Worldwide Automotive Inspection Service Market — Strategic Outlook 2026: Actionable Insights from PW Consulting

PW Consulting today publishes its flagship market research briefing, Worldwide Automotive Inspection Service Market (Base Year: 2025), designed to equip C-suite leaders, corporate strategy teams, and functional heads with the foresight required to make high-confidence decisions in 2026. Built on a multi-year historical base, rigorous primary research, and forward-looking scenario modeling, the report translates complex industry change into a concise strategic playbook. Below we summarize the strategic value of the study, highlight critical competitive and regulatory dynamics shaping the market, and outline the practical tools included to accelerate execution — while reserving granular segment-level disclosure for the full report available on our website.

Worldwide Automotive Inspection Service Market

Market at a glance: growth trajectory and market structure

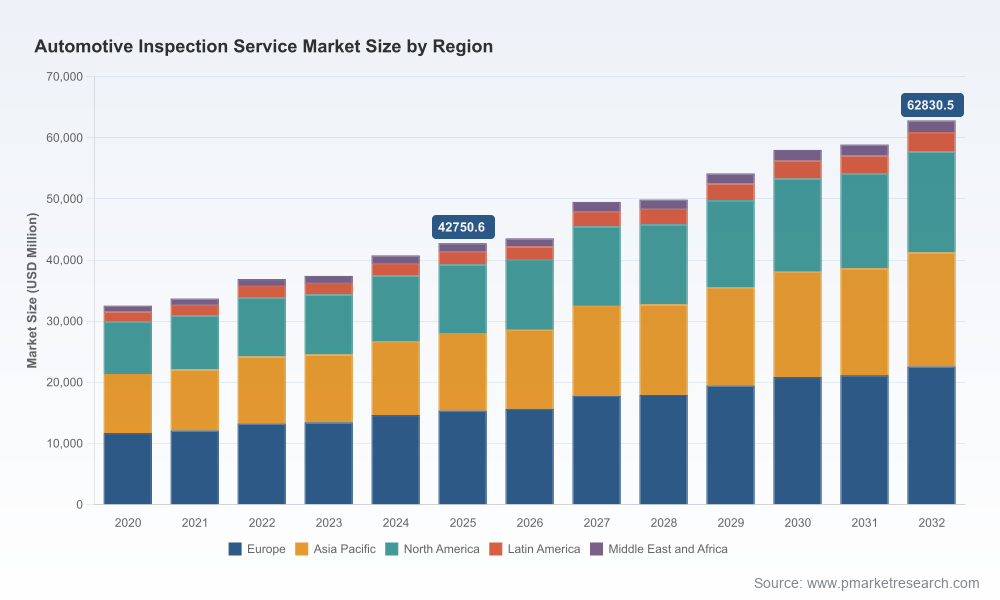

The global automotive inspection services market is on a sustained growth path. Our base-year assessment for 2025 establishes a robust market size and a mid-single-digit compound annual growth rate (CAGR) for the forecast horizon. PW Consulting’s bottom-up modeling projects continued expansion through the 2026–2032 period, driven by a mix of regulatory compliance needs, fleet modernization, and new technical testing requirements associated with electrification and software-defined vehicles.

Worldwide Automotive Inspection Service Market

- Historical performance and near-term outlook: The market has expanded steadily from the early 2020s through 2025, reflecting stable demand for statutory inspections, used-vehicle remarketing services, and an expanding remit of technical verification tasks.

- Forecast confidence: Our central forecast is based on a 2026–2032 projection that incorporates scenario sensitivity to regulatory shifts, EV adoption curves, and new testing modalities such as wireless and cybersecurity verification.

- Market structure: While the market features several large, global TIC (testing, inspection, certification) players, concentration metrics indicate substantial room for regional specialists, technology-focused entrants, and vertically integrated remarketing operators to gain share.

Why this report matters for 2026 decision-making

Executives face a unique inflection point in 2026: inspection services are no longer a pure compliance commodity. They are becoming a critical point of integration across vehicle lifecycles — from OEM validation and supply chain verification to post-sale reconditioning, warranty management, and insurance claims processing. The report equips decision-makers with three principal capabilities:

Worldwide Automotive Inspection Service Market

- Forward-looking regulatory intelligence: We map emerging and enacted regulatory changes with scenario-level impacts on inspection workloads, margin pressure, and capital requirements. This enables legal and public affairs teams to prioritize advocacy and compliance investments where they matter most.

- Technology and capability roadmaps: For operators and investors, the study delineates where to allocate CAPEX and R&D — e.g., EV battery testing, wireless/OTA validation, ADAS calibration and verification, and cybersecurity testbeds. These are accompanied by timing and ROI estimates under multiple adoption scenarios.

- Commercial and partnership strategies: The report identifies high-opportunity go-to-market plays — strategic alliances with OEMs and remarketing platforms, bolt-on acquisitions to close capability gaps, and service-bundle strategies for fleet and insurer customers.

Core market dynamics and structural trends

- Regulatory complexity and divergence: Jurisdictional changes continue to re-shape volumes and service mixes. Some regions are easing periodic safety checks for passenger vehicles while maintaining targeted emissions regimes; others are broadening technical mandates to include battery safety and cybersecurity assurances. The net effect is a redistribution of inspection workload and a premium on multi-discipline capabilities.

- Electrification and software-defined mobility: The rise of BEVs, hybrids, and connected vehicles shifts inspection requirements from mechanical checks toward diagnostics, battery health assessment, and wireless/wireless-protocol testing. Inspection providers who internalize these capabilities early will secure advantaged long-term margins.

- Digitization and AI-enabled quality assurance: AI-driven visual and sensor-based inspection systems are converting manual processes into faster, repeatable, auditable workflows. Early adopters can improve throughput, lower cost-per-inspection, and provide richer data products to OEMs and remarketers.

- Integration with remarketing and reconditioning: Vehicle remarketing platforms are increasingly embedding standardized inspection frameworks to streamline used-vehicle transactions. This vertical integration creates opportunities for inspection firms to capture higher-value service bundles.

Competitive landscape — what the leading players are doing

The market is characterized by a mix of established global TIC firms, automotive-specialized inspection chains, materials and lab-focused providers, and digital-first remarketing platforms. Notable dynamics include:

- Global TIC leaders are broadening scope. Firms with long-standing strengths in testing, inspection, and certification have expanded their automotive portfolios to include EV battery testing, ADAS validation, and supply-chain assurance. Strategic conversations among top-tier TIC firms have been public and, in at least one high-profile instance, included exploratory merger discussions — underscoring the strategic value ascribed to scale and capability breadth.

- Vehicle inspection specialists are digitally transforming. The world’s largest periodic inspection providers continue to process tens of millions of inspections annually while investing in digital services and wireless testing capabilities to stay relevant to software-defined vehicles.

- Vertical and digital platform plays are accelerating. Remarketing and auction platforms are embedding inspection services into their transactional flows, rebranding and integrating inspection capabilities to offer a seamless used-vehicle experience.

- New capability-focused entrants: Materials testing, emissions labs, and niche wireless testing consultancies are attracting attention as OEMs and fleets demand specialized third-party verification beyond traditional safety checks.

Representative examples (non-exhaustive): global TIC players with strong automotive portfolios; specialist periodic inspection operators expanding digital services; remarketing platforms integrating inspection into transactions; and materials/wireless testing firms providing OEM-focused verification services. Detailed company profiles, capability maps, and assessed strategic options for each leading actor are included in the full report.

Recent developments shaping 2026 strategy

- Large inspection chains reported strong volumes and are publicly articulating transformation programs toward digital and software-enabled mobility services; one major provider reported conducting tens of millions of vehicle inspections in the latest fiscal cycle, reinforcing its leadership in periodic technical checks.

- Strategic M&A and capability acquisitions are underway, particularly to shore up wireless testing, cybersecurity validation, and battery testing skillsets. Some discussions among top-tier TIC firms have been public but concluded without consolidation — a signal that scale is desirable but integration complexity is material.

- Policy shifts at the subnational level are already altering inspection demand. For example, some jurisdictions have removed mandatory annual safety inspections for non-commercial passenger vehicles while preserving emissions testing in specific urban areas — a pattern that will continue to produce idiosyncratic volume impacts.

- Remarketing and reconditioning networks are standardizing inspection frameworks and investing in digital tooling, raising the bar for speed, traceability, and report standardization in used-car transactions.

Actionable recommendations for 2026

Executives should prioritize the following, based on PW Consulting’s risk-and-opportunity scoring:

- For inspection providers: Accelerate capability builds in EV battery diagnostics, wireless/OTA testing, and ADAS calibration — prioritize investments that generate recurring revenue streams (service contracts, fleet programs, insurer partnerships).

- For OEMs and Tier 1 suppliers: Establish preferred third-party verification roadmaps that bundle mechanical, functional safety, and cybersecurity checks; consider co-investment in shared testbeds and certification frameworks to reduce time-to-market.

- For remarketers and digital marketplaces: Standardize inspection outputs and integrate API-driven data exchange to reduce friction in cross-border remarketing and certification claims.

- For investors and M&A teams: Target bolt-on acquisitions that deliver asymmetric capability improvements (e.g., wireless testing consultancies, battery-testing labs), and prioritize integration playbooks focused on data interoperability and workforce reskilling.

What’s in the full PW Consulting report — practical, executable content

The published study delivers a comprehensive and operationally focused toolkit intended to drive execution in 2026:

- Market model and interactive forecasts: A downloadable model covering 2020–2032 with base, upside, and downside scenarios; users can re-run assumptions to test CAPEX, revenue mix, and regulatory impact permutations.

- Regulatory and standards compendium: Jurisdiction-by-jurisdiction regulatory summaries, likely policy trajectories, and their sensitivity on service volumes and margin structures.

- Capability checklist and investment guide: Prioritized capability builds with estimated time-to-proficiency, suggested vendors/partners, and benchmark KPIs for throughput and margin improvement.

- Competitive profiles and strategic options matrix: Deep-dive profiles of leading players, emerging entrants, and system integrators, each with strategic recommendations (grow, partner, acquire, divest).

- Operational playbooks: Templates for integrating AI inspection systems, standardized digital inspection reporting, and partnership contracts for remarketers and insurers.

- Primary research appendices: Methodology, interview list, and data-sourcing notes to reassure users of the report’s empirical foundation.

How to use this intelligence

PW Consulting recommends a three-step adoption approach for 2026 planning cycles:

- Immediate (0–6 months): Run the provided model under your enterprise assumptions; map regulatory exposures by operating region; prioritize quick-win capability upgrades (digital inspection, API integration).

- Mid-term (6–18 months): Execute strategic partnerships and targeted acquisitions to fill capability gaps; pilot AI-driven inspection workflows and battery diagnostic services with select fleet customers or OEM partners.

- Long-term (18–36 months): Scale high-value service bundles (fleet warranty programs, insurer-integrated claims verification, OEM software validation), and pursue capability consolidation where economics justify larger-scale integration.

Accessing the full report

This release is an executive summary intended to convey the strategic value and key directional findings of PW Consulting’s Worldwide Automotive Inspection Service Market report. For the complete dataset, granular segment-level analysis, company-by-company financials, and interactive forecasting tools, please consult the full report available via PW Consulting’s research portal. The full publication contains the detailed segmentation and regional analyses necessary to operationalize the recommendations above.

PW Consulting’s senior analysts remain available for briefings, bespoke scenario runs, and M&A diligence support. Contact our Automotive Practice to arrange a tailored session that applies the research directly to your 2026 commercial and investment plans.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Inspection Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com