Worldwide Small Bulldozers Market — Strategic Briefing for 2026 Decision-Makers

Executive summary

PW Consulting’s latest market study sets a strategic compass for firms making capital-allocation, portfolio, and go-to-market decisions in 2026. The global small bulldozers market is estimated at approximately USD 1,345.7 Million in the base year (2025) and is projected to grow to roughly USD 1,870.9 Million by 2032. Our forecast model for the 2026–2032 period shows a compound annual growth rate (CAGR) of 4.82%, reflecting a steady, investment-grade expansion driven by infrastructure programs, replacement cycles, and incremental technology adoption in compact earthmoving.

Worldwide Small Bulldozers Market

Why this briefing matters in 2026

- Translating macro momentum into 2026 choices: With heat in global infrastructure pipelines and uneven raw-material dynamics, executives must convert headline demand into defensible, cash-generating product and channel strategies.

- Balancing innovation and margin: Small dozers are at an inflection point—demand for precision grading, fuel efficiency, and operator comfort is rising while input-cost volatility pressures margins. Our analysis shows where to invest selectively to protect profitability.

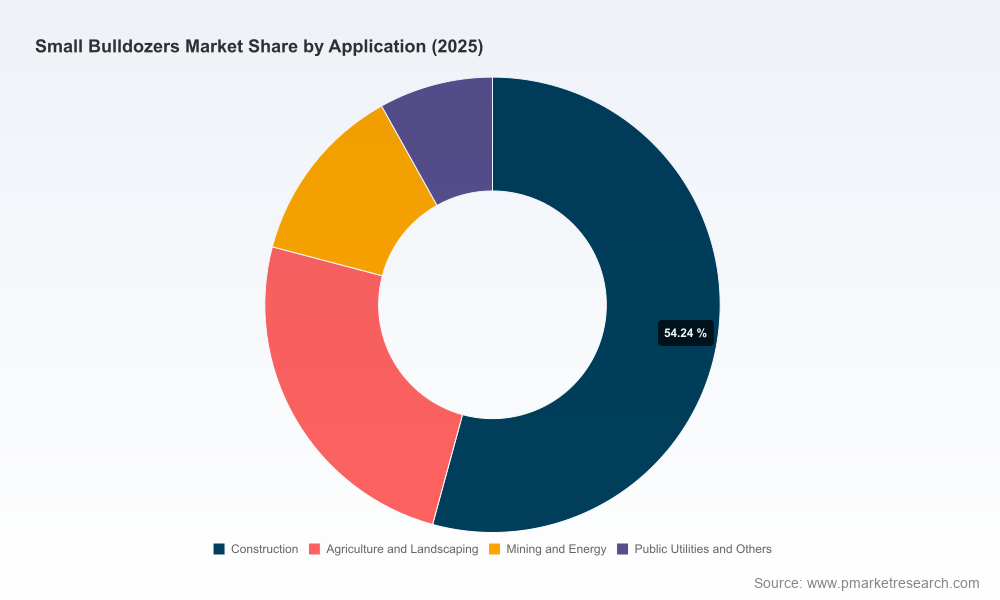

- Actionable intelligence without overload: This briefing highlights the strategic signals and decision levers from our full report while intentionally withholding granular sub-segment figures to encourage direct engagement with the full dataset and tools.

Market dynamics shaping 2026

Three structural trends dominate near-term strategy:

Worldwide Small Bulldozers Market

- Demand drivers: Continued public- and private-sector infrastructure programs, urbanization-linked landscaping and utility work, and replacement/expansion in contractor fleets underpin baseline demand. These drivers sustain above-inflation unit demand in many markets even when large-equipment cycles cool.

- Input-cost pressure and regulation: Steel cost dynamics materially affect small dozer unit economics. Global hot-rolled coil prices moved higher into early 2026, and U.S. policy shifts—most notably an increase in Section 232 tariffs on certain steel imports in mid-2025—have contributed to notable price rises in construction-grade steel products. These changes create a two-speed cost environment across suppliers with different sourcing footprints.

- Technology-led differentiation: Precision-control systems, drivetrain electrification or E-Drive hybrids, and integrated telematics are rapidly migrating from premium mid-size dozers into the small segment. Vendors that combine hardware robustness with software-enabled productivity demonstrate stronger aftermarket monetization potential.

Competitive landscape — structure and signals

The small bulldozers market is moderately concentrated. The leading tier of OEMs collectively accounts for a significant share of revenue, with a wider set of regional and price-oriented suppliers capturing meaningful niche volumes. This concentration profile creates both defensive and offensive pathways for incumbents and challengers:

Worldwide Small Bulldozers Market

- Incumbent strengths: Global OEMs emphasize integrated precision systems, operator ergonomics, and established dealer networks. Their recent product upgrades focus on SmartGrade/IMC-class controls, improved cab visibility, and fuel efficiency—features prioritized by rental fleets and civil contractors seeking utilization gains.

- Value and volume players: Competitive pressure from cost-focused manufacturers supports brisk activity in emerging markets and budget-conscious contractor segments. These suppliers use simplicity, low maintenance, and aggressive pricing to preserve share where total cost-of-ownership (TCO) constraints dominate.

- Consolidation levers: With a measured level of market concentration, M&A and partnership moves can quickly shift competitive advantage—especially for firms seeking scale in distribution, parts, or digital services.

What recent product and industry moves tell us

- Product roadmaps emphasize operator productivity and lower operating costs. Examples from the last 18 months include updates and launches of next-generation small dozer models with E-Drive options and integrated grade-control systems—concrete evidence that digitization is a near-term battleground.

- Trade-show activity in early 2026 revealed OEM focus on software-enabled hardware (IMC/SmartGrade-class offerings) and cab improvements targeted at multi-shift rental and utility crews. These moves indicate OEMs are prioritizing solutions that shorten payback for customers.

- Raw-material volatility and tariff-induced cost moves have prompted OEMs to rethink sourcing and localized component strategies. Procurement flexibility and supplier diversification are now tactical imperatives for margin protection.

Core companies analyzed

Our competitive audit centers on global and regional leaders—firms that set product and distribution benchmarks for the small-dozer segment. The report includes in-depth profiles of OEMs that illustrate differing strategic plays:

- Caterpillar Inc. — focus on integrated grading and operator-centric design for site development and utility work.

- Komatsu Ltd. — emphasis on intelligent controls and high-speed precision grading.

- Deere & Company — incorporation of SmartGrade and E-Drive to push productivity and fuel efficiency.

- Case Construction Equipment — recent N‑Series refreshes targeting visibility, controls, and efficiency across a broad lineup.

- Liebherr, Shantui, LiuGong, SDLG, XCMG, and Hyundai CE — varied approaches from premium engineering to cost-led global volume plays, each with distinct channel and aftermarket strategies.

Recent product announcements and trade-show previews (2025–2026) serve as near-term indicators of where R&D and marketing priorities are moving and are discussed in dedicated competitor case studies in the full report.

Report contents — what the full study delivers

PW Consulting’s full market study is structured to be directly operational for corporate strategy, commercial planning, and investment committees. Key deliverables include:

- Top-down and bottom-up market sizing and a 2026–2032 forecast (base year 2025), with scenario variants reflecting steel-price and tariff regimes.

- Competitive heatmaps, product-feature matrices, and dealer network assessments to support go-to-market alignment.

- Cost-pass-through and procurement sensitivity models that quantify margin exposure to steel and freight moves.

- Technology adoption pathways and aftermarket revenue forecasts to build differentiated monetization plans.

- Targeted M&A screening and partnership shortlists with financial and operational rationale.

- Actionable playbooks for OEMs, independent distributors, rental companies, and private-equity investors addressing pricing, product cadence, and service strategies.

- Appendices that document data sources, methodology, and a transparent assumptions log suitable for board-level scrutiny.

Strategic recommendations for 2026

Below are priority actions distilled from the full study—framed by time horizon and expected impact:

- Immediate (next 6 months)

- Lock in steel and key component supply through a mix of forward contracts and alternative suppliers to cap input-cost exposure.

- Prioritize upgrades to telematics and remote diagnostics on current small-dozer platforms to accelerate aftermarket revenue and reduce downtime for fleet clients.

- Recalibrate pricing strategies for markets affected by tariff-induced cost shifts, using localized value communication rather than across-the-board list increases.

- Medium term (6–24 months)

- Accelerate product modules that deliver measurable productivity gains (e.g., grade-control bundles) that reduce customers’ operating hours and justify premium pricing.

- Expand parts and service footprints in high-utilization corridors where fleet operators can be converted to subscription or outcome-based models.

- Test hybrid/electric drivetrains on high-usage small-dozer configurations to gather field data and create differentiation for urban and environmentally constrained projects.

- Strategic (24–36 months)

- Pursue selective M&A or strategic alliances to fill distribution gaps or acquire digital platforms that accelerate aftermarket monetization—targets should be assessed against the market concentration dynamics we model in the report.

- Invest in manufacturing footprint adjustments to reduce lead times and tariff exposure—localized assembly or modular production can materially improve competitiveness in tariff-impacted markets.

KPIs and decision triggers

- Monitor realized steel input inflation vs. forward curves; trigger procurement hedges if realized costs deviate more than a defined tolerance band from plan.

- Track telematics attach rates and aftermarket ARPU (average revenue per unit) as early indicators of successful digital monetization.

- Use utilization uplift (hours saved per machine per month) from precision-control options to validate pricing premiums and guide R&D prioritization.

How boards and executive teams should use the report

The study is designed for direct integration into 2026 budgeting and strategic-planning cycles. Practical applications include:

- Capex prioritization: Use product-level payback and TCO sensitivity outputs to sequence investments across product lines.

- Procurement policy: Implement recommended supplier-diversification thresholds and forward-purchasing triggers included in the procurement playbook.

- M&A and partnerships: Leverage the M&A screening appendix to shortlist targets that deliver immediate distribution scale or software-enabled monetization.

- Commercial alignment: Recalibrate dealer incentives and rental partnerships based on the segment-level use-cases and profit-pool mapping in the full report.

Conclusion — the strategic trade-off in 2026

The small bulldozers market in 2026 presents a clear trade-off: investment in productivity-enabling technologies and localized resilience can protect and expand margins, but these moves require disciplined capital allocation in an environment of input-cost turbulence and shifting regulation. PW Consulting’s full report provides the granular segmentation, scenario models, and competitor scorecards needed to convert that strategic clarity into executable plans.

To access the full dataset, interactive models, and supplier-level benchmarking that underpin these insights, please consult the PW Consulting Worldwide Small Bulldozers Market report on our website. The report includes the detailed regional and application splits, scenario outputs, and deal-level recommendations that boards and strategy teams require to act confidently in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Small Bulldozers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com