Worldwide Semiconductor Consumables Market 2026: Strategic Imperatives for Boards and Sourcing Leaders

PW Consulting's latest market study on the Worldwide Semiconductor Consumables Market frames 2026 as an inflection year for buyers, manufacturers and investors in the consumables ecosystem. Drawing on a six‑year historical run (2020–2025) and a rigorous forecast to 2032, the report quantifies the market's structural momentum — a compound annual growth rate (CAGR) of 6.99% from the 2026 baseline — while translating that momentum into actionable choices for enterprise leadership.

Worldwide Semiconductor Consumables Market

Why 2026 matters: macro trajectory and strategic urgency

After recovering from cyclical pressures in the early 2020s, the global consumables market reached approximately USD 77.6 billion in the 2025 base year and is projected to exceed USD 124.5 billion by 2032 under the central case. The forecasted 6.99% CAGR masks important nonlinearities: near‑term demand spikes tied to AI/HPC architectures, persistent supply‑side bottlenecks in critical minerals and extended lead times for specialized parts combine to compress planning horizons for semiconductor fabs and their vendors. For decision‑makers, that means 2026 is no longer a ‘steady state’ planning year — it is a transition year for re‑architecting procurement, capacity strategy, and risk mitigation.

Worldwide Semiconductor Consumables Market

Report scope and practical content

- Comprehensive market sizing and a seven‑year forecast (2026–2032) with scenario analysis calibrated to technology adoption curves and capacity buildout assumptions.

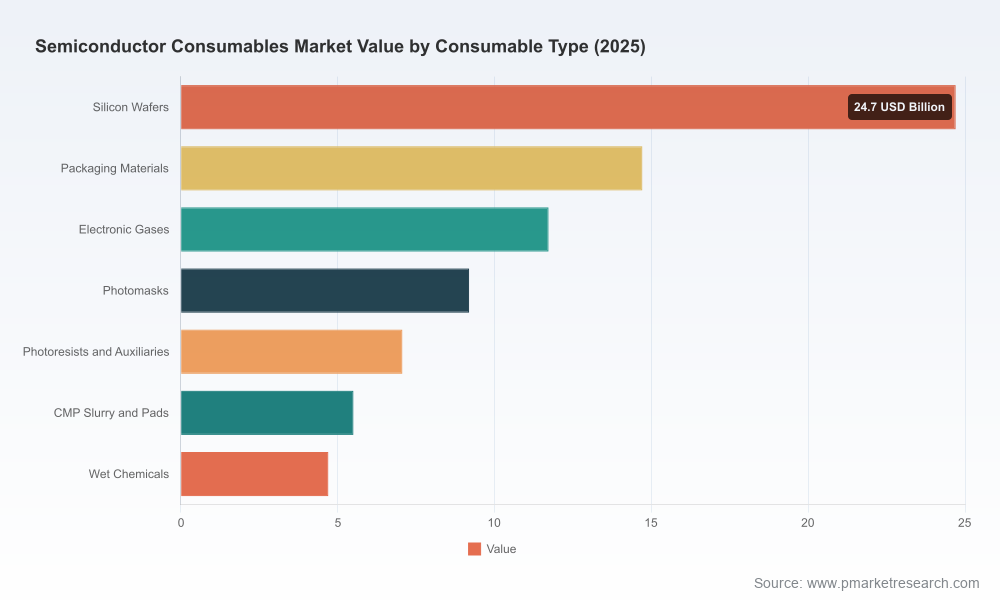

- End‑to‑end supply chain maps for key consumable groups — from wafers and packaging substrates to probe/test consumables, electronic gases, and wet chemistries — together with supplier tiering and service propositions.

- Procurement playbooks and model contracts addressing inventory buffers, long‑lead ordering, buy‑side quality assurance and certification practices to reduce yield loss and process downtime.

- Regulatory and trade impact assessments, including compliance checklists and tax/incentive overlays for build‑out and reshoring programs.

- Competitive benchmarking and acquisition target shortlists, supported by financial sensitivity models and integration risk scores.

- Practical tools for chief procurement officers and plant directors: TCO calculators, supplier risk heatmaps, and a stepwise action plan for 90/180/360‑day horizon moves.

Competitive structure: concentrated but dynamic

The consumables market displays notable concentration: the top three suppliers account for a substantial share of market revenue, while the top five capture over half of industry sales. That concentration reflects the high technical barriers and quality requirements inherent to contamination control, wafer handling and high‑precision test consumables. Yet concentration coexists with pockets of fragmentation — particularly among niche suppliers of specialty chemistries and regional carriers — creating opportunities for selective M&A and partnership plays.

Worldwide Semiconductor Consumables Market

Key strategic profiles highlighted in the report include:

- Entegris, Inc. (Billerica, MA) — a materials‑handling and contamination control leader whose integrated product and systems portfolio makes it a preferred partner for yield‑sensitive fabs. Entegris’s strength in filtration, fluid management and wafer handling positions it favorably as fabs chase incremental yield gains.

- Shin‑Etsu Polymer (Tokyo) — a specialist in high‑purity wafer containers and front‑end packaging solutions; its focus on contamination‑resistant transport and cleanroom‑compatible packaging aligns with tight particle budgets at advanced nodes.

- FormFactor (Livermore, CA) and Technoprobe (Cernusco Lombardone, Italy) — leaders in probe cards and test consumables, crucial for high‑parallelism testing strategies required by advanced logic, memory and heterogeneous integration.

- Miraial, Micronics Japan, Japan Electronic Materials (JEM) and MPI — regional and product‑focused players that supply wafer carriers, probe cards and test peripherals, often offering rapid local support and niche product differentiation.

For strategic buyers, the competitive mix implies a two‑track sourcing strategy: maintain long‑term partnerships with system‑level suppliers for mission‑critical consumables while qualifying a broader set of regional specialists to shorten lead times and provide redundancy.

Regulation, raw materials and the new supply‑risk calculus

The policy and raw‑material landscape has changed materially, and the report integrates the most consequential developments for 2026 planning:

- Export controls and licensing regimes for critical minerals have tightened in several jurisdictions, producing acute price and availability volatility for inputs used across consumable categories. In some cases, prices for constrained minerals have spiked dramatically in a short interval, altering supplier cost structures and procurement economics.

- Geopolitical trade measures and targeted procurement restrictions are reshaping supplier eligibility for government contracts and certain high‑security programs. These rules are driving some purchasers toward supplier re‑certification and geographical diversification to avoid disqualification.

- Extended lead times — in some categories approaching many months — combined with rising costs for energy, logistics and specialty chemicals are driving fabs to re‑examine inventory policies, hedging approaches and local capacity investments.

Our scenario modules quantify the impact of these disruptions on delivery times, unit costs and project IRR for new fab support facilities. For boards and CFOs considering CAPEX for captive consumables manufacturing, the report provides a stepwise ROI threshold matrix linked to tariff incentives and local industrial policy support.

Technology and demand drivers: where consumables matter most

Demand for consumables is being pulled by two broad structural forces. First, the rapid deployment of high‑performance computing and AI workloads is intensifying requirements for memory and advanced packaging, which in turn elevates consumption per wafer for certain specialty items. Second, the diversification of compute away from monolithic nodes toward advanced packaging and heterogeneous integration changes the mix of consumables used in front‑end and back‑end processes. The report maps these demand shifts against technology adoption timelines so procurement teams can prioritize capital investments and qualification cycles.

Practical recommendations for 2026 decision cycles

- Recalibrate inventory strategies from days‑of‑supply to scenario‑based safety stock. Adopt multi‑tier reorder logic that differentiates between mission‑critical, long‑lead consumables and commoditized items to avoid excess working capital.

- Institute a supplier‑segmentation program that blends strategic single‑source partnerships (for system and integration performance) with a resilient second‑source network for critical inputs and test consumables.

- Pursue near‑term qualification of regional providers and invest in accelerated co‑validation programs; public incentives and local demonstration centers are lowering the hurdle for localized validation tracks in several markets.

- Hedge raw‑material exposure through blended sourcing and selective long‑term offtake agreements; concurrently, fund materials R&D and substitution assessments where feasible to reduce dependency on constrained minerals.

- Embed regulatory forward‑scanning and export‑control screening into procurement workflows so supplier eligibility risks can be surfaced before contract award.

- Explore value capture via vertical integration only where unit economics are compelling and supply risk is systemic — use our provided ROI matrix to test scenarios before committing CAPEX.

Case in point: infrastructure and verification ecosystems

Recent regional initiatives illustrate how infrastructure investments can reshape consumables dynamics. The report examines a newly announced demonstration center dedicated to consumable performance verification and certification. Facilities like this reduce qualification times for new suppliers and accelerate adoption of mass‑production formats. For strategic planners, these centers are both a risk mitigant and an opportunity: they can lower entry barriers for regional players, but they also compress time‑to‑certification for global incumbents.

What the report hides (and why you should read it)

In keeping with our "trailer" approach, this briefing deliberately outlines the strategic contours without disclosing granular, segment‑level market shares or dollar‑by‑region breakdowns. The full report contains detailed split models by consumable type, region, and end use; supplier scorecards with product‑level revenues; and downloadable scenario models that allow practitioners to stress‑test procurement and investment decisions under alternative policy and commodity price paths.

How to use this analysis in your 2026 planning cycle

- Boards: Use the report’s scenario outputs to evaluate capital deployment options, partner strategies, and M&A candidacy tied to supply‑chain resilience.

- CFOs: Leverage TCO and ROI matrices to compare buy vs. build for captive consumables, and to prioritize incentive capture from industrial policy programs.

- Chief Procurement Officers: Adopt the procurement playbooks and supplier risk dashboards to tighten lead‑time control and to re‑engineer qualification timelines.

- R&D and Operations: Apply the validation roadmaps and contamination control checklists to shorten time to yield for new process nodes and packaging formats.

PW Consulting’s Worldwide Semiconductor Consumables Market report is designed to be both a defensible market reference and an operational toolkit for 2026 decisions. For access to the full dataset, segmented forecasts, supplier scorecards and downloadable models, please visit the PW Consulting report page or contact our industry practice to arrange a bespoke briefing and licensing options.

For detailed analysis of this topic, please visit the official page:Worldwide Semiconductor Consumables Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com