Polydimethylsiloxane (PDMS) Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-29 10:09:17

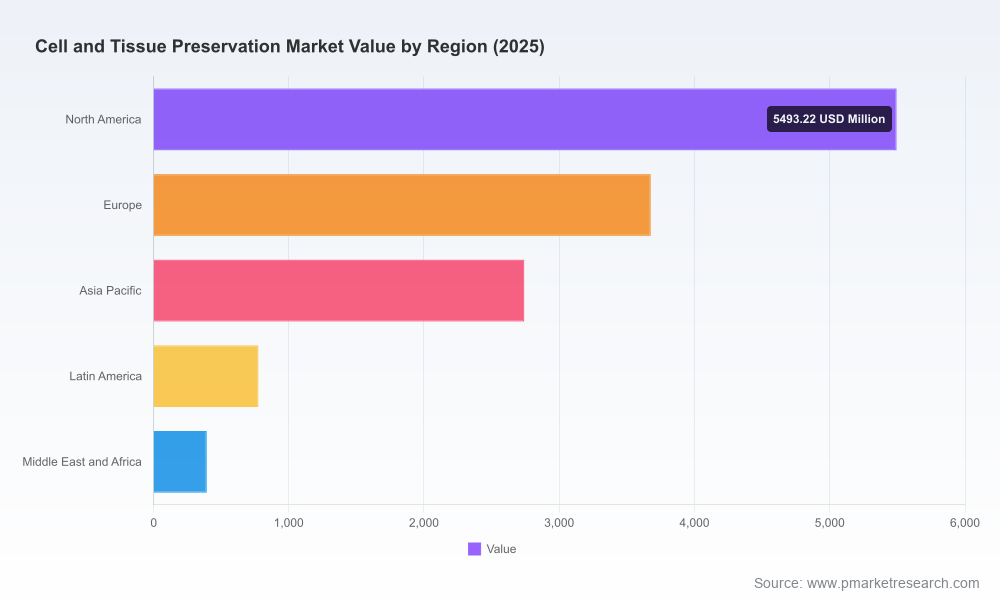

As cell- and tissue-based therapies move from bench to bedside and biobanking scales to support precision medicine pipelines, preservation solutions have become a strategic fulcrum for product integrity, cost control, and regulatory compliance. PW Consulting’s new market study places the global cell and tissue preservation industry at approximately USD 13.08 billion in the 2025 base year and projects continued rapid expansion through the 2026–2032 forecast window at a compound annual growth rate of 11.8%, reaching an anticipated market size in the late 2030s’ forecast horizon. For corporate leaders planning capital allocation, commercial strategy, or M&A in 2026, this report provides the actionable market intelligence required to convert growth opportunity into defensible commercial outcomes.

Worldwide Cell and Tissue Preservation Market

Timing matters — 2026 is a pivot year for adoption curves: cell- and gene-therapy manufacturing continues to broaden beyond early adopters, while clinical-grade preservation workflows are increasingly embedded into late-stage clinical programs. Companies that align supply, regulatory readiness, and clinical logistics in 2026 will capture outsized share as the market accelerates.

Worldwide Cell and Tissue Preservation Market

Macro clarity — our study synthesizes demand drivers, technology adoption roadmaps, and supplier economics across the preservation stack (equipment, media, consumables and services). We quantify the scale of the opportunity and model realistic scenarios that stress-test revenue and margin outcomes against adoption and regulatory scenarios.

Worldwide Cell and Tissue Preservation Market

Regulatory and standards inflection — with CBER’s guidance agenda and targeted ISSCR updates, manufacturers and service providers face evolving compliance expectations that materially affect product design, qualification testing, and sourcing of human- or animal-derived inputs. The report maps those regulatory vectors to commercial impact and timelines.

Executive synthesis and scenario models: clear base, upside, and downside cases for 2026–2032 that incorporate demand shocks, reimbursement sensitivity, and regulatory milestones so executives can stress-test strategic plans.

Supplier and technology scorecards: comparative matrices that evaluate vendors across technical performance, cGMP readiness, supply-chain resilience, and commercial footprint — designed for rapid shortlisting during procurement and diligence.

Regulatory readiness playbook: an actionable checklist aligned to FDA CBER priorities (including recent draft finalizations affecting allogeneic products and raw-material sourcing), with recommended submission strategies and mitigation levers for materials-of-origin concerns.

Cold-chain and operational optimization toolkit: unit-economics templates, temperature-mapping best practices, and validated packaging/transport trade-offs to lower touch-points, reduce Viability Loss Events, and tighten total landed cost.

M&A and partnership diligence briefings: target filters, valuation sensitives, and integration risk heatmaps focused on preservation media platforms, cryogenic hardware, and adjacent logistics players.

Commercial go-to-market accelerators: customer segmentation frameworks, pricing playbooks, and pilot-to-scale progression maps that shorten sales cycles for suppliers and end-users alike.

The market is characterized by established life-science suppliers extending from broad portfolios and specialist firms focused on proprietary media and clinically validated platforms. Competitive positioning is being shaped by technical differentiation (formulation and reproducibility), regulatory pedigree (cGMP and clinical use cases), and logistics capability (cold-chain and clinical supply support).

Thermo Fisher Scientific Inc. — Leverages a broad portfolio spanning culture media, cryogenic storage equipment, and integrated workflow services. Strengths include global distribution scale and deep service capabilities for clinical and research customers; strategic value lies in bundling equipment with consumables and managed services to deepen customer lock-in.

Merck KGaA (MilliporeSigma / Sigma-Aldrich) — Competes on reagent depth and institutional relationships. Expect continued emphasis on GMP-grade reagents and co-development with biomanufacturers to address materials-of-origin scrutiny and supply-traceability demands.

BioLife Solutions Inc. — A category specialist with recognized brands in CryoStor® and HypoThermosol® and ongoing corporate messaging that frames the company as a cell-preservation leader. Recent investor presentations and product updates through 2025–2026 reaffirm positioning in clinical workflows and point to focused expansion of applicability across cell-therapy manufacturing and cold-chain transport markets.

Lonza Group — Brings strengths in cell- and gene-therapy manufacturing support and GMP-grade media; strategic plays likely emphasize upstream/downstream integration for therapy developers seeking single-supplier simplicity.

BD (Becton, Dickinson and Company) — Focused on consumables and processing tools; competitive advantage is in consumable design and field-installed instrument networks that serve clinical sites and hospital labs.

Cytiva (Danaher) and Sartorius AG — Both positioned around bioprocessing equipment and media that enable scalable preservation within manufacturing environments; watch for cross-selling into biomanufacturing value chains.

Corning, STEMCELL Technologies, FUJIFILM Irvine Scientific, Avantor, AMSBIO, CellGenix — Each brings niche strengths: cultureware and containers (Corning), stem-cell specific formulations (STEMCELL), reproductive and therapy-optimized media (FUJIFILM), distribution scale (Avantor), research-focused kits (AMSBIO), and GMP-grade therapy media (CellGenix).

BioLife’s late-2025 product messaging and January 2026 investor materials emphasize integration of preservation platforms into cell-therapy workflows and an expanding addressable market for biopreservation tools — an indicator that specialty media providers are migrating from niche laboratory use into clinical supply chains.

Regulatory action: the FDA CBER 2026 agenda signals forthcoming finalizations on materials-of-origin considerations and safety testing of allogeneic cells. Organizations must accelerate raw-material traceability programs, qualify alternatives to animal-derived inputs, and update comparability strategies to de-risk clinical timelines.

Standards update: the ISSCR 2025 targeted revision highlights the sector’s evolving ethical and scientific guardrails. For firms working with stem-cell-based models, updated translational criteria will affect proof-of-concept timelines and may reshape repository consent structures.

Reimbursement reality check: no discrete CPT or DRG codes emerged in 2025–2026 for preservation media or consumables, underscoring that clinical adoption will be driven primarily by demonstrated clinical utility, operational savings, and manufacturer contracting rather than new procedural reimbursement.

For therapeutics manufacturers: lock down dual-sourcing for critical preservation inputs and prioritize suppliers with cGMP credentials and cold-chain logistics capabilities. Run a 90–180 day accelerated qualification for at least one alternative supplier.

For suppliers: invest in documented clinical performance data and extend service offerings (training, cold-chain management) to escape pure product commoditization and elevate lifetime customer value.

For biobanks and clinical sites: implement preservation–to–analytics audits that quantify viability retention and downstream data quality gains; use the findings to negotiate outcome-based supplier contracts.

For investors and M&A teams: prioritize targets with differentiated formulation IP, GMP readiness, and existing pathways into clinical supply — and demand transparent supply-chain traceability given regulatory focus on materials-of-origin.

Key upside drivers include broader clinical adoption of cell therapies, increased biobanking for population-scale initiatives, and improvements in formulation science that reduce post-thaw viability losses. Principal risks are regulatory tightening around biological inputs, supply-chain concentration for critical reagents, and potential commoditization of legacy media absent clinical differentiation. The market demonstrates meaningful leadership by several incumbent players but remains open to innovation-led entrants — making 2026 a high-leverage year for establishing durable competitive moats.

Step 1 — Executive briefing: align the board and C-suite on the report’s scenarios and choose the preferred strategic path (protect, expand, pivot).

Step 2 — Rapid supplier audit: deploy our supplier scorecard during Q1–Q2 2026 to identify single points of failure and negotiate contingency agreements.

Step 3 — Pilot and scale: select a clinical site or manufacturing line for a preservation-optimization pilot; measure viability, cost per dose, and logistics incidents to build a quantified business case for scale.

Step 4 — Regulatory harmonization: integrate the regulatory readiness playbook into submission timelines and raw-material sourcing policies to reduce inspection and approval risk.

PW Consulting’s Worldwide Cell and Tissue Preservation Market report provides the full set of forecast models, vendor scorecards, regulatory timelines, and operative templates required for execution. This briefing is a strategic preview designed to show the analytical approach and decision-ready tools; core segment-level tables, regional breakdowns, and detailed numeric appendices are intentionally reserved for the full report. To access the complete study and our interactive scenario models, visit the PW Consulting report page or contact your PW Consulting account team for an executive briefing and sample datasets.

For detailed analysis of this topic, please visit the official page:Worldwide Cell and Tissue Preservation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com