Lingonberry Powder Market Forecast 2026–2036: Global Market to Reach USD 550.0 Million by 2036 at 4.1% CAGR

Food |

2026-03-09 13:18:42

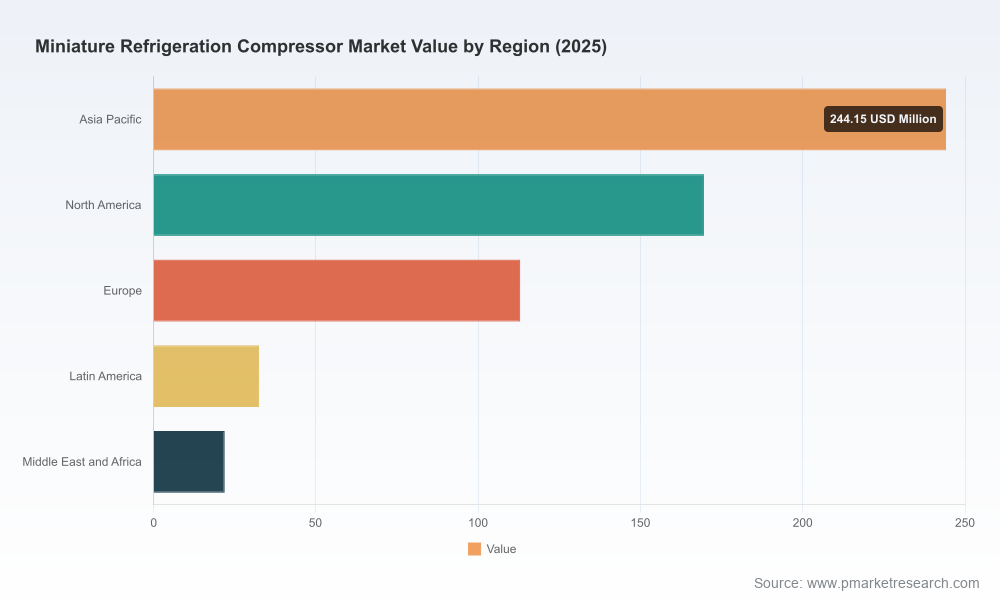

PW Consulting’s latest market intelligence brief on the Worldwide Miniature Refrigeration Compressor market delivers the strategic context and decision-support frameworks that executives and product teams need as they move into 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study frames a market expanding at a compound annual growth rate (CAGR) of 8.52%. The global market valuation crosses the half‑billion USD threshold in the 2025 base year (reported at USD 581.15 Million) and is projected to continue its upward trajectory into a billion‑dollar market by the early 2030s. This release highlights the practical, executable outputs of the full report while intentionally reserving detailed sub‑segment datapoints to encourage direct engagement with the source intelligence.

Worldwide Miniature Refrigeration Compressor Market

Regulatory timing and product roadmaps — 2026 represents a pivot point: new refrigerant classifications and energy-efficiency mandates are forcing product architecture and certification timelines. Companies that align R&D, certification, and manufacturing plans to meet 2026–2027 compliance windows gain first-mover advantage.

Worldwide Miniature Refrigeration Compressor Market

Procurement and supply‑chain risk management — raw material volatility and supplier concentration are driving procurement strategies from shortterm spot buying toward hedged, long‑term agreements and alternative material sourcing.

Worldwide Miniature Refrigeration Compressor Market

Commercial positioning — portable cooling, medical cold chain, electric vehicle refrigeration and electronics cooling are evolving buyer requirements (weight, power consumption, silence, and refrigerant compatibility). This report equips pricing, channel, and product decisions to capture higher-margin niches.

Regulatory push to low‑GWP refrigerants: Regulatory frameworks (including recent AIM Act implementations and international equivalents) are accelerating adoption of low‑GWP refrigerants and creating practical deadlines for A2L refrigerant use in many self‑contained and field‑assembled systems. That technical and compliance burden alters compressor designs, sealing strategies, and service ecosystems.

Efficiency standards and variable‑speed adoption: Energy performance mandates and buyer demand for extended battery life in mobile and portable use cases are increasing the adoption of variable‑speed BLDC compressors and integrated inverter controls.

Raw material pressure: Commodity price volatility—illustrated by copper price movement in early 2026—translates into cost pass‑through pressures and margin compression unless manufacturers hedge or redesign to reduce copper intensity in windings and tubing.

Electrification and mobility: Growth in micro‑refrigeration for electric vehicles, portable medical devices, and last‑mile logistics creates product segmentation opportunities defined by weight, COP (coefficient of performance), and system integration complexity.

Consolidation vs. specialization: The market exhibits a balance between vertically integrated incumbents and specialist micro‑compressor innovators. Market concentration metrics indicate meaningful room for consolidation and strategic partnerships.

PW Consulting’s model quantifies a steady mid‑single‑digit to high‑single‑digit expansion over the forecast window, driven by adoption across portable cooling, medical devices, vehicle refrigeration, and electronics thermal management. With a reported CAGR of 8.52% for the forecast period, buyers and suppliers should plan around sustained demand growth and product premiumization. Market concentration is non‑trivial: our analysis of industry share shows a moderate high‑end aggregation—three‑ and five‑player concentration metrics indicate that leading vendors control a meaningful portion of revenue while leaving competitive space for regional specialists and OEM suppliers. The detailed regional, product‑type, and application splits are presented in the full dataset available through PW Consulting.

Top‑line forecast model (2026–2032) with scenario toggles for high‑/low‑growth and regulatory shock scenarios.

Regulatory compliance matrix mapping refrigerant options (including A2L pathways), certification timelines, and retrofit/field‑service implications for each compressor architecture.

Supplier scorecards and capability heatmaps — engineering, manufacturing scale, IP, refrigerant compatibility, and certification status — built for procurement and corporate development teams.

Raw‑material sensitivity and cost modeling, including copper price stress tests and design alternatives to mitigate exposure.

Product and BOM benchmarking templates to quantify TCO, energy performance, and service lifetime across variable‑speed and fixed‑speed architectures.

Go‑to‑market playbooks for four distinct buyer segments (portable logistics, medical/healthcare, vehicle refrigeration, electronics/industrial), including channel strategies, pricing guidance, and partnership archetypes.

M&A and partnership target lists with a short‑list of acquisition rationales (capability, market access, manufacturing scale) and integration checklists.

We profile market leaders and fast followers across a spectrum from ultra‑compact innovators to global compressor manufacturers. Highlights from our competitive analysis include:

Aspen Compressor (USA): A pioneer in extremely compact rotary compressors with a strong reputation for premium, US‑made products and UL approvals for low‑GWP refrigerants. Their product breadth across single and twin‑cylinder rotary lines positions them well for high‑value, weight‑sensitive applications and customers prioritizing provenance and certification.

RIGID Technology (China): A leader in high power‑density BLDC miniature rotary compressors, offering a wide voltage and capacity range. Their engineering depth and modular micro‑cooling solutions make them a natural partner for OEMs integrating direct‑expansion systems into mobile and battery‑powered platforms.

MOIR Cooling and Glen Refrigeration (China): Both firms emphasize ultra‑small footprints and system integration, with MOIR focusing on high‑temperature tolerance and high COP designs, while Glen pairs compressors with micro‑condensers/evaporators to deliver system packages—an attractive option for clients seeking single‑vendor micro‑thermal solutions.

Lando Chillers and Miracle Refrigeration (China): Strong OEM partners that prioritize compactness, low vibration, and competitive pricing. They are often chosen by appliance and portable device OEMs where cost and integration speed matter.

Huayi Compressor: A large‑scale hermetic compressor manufacturer offering a breadth of displacement options and legacy scale advantages for appliance OEMs and established channel partners.

Secop (Germany): A European player with a clear focus on high‑efficiency DC compressors for mobile and medical cold‑chain applications. Their sustainability orientation and invested presence in light commercial segments make them a strategic contender in regulated markets.

Air Squared (USA): Notable for its novel small scroll compressor technology, which offers a compact alternative to rotary architectures in select vapor‑compression systems.

Recent industry activity underscores these dynamics: Aspen Compressor’s product presence at AHR Expo 2026 highlights the continued market emphasis on certified, compact rotary solutions and the premium positioning of US‑manufactured options. Across the board, vendors are responding to refrigerant transitions, efficiency mandates, and customer demand for integrated, lighter, and more energy‑efficient micro‑cooling systems.

Prioritize A2L and low‑GWP readiness: accelerate prototyping and certification for low‑GWP refrigerant compatibility; establish test plans that include service and safety protocols for end‑users and field technicians.

Hedge raw‑material risk and design for resilience: secure multi‑year supply agreements for critical copper components, evaluate copper‑reduction designs, and consider geographic sourcing diversification to mitigate price shocks.

Invest in variable‑speed systems and electronic controls: integrate inverter‑grade motor control IP early to capture efficiency and battery‑life benefits in mobile and portable applications.

Define a clear manufacturing footprint strategy: balance proximity to key OEMs and regulatory markets against cost—near‑market production for regulated regions and centralized scale for commodity lines.

Adopt a flexible channel strategy: combine direct OEM partnerships for high‑spec systems with distribution agreements for commoditized compressor lines to optimize margin and volume.

Use M&A selectively: prioritize bolt‑on buys that either provide regulatory certifications, specialized product IP, or immediate access to targeted end markets (medical, EV refrigeration, portable logistics).

The full report includes the complete quantitative dataset (USD Million revenue, historical 2020–2025, and point forecasts 2026–2032), granular segmentation by region, type and application, and the supporting methodology. In line with our "trailer" approach, this executive brief highlights strategic takeaways and actionable guidance while reserving detailed sub‑segment figures and downloadable models for subscribers. Organizations planning product launches, regional expansions, or M&A activity in 2026 will find the full report and accompanying customer workshops highly valuable to compress decision cycles and reduce execution risk.

For immediate access to the full dataset, supplier scorecards, and the tailored scenario model for your organization, contact PW Consulting to arrange a briefing and secure licensed access to the Worldwide Miniature Refrigeration Compressor Market report.

PW Consulting — Senior Strategic Advisor & Chief Industry Analyst

For detailed analysis of this topic, please visit the official page:Worldwide Miniature Refrigeration Compressor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com