Worldwide Metallocene Based Polyethylene Market: Strategic Imperatives for 2026 — PW Consulting Official Release

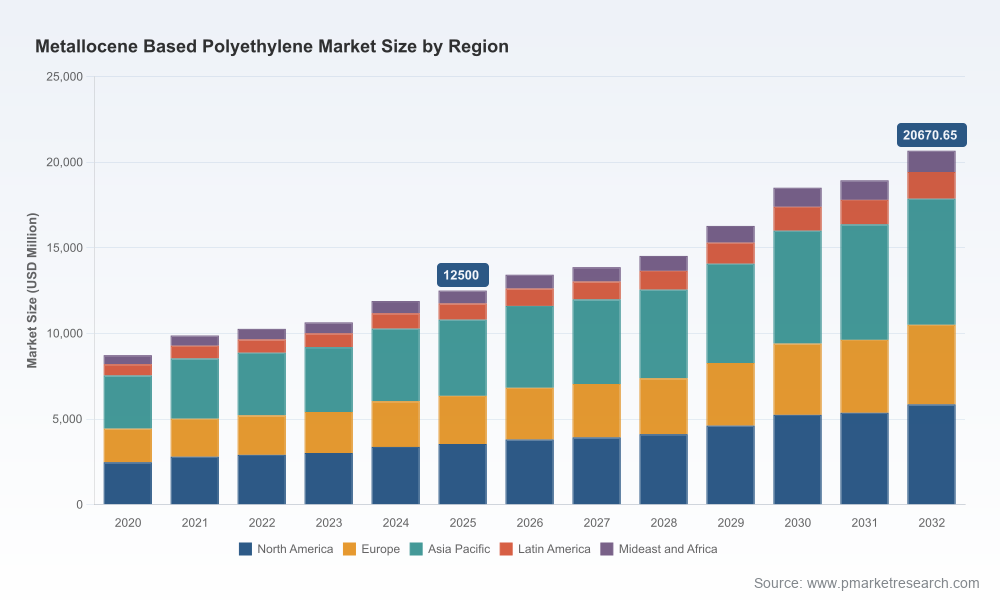

PW Consulting today releases its authoritative industry briefing accompanying the new Worldwide Metallocene Based Polyethylene Market research report. The sector reached an estimated total market size of USD 12,500 Million in the report base year (2025) and, driven by continued substitution into higher-performance film and specialty extrusion applications, is forecast to expand at a compound annual growth rate (CAGR) of 7.45% through the 2026–2032 horizon, arriving at a materially larger market by 2032. This briefing highlights the strategic value of the full study for corporate decision-makers preparing investments, commercial strategies, and risk mitigation plans in 2026 — and explains why detailed, granular intelligence from the full report will be decision-critical.

Worldwide Metallocene Based Polyethylene Market

What the report delivers — actionable, transaction-ready intelligence

- High-resolution market sizing and demand modeling: annualized historic baselines (2020–2025), bottom-up demand construction by polymer family and application, and seven-year scenario forecasts (2026–2032) with sensitivity to feedstock and regulatory shocks.

- Supply-chain and capacity analysis: plant-level capacity maps, recent and announced capital projects, and utilization scenarios that quantify likely shortfalls and surpluses under alternative demand paths.

- Pricing and margin analytics: input-cost pass-through modeling linked to ethylene and energy price scenarios, plus freight and logistics stress tests.

- Regulatory and sustainability matrix: implications of emerging restrictions and recycled-content mandates, certification pathways (e.g., ISCC), and design-for-recyclability trade-offs for metallocene formulations.

- Competitor playbooks and M&A opportunity screens: strategic profiles for global producers, scenario-driven market concentration analysis, and prioritized targets for bolt-on investments or joint ventures.

- Commercial strategy templates: go-to-market segmentation for high-growth applications, value-based pricing levers, and win-the-bid recommendations for film, agricultural, and industrial customers.

Why this matters for 2026 decision-makers

- Managing feedstock volatility: In Q4 2025 ethylene spot averaged approximately $0.85/kg, an increase year-on-year tied to regional supply disruptions. The report quantifies direct-margin exposure across product grades and presents hedging and sourcing strategies that protect profitability under multi-scenario ethylene price paths.

- Navigating regulatory inflection points: New restrictions on catalyst residues for food-contact polyethylene under EU REACH (effective January 2026) and regional recycled-content mandates (for example, legislated targets in California) create compliance costs and reformulation imperatives. The study maps reformulation costs by grade and identifies fast-follow pathways for maintaining food-contact and packaging qualifications.

- Trade and logistics risks are no longer benign: Recent trade actions and transport bottlenecks — including countervailing duties imposed on certain imports and freight surcharges on key domestic corridors — materially change the competitiveness calculus for export-oriented plants and for regional sourcing strategies. The report models the break-even economics of local investment versus import dependence under duty and surcharge scenarios.

- Certification and circularity unlock commercial premiums: Certification achievements by major suppliers (for example, ISCC PLUS designations announced in 2025) are already influencing procurement decisions among brand owners. Our research defines the price premium thresholds for certified and recycled-content metallocene PE and quantifies payback timelines for certification investments.

Competitive dynamics — how leading producers are positioning

The market exhibits moderate concentration, with the largest three producers accounting for a significant portion of capacity and the top five materially more. This market structure creates room for both scale plays and focused differentiation strategies.

Worldwide Metallocene Based Polyethylene Market

- LyondellBasell: Recent announcements to expand metallocene LLDPE capacity in Europe signal a low-cost scale play to capture film and packaging growth. The expansion will pressure regional spot markets and alters project economics for late-moving competitors. Strategic implication: incumbents and new entrants must recalibrate capacity timing or pursue niche differentiation to avoid margin deterioration.

- Dow Inc.: With moves toward circularity — including ISCC PLUS certification achievements — Dow’s playbook centers on premium positioning for certified, high-performance films and adhesives. For customers, the strategic question is whether to partner with certified suppliers or accelerate in-house circular formulations; the full report provides supplier scorecards to guide that decision.

- ExxonMobil Chemical and SABIC: Both companies continue to refine metallocene portfolios with performance-driven grades for high-strength films and high-speed cast extrusion. SABIC’s new grade introductions in 2025 demonstrate the speed-to-market advantage of pipeline R&D; the study evaluates the commercial lift for new grades versus the cost of market education.

- Regional champions and diversified producers (Borealis, INEOS, TotalEnergies, Prime Polymer, LG Chem, Reliance): These firms mix local scale with targeted innovation. The analysis includes a comparative matrix that highlights geographic exposure, feedstock integration, and product-development agendas — critical inputs for strategic sourcing and alliance decisions.

Recent events that change investment logic

- Capacity expansions announced in late 2025 will compress regional margins unless demand growth accelerates; the report’s utilization scenarios quantify the timeline for re-balancing.

- New product launches and certifications in 2025 enhance supplier differentiation but increase complexity for procurement teams seeking consistent, compliant supply across regions.

- Trade measures and logistics surcharges implemented since late 2025/early 2026 create immediate arbitrage opportunities — and discrete supply risks — that need to be stress-tested in any capital planning exercise.

Key strategic recommendations for 2026

- Conduct a 48–72 month supply-scenario stress test before committing to greenfield capacity. Use the report’s demand scenarios to compare outcomes under high-growth, base, and downside assumptions.

- Accelerate feedstock risk mitigation: pursue multi-sourced ethylene contracts, explore tolling arrangements, and size derivative hedges aligned to the company’s exposure curve described in our margin-sensitivity toolkit.

- Prioritize certification and recycled-content pathways where customer willingness to pay exists — especially for brand-sensitive packaging customers. The report contains a segmented elasticity matrix showing where premiums can be captured.

- Optimize regional footprint: re-evaluate import/export strategies in light of recent tariff measures and freight surcharges; consider contractual clauses to pass through logistics cost volatility to end customers where market structure allows.

- Refine product portfolios toward value-adding formulations (elastic films, high-performance cast films, and specialty extrusion) while maintaining a clear playbook for commoditized LLDPE/HDPE exposures.

- Pursue targeted M&A or JV opportunities to acquire feedstock security, local market access, or recycling capabilities — the report identifies priority targets and valuation ranges under multiple return scenarios.

How PW Consulting’s methodology supports confident decisions

The full report combines bottom-up plant and shipment data, primary interviews with procurement and R&D leaders across the value chain, proprietary demand models calibrated to historical performance (2020–2025), and scenarios that reflect near-term shocks (feedstock, regulatory, trade, and logistics). Revenue metrics are presented in USD Million, with the 2025 base year clearly identified, and forecasts constructed for 2026–2032. Our concentration analysis and competitor profiles integrate announced capacity changes and new-grade launches through autumn 2025, ensuring recommendations are grounded in the latest public and proprietary intelligence.

Worldwide Metallocene Based Polyethylene Market

Next steps

For CEOs, CFOs, commercial leaders, and corporate development teams evaluating investments or strategic pivots in 2026, the full Worldwide Metallocene Based Polyethylene Market report is an essential decision tool. It provides the granular supply-demand matrices, price and margin stress tests, and competitor playbooks that cannot be conveyed in a high-level summary. To access the full dataset, model, and executive briefings, contact your PW Consulting account lead or visit PW Consulting’s insights portal for purchasing and advisory options. Our analysts are available to facilitate custom scenario workshops and bespoke valuation assessments tied directly to your strategic planning cycle.

PW Consulting — actionable intelligence for confident industrial decisions.

For detailed analysis of this topic, please visit the official page:Worldwide Metallocene Based Polyethylene Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com