vectors: capacity, certification coverage, product forms, application engineering, and go-to-market agility.

- Case studies of successful product launches that leveraged non-GMO textured soy protein to achieve rapid retail entry, including practical formulation notes and cost considerations.

- Regulatory and certification playbook that maps compliance requirements to commercial outcomes by major market—presented as decision matrices and implementation timelines.

- Interactive scenario tools (proprietary models) that allow users to stress-test procurement strategies against variations in acreage, premiums, and demand growth.

How PW Consulting’s Analysis Adds Strategic Value

We combine high-resolution market modeling with on-the-ground supplier intelligence to produce recommendations that are both defensible and implementable. For 2026, our analysis helps executives answer three critical questions:

- Where should we anchor supply to balance cost, reliability, and provenance?

- Which product formats and value-added services will create commercial differentiation in the next 12–24 months?

- What combinations of organic growth, partnerships, and M&A will generate the quickest path to scale for non-GMO textured soy protein offerings?

Next Steps and Access

This release serves as a strategic primer. The full report contains the granular, actionable intelligence required to convert insight into competitive advantage—contract templates, supplier scorecards, SKU-level formulation levers, and scenario modeling assets. To access the complete dataset, segmentation tables, and proprietary models that underpin these findings, please visit our report page or contact PW Consulting’s research team for a customized briefing.

PW Consulting remains committed to helping clients translate macro trends into robust, risk-adjusted business plans. In a market where provenance, processing, and product innovation determine winners, 2026 is the year to move from planning to execution.

For detailed analysis of this topic, please visit the official page:Worldwide Non-GMO Textured Soybean Protein Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com